Experian 2010 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2010 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Experian Annual Report 2010 Financial statements92

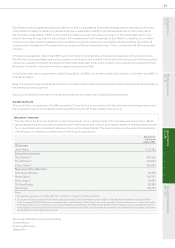

Notes to the Group nancial statements (continued)

3. Recent accounting developments (continued)

At the balance sheet date, a number of new standards, amendments and interpretations were in issue but are not yet effective for

the Group and have not been early adopted:

Amendment to IAS 27 – ‘Consolidated and Separate Financial Statements’ -

Amendment to IAS 39 – ‘Eligible Hedged Items’ -

Amendment to IFRS 2 – ‘Group Cash–Settled Share–Based Payment Transactions’ -

Revision to IFRS 3 – ‘Business Combinations’ -

Improvements to IFRSs (April 2009) -

Amendments to IFRIC 9 and IAS 39 –‘Embedded Derivatives’ -

IFRIC 17 – ‘Distributions of Non–Cash Assets to Owners’ -

IFRIC 18 – ‘Transfers of Assets from Customers’ -

The amendments to IAS 27 and IFRS 3 will impact the accounting treatment of acquisitions in the Group nancial statements.

If they had been adopted, the other new standards, amendments or interpretations would have had no material effect on the

results or nancial position of the Group disclosed within these nancial statements although a number would lead to additional

or revised disclosures.

4. Signicant accounting policies

The principal accounting policies applied in the preparation of these nancial statements are set out below. These policies have

been consistently applied to both years presented, unless otherwise stated.

Basis of consolidation

Subsidiaries

Subsidiaries are fully consolidated from the date on which control is transferred to the Group. They cease to be consolidated

from the date that the Group no longer has control. As required by IFRS 3, all business combinations are accounted for using the

purchase method.

Intra-group transactions, balances and unrealised gains on transactions between group companies are eliminated on

consolidation. Unrealised losses are also eliminated unless the transaction provides evidence of an impairment of the asset

transferred.

Accounting policies of subsidiaries and segments are consistent with the policies adopted by the Group for the purposes of the

Group’s consolidation. The Group nancial statements incorporate the nancial statements of the Company and its subsidiary

undertakings for the nancial year ended 31 March 2010. A list of the signicant subsidiaries is given in note Q to the parent

company nancial statements.

Minority interests

The Group applies a policy of treating transactions with minority interests as transactions with parties external to the Group.

Disposals to minority interests result in gains and losses for the Group that are recorded in the Group income statement.

Purchases from minority interests result in goodwill, being the difference between any consideration paid and the relevant share

acquired of the carrying value of the net assets of the subsidiary.

Associates

Associates are entities over which the Group has signicant inuence but not control, generally achieved by a shareholding of

between 20% and 50% of the voting rights. The equity method is used to account for investments in associates and investments

are initially recognised at cost.

The Group’s share of net assets of its associates and loans made to associates are included in the Group balance sheet. The

Group’s share of its associates’ post-acquisition after tax prots or losses is recognised in the Group income statement, and its

share of post-acquisition movements in equity is recognised in the Group’s statement of changes in total equity. The cumulative

post-acquisition movements are adjusted against the carrying amount of the investment. The carrying amount of an investment in

an associate is tested for impairment by comparing its recoverable amount to its carrying amount whenever there is an indication

that the investment may be impaired.