Wells Fargo 2005 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

90

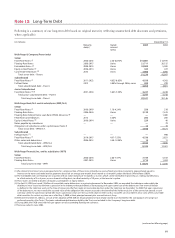

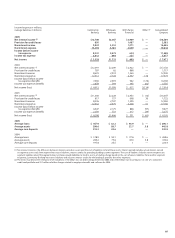

(in millions) Year ended December 31,

2005 2004 2003

Outside professional services $835 $669 $509

Contract services 596 626 866

Travel and entertainment 481 442 389

Outside data processing 449 418 404

Advertising and promotion 443 459 392

Postage 281 269 336

Telecommunications 278 296 343

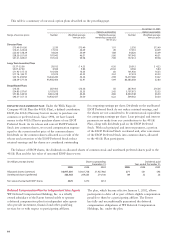

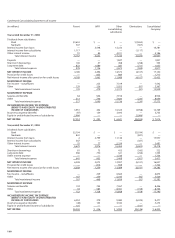

Year ended December 31,

2005 2004 2003

Pension Other Pension Other Pension Other

benefits(1) benefits benefits(1) benefits benefits(1) benefits

Discount rate 6.0% 6.0% 6.5% 6.5% 7.0% 7.0%

Expected

return on

plan assets 9.0 9.0 9.0 9.0 9.0 9.0

Rate of

compensation

increase 4.0 — 4.0 — 4.0 —

(1) Includes both qualified and nonqualified pension benefits.

The weighted-average assumptions used to determine the

net periodic benefit cost were:

The long-term rate of return assumptions above were

derived based on a combination of factors including

(1) long-term historical return experience for major asset

class categories (for example, large cap and small cap

domestic equities, international equities and domestic fixed

income), and (2) forward-looking return expectations for

these major asset classes.

To account for postretirement health care plans we use a

health care cost trend rate to recognize the effect of expected

changes in future health care costs due to medical inflation,

utilization changes, new technology, regulatory requirements

and Medicare cost shifting. We assumed average annual

increases of 9.5% for health care costs for 2006. The rate

of average annual increases is assumed to trend down 1%

each year between 2006 and 2010. By 2010 and thereafter,

we assumed rates of 5.5% for HMOs and for all other types

of coverage. Increasing the assumed health care trend by

one percentage point in each year would increase the benefit

obligation as of December 31, 2005, by $52 million and

the total of the interest cost and service cost components

of the net periodic benefit cost for 2005 by $4 million.

Decreasing the assumed health care trend by one percentage

point in each year would decrease the benefit obligation as

of December 31, 2005, by $48 million and the total of the

interest cost and service cost components of the net periodic

benefit cost for 2005 by $4 million.

Other Expenses

Expenses exceeding 1% of total interest income and noninterest

income that are not otherwise shown separately in the financial

statements or Notes to Financial Statements were:

(in millions) Pension benefits Other

Qualified Non-qualified benefits

Year ended December 31,

2006 $ 288 $ 24 $ 54

2007 315 27 55

2008 366 28 56

2009 329 34 57

2010 339 33 62

2011-2015 1,986 158 313

The investment strategy for the postretirement plans is

maintained separate from the strategy for the pension plans.

The general target asset mix is 55–65% equities and 35–45%

fixed income. In addition, the Retiree Medical Plan Voluntary

Employees’ Beneficiary Association (VEBA) considers the

effect of income taxes by utilizing a combination of variable

annuity and low turnover investment strategies. Members of

the EBRC formally review the investment risk and performance

of the postretirement plans on a quarterly basis.

Future benefits, reflecting expected future service that

we expect to pay under the pension and other benefit

plans, were: