IBM 2009 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2009 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

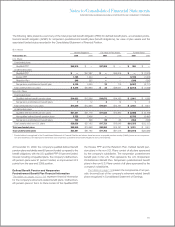

HEALTHCARE COST TREND RATE

For nonpension postretirement benefit plan accounting, the

company reviews external data and its own historical trends for

healthcare costs to determine the healthcare cost trend rates.

However, the healthcare cost trend rate has an insignificant

effect on plan costs and obligations as a result of the terms of

the plan which limit the company’s obligation to the participants.

The company assumes that the healthcare cost trend rate for

2010 will be 7 percent. In addition, the company assumes that

the same trend rate will decrease to 5 percent over the next

three years. A one percentage point increase or decrease in the

assumed healthcare cost trend rate would not have a material

effect on 2009, 2008 and 2007 net periodic cost or the benefit

obligations as of December 31, 2009 and 2008.

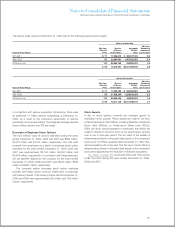

Plan Assets

Retirement-related benefit plan assets are recognized and mea-

sured at fair value as described in note A, “Significant Accounting

Policies,” on page 77. Because of the inherent uncertainty of

valuations, these fair value measurements may not necessarily

reflect the amounts the company could realize in current market

transactions.

INVESTMENT POLICIES AND STRATEGIES

The investment objectives of the Qualified PPP portfolio are

designed to generate returns that will enable the plan to meet

its future obligations. The precise amount for which these obli-

gations will be settled depends on future events, including the

retirement dates and life expectancy of the plans’ participants.

The obligations are estimated using actuarial assumptions, based

on the current economic environment and other pertinent factors

described on page 115. The Qualified PPP portfolio’s investment

strategy balances the requirement to generate returns, using

potentially higher yielding assets such as equity securities, with

the need to control risk in the portfolio with less volatile assets,

such as fixed-income securities. Risks include, among others,

inflation, volatility in equity values and changes in interest rates

that could cause the plan to become underfunded, thereby

increasing its dependence on contributions from the company.

To mitigate any potential concentration risk, careful consider-

ation is given to balancing the portfolio among industry sectors,

companies and geographies, taking into account interest rate

sensitivity, dependence on economic growth, currency and other

factors that affect investment returns. As a result, the Qualified

PPP portfolio’s target allocation is 44 percent equity securities,

46 percent fixed income securities, 5 percent real estate and 5

percent other investments, which is consistent with the alloca-

tion decisions made by the company’s management and is

similar to the prior year target allocation. The table on page 118

details the actual allocation of equity, fixed income, real estate

and all other types of investments for the Qualified PPP portfolio.

The assets are managed by professional investment firms

and investment professionals who are employees of the com-

pany. They are bound by investment mandates determined by

the company’s management and are measured against specific

benchmarks. Among these managers, consideration is given,

but not limited to, balancing security concentration, issuer con-

centration, investment style and reliance on particular active and

passive investment strategies.

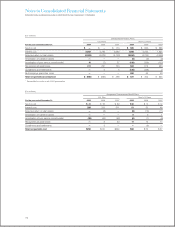

Market liquidity risks are tightly controlled, with only a mod-

est percentage of the Qualified PPP portfolio invested in private

market assets consisting of private equities and private real

estate investments, which are less liquid than publicly traded

securities. As of December 31, 2009, the Qualified PPP port-

folio had $3,618 million in commitments for future investments

in private markets to be made over a number of years. These

commitments are expected to be funded from plan assets.

Derivatives are used on a limited basis as an effective means

to achieve investment objectives and/or as a component of

the plan’s risk management strategy. The primary reasons for

the use of derivatives are fixed income management, including

duration, interest rate management and credit exposure, cash

equitization and as a means to gain exposure to the currency

and commodities markets.

Outside the U.S., the investment objectives are similar to

those described above, subject to local regulations. The weighted-

average target allocation for the non-U.S. plans is 47 percent

equity securities, 46 percent fixed income securities, 2 percent

real estate and 5 percent other investments, which is consistent

with the allocation decisions made by the company’s manage-

ment and is similar to the prior year weighted-average target

allocation. The table on page 118 details the actual allocations

of equity, fixed income, real estate and all other types of invest-

ments for non-U.S. plans. In some countries, a higher percent-

age allocation to fixed income securities is required. In others,

the responsibility for managing the investments typically lies with

a board that may include up to 50 percent of members elected

by employees and retirees. This can result in slight differences

compared with the strategies previously described. Generally,

these non-U.S. plans do not invest in illiquid assets and their

use of derivatives is usually limited to currency hedging, adjust-

ing portfolio durations and reducing specific market risks. There

was no significant change in the investment strategies of these

plans during either 2009 or 2008.

The company’s nonpension postretirement benefit plans are

underfunded or unfunded. For some plans, the company main-

tains a nominal, highly liquid trust fund balance to ensure timely

benefit payments.

117