IBM 2009 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2009 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

No significant amendments of retirement-related benefit plans

occurred during the year ended December 31, 2007 that had a

material effect on the Consolidated Statement of Earnings.

Assumptions Used to Determine Plan

Financial Information

Underlying both the measurement of benefit obligations and net

periodic (income)/cost are actuarial valuations. These valuations

use participant-specific information such as salary, age and years

of service, as well as certain assumptions, the most significant

of which include estimates of discount rates, expected return on

plan assets, rate of compensation increases, interest crediting

rates and mortality rates. The company evaluates these assump-

tions, at a minimum, annually, and makes changes as necessary.

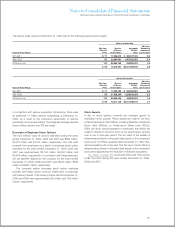

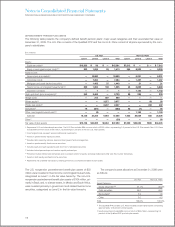

The table below presents the assumptions used to measure

the net periodic (income)/cost and the year-end benefit obliga-

tions for retirement-related benefit plans.

Defined Benefit Pension Plans

U.S. Plans Non-U.S. Plans

For the year ended December 31: 2009 2008 2007 2009 2008 2007

Weighted-average assumptions used to measure net

periodic (income)/cost for the year ended December 31:

Discount rate 5.75% 6.00% 5.75% 4.89% 5.06% 4.40%

Expected long-term returns on plan assets 8.00% 8.00% 8.00% 6.73% 6.86% 6.95%

Rate of compensation increase* N/A N/A 4.00% 3.09% 3.23% 3.05%

Weighted-average assumptions used to measure

benefit obligations at December 31:

Discount rate 5.60% 5.75% 6.00% 4.84% 4.89% 5.06%

Rate of compensation increase* N/A N/A N/A 2.92% 3.09% 3.23%

* Rate of compensation increase is not applicable to the U.S. defined benefit pension plans as benefit accruals ceased December 31, 2007 for all participants.

N/A—Not applicable

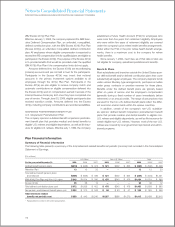

Nonpension Postretirement Benefit Plans

U.S. Plans Non-U.S. Plans

For the year ended December 31: 2009 2008 2007 2009 2008 2007

Weighted-average assumptions used to measure

net periodic cost for the year ended December 31:

Discount rate 5.75% 6.00% 5.75% 7.36% 7.13% 6.93%

Expected long-term returns on plan assets N/A 3.02% N/A 9.19% 9.04% 9.95%

Weighted-average assumptions used to measure

benefit obligations at December 31:

Discount rate 5.40% 5.75% 6.00% 7.92% 7.36% 7.13%

N/A—Not applicable

DISCOUNT RATE

The discount rate assumptions used for retirement-related ben-

efit plans accounting reflect the yields available on high-quality,

fixed income debt instruments at the measurement date. For

the U.S. discount rate assumptions, a portfolio of high-quality

corporate bonds is used to construct a yield curve. The cash

flows from the company’s expected benefit obligation payments

are then matched to the yield curve to derive the discount rates.

In the non-U.S., where markets for high-quality long-term bonds

are not generally as well developed, a portfolio of long-term

government bonds is used as a base, to which a credit spread

is added to simulate corporate bond yields at these maturities

in the jurisdiction of each plan, as the benchmark for developing

the respective discount rates.

115