Experian 2010 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2010 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

103

Introduction

2 – 11

Business review

12 – 51

Governance

52 – 84

Financial statements

85 – 160

5. Financial risk management (continued)

This credit risk is minimised by a policy under which the Group only enters into such contracts with banks and nancial

institutions with strong credit ratings, within limits set for each organisation. Dealing activity is closely controlled and

counterparty positions are monitored regularly. The general credit risk on derivative nancial instruments utilised by the Group

is therefore not considered to be signicant. No credit limits were exceeded during the year and the Group does not anticipate

that any losses will arise from non-performance by these counterparties.

At the balance sheet date trade receivables with nancial institutions accounted for some 45% (2009: 37%) of total trade

receivables in the UK and some 20% (2009: 33%) of total trade receivables in the USA. The remaining balances are distributed

across multiple industries and geographies. The Group has implemented policies that require appropriate credit checks on

potential customers before granting credit. The maximum credit risk in respect of such nancial assets is the carrying value of

the assets.

Liquidity risk

The Group maintains long-term committed facilities to ensure it has sufcient funds available for operations and planned

expansions. The Group monitors rolling forecasts of projected cash ows to ensure that it will have adequate undrawn

committed facilities available.

Details of the facilities available to the Group and their utilisation at the balance sheet date are given in note 24. The maturity

analysis of nancial liabilities is given in note 28.

Capital risk management

The Group’s objectives in managing capital are to safeguard its ability to continue as a going concern in order to provide returns

for shareholders and benets for other stakeholders and to maintain an optimal capital structure and cost of capital.

In order to maintain or adjust the capital structure, the Group may adjust the amount of dividends paid to shareholders, return

capital to shareholders, issue new shares or sell assets to reduce net debt. As part of its internal reporting processes the Group

monitors capital employed by operating segment. For this purpose, capital employed excludes net debt and tax balances and at

31 March 2010 the Group’s capital employed was US$4,251m (2009: US$4,205m). The Group manages its working capital in order

to meet its target to convert at least 90% of EBIT into operating cash ow and the conversion percentage for the year ended 31

March 2010 was 98% (2009: 99%).

Fair value estimation

The fair value of derivative nancial instruments and other nancial assets and liabilities is determined by using market data

and established estimation techniques such as discounted cash ow and option valuation models. The fair value of foreign

exchange contracts is based on a comparison of the contractual and year end exchange rates. The fair values of other derivative

nancial instruments are estimated by discounting the future cash ows to net present values using appropriate market rates

prevailing at the year end.

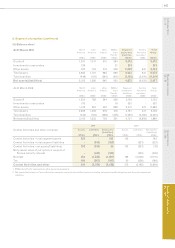

The following table presents an analysis of the Group’s nancial assets and nancial liabilities that are measured at fair value at

31 March 2010 by level, as required and dened by IFRS 7 ‘Improving Disclosures about Financial Instruments’:

Level 1

US$m

Level 2

US$m

Level 3

US$m

To t a l

US$m

Assets

Loans and receivables -44 -44

Derivatives used for hedging -43 -43

Financial assets at fair value through prot and loss -19 928

Available for sale 33 - - 33

Total assets 33 106 9148

Liabilities

Derivatives used for hedging -35 -35

Financial liabilities at fair value through prot and loss -70 669 739

Total liabilities -105 669 774

Net nancial assets/(liabilities) 33 1(660) (626)

Valuations that are based on unadjusted quoted prices in active markets for identical assets and liabilities are classied as

Level 1 in the above analysis. Inputs other than quoted prices included in Level 1, that are observable for the asset or liability,

either directly (that is, as prices) or indirectly (that is, derived from prices), are classied as Level 2. Inputs for assets or

liabilities that are not based on observable market data are classied as Level 3.