Wells Fargo 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

87

Note 15: Employee Benefits and Other Expenses

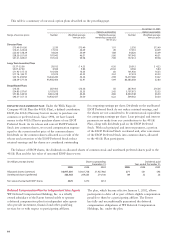

Employee Benefits

We sponsor noncontributory qualified defined benefit

retirement plans including the Cash Balance Plan. The

Cash Balance Plan is an active plan that covers eligible

employees (except employees of certain subsidiaries).

Under the Cash Balance Plan, eligible employees’ Cash

Balance Plan accounts are allocated a compensation credit

based on a percentage of their certified compensation. The

compensation credit percentage is based on age and years

of credited service. In addition, investment credits are

allocated to participants quarterly based on their accumulated

balances. Employees become vested in their Cash Balance

Plan accounts after completing five years of vesting service

or reaching age 65, if earlier.

Although we were not required to make a contribution

in 2005 for our Cash Balance Plan, we funded the maximum

amount deductible under the Internal Revenue Code, or

$288 million. The total amount contributed for our pension

plans was $340 million. We expect that we will not be

required to make a contribution in 2006 for the Cash

Balance Plan. The maximum we can contribute in 2006 for

the Cash Balance Plan depends on several factors, including

the finalization of participant data. Our decision on how

much to contribute, if any, depends on other factors,

including the actual investment performance of plan assets.

Given these uncertainties, we cannot at this time reliably

estimate the maximum deductible contribution or the

amount that we will contribute in 2006 to the Cash

Balance Plan. For the unfunded nonqualified pension plans

and postretirement benefit plans, we will contribute the

minimum required amount in 2006, which equals the benefits

paid under the plans. In 2005, we paid $78 million in benefits

for the postretirement plans, which included $29 million

in retiree contributions, and $13 million for the unfunded

pension plans.

We sponsor defined contribution retirement plans

including the 401(k) Plan. Under the 401(k) Plan, after

one month of service, eligible employees may contribute up

to 25% of their pretax certified compensation, although

there may be a lower limit for certain highly compensated

employees in order to maintain the qualified status of the

401(k) Plan. Eligible employees who complete one year

of service are eligible for matching company contributions,

which are generally a 100% match up to 6% of an employee’s

certified compensation. The matching contributions generally

vest over four years.

Expenses for defined contribution retirement plans were

$370 million, $356 million and $257 million in 2005, 2004

and 2003, respectively.

We provide health care and life insurance benefits for

certain retired employees and reserve the right to terminate

or amend any of the benefits at any time.

The information set forth in the following tables is

based on current actuarial reports using the measurement

date of November 30 for our pension and postretirement

benefit plans.