Wells Fargo 2005 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

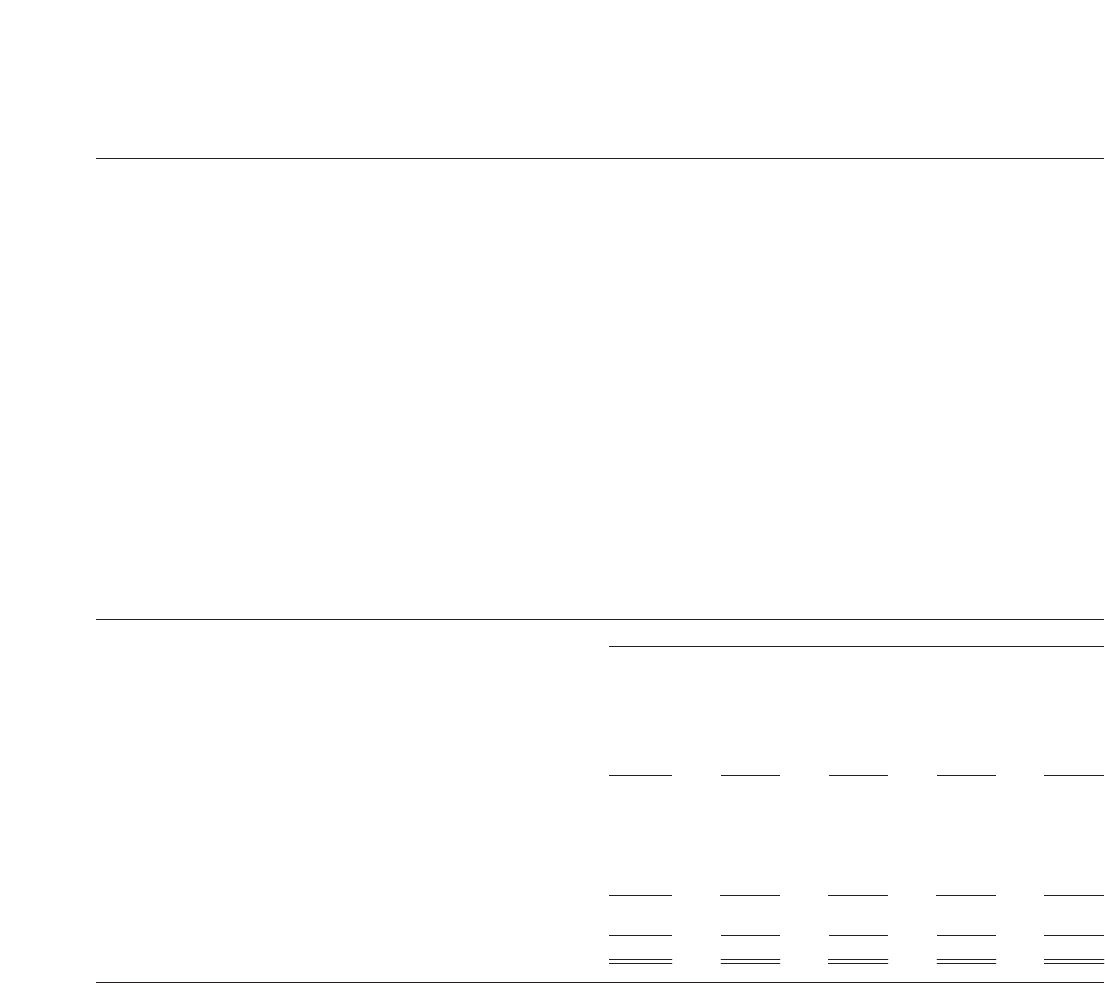

73

14% of total loans at December 31, 2005, compared with

18% at the end of 2004. These loans are mostly within the

larger metropolitan areas in California, with no single area

consisting of more than 3% of our total loans. Changes in

real estate values and underlying economic conditions for

these areas are monitored continuously within our credit

risk management process.

Some of our real estate 1-4 family mortgage loans, including

first mortgage and home equity products, include an interest-

only feature as part of the loan terms. At December 31, 2005,

such loans were approximately 26% of total loans, compared

with 28% at the end of 2004. Substantially all of these loans

are considered to be prime or near prime. We do not offer

option adjustable-rate mortgage products, nor do we offer

variable-rate mortgage products with fixed payment amounts,

commonly referred to within the financial services industry as

negative amortizing mortgage loans.

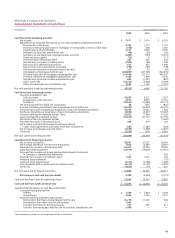

A summary of the major categories of loans outstanding is

shown in the following table. Outstanding loan balances

reflect unearned income, net deferred loan fees, and unamor-

tized discount and premium totaling $3,918 million and

$3,766 million at December 31, 2005 and 2004, respectively.

Loan concentrations may exist when there are amounts

loaned to a multiple number of borrowers engaged in similar

activities or similar types of loans extended to a diverse group

of borrowers that would cause them to be similarly impacted

by economic or other conditions. At December 31, 2005 and

2004, we did not have concentrations representing 10% or

more of our total loan portfolio in commercial loans (by

industry); commercial real estate loans (other real estate

mortgage and real estate construction) (by state or property

type); or other revolving credit and installment loans (by

product type). Our real estate 1-4 family mortgage loans to

borrowers in the state of California represented approximately

Note 6: Loans and Allowance for Credit Losses

(in millions) December 31,

2005 2004 2003 2002 2001

Commercial and commercial real estate:

Commercial $ 61,552 $ 54,517 $ 48,729 $ 47,292 $ 47,547

Other real estate mortgage 28,545 29,804 27,592 25,312 24,808

Real estate construction 13,406 9,025 8,209 7,804 7,806

Lease financing 5,400 5,169 4,477 4,085 4,017

Total commercial and commercial real estate 108,903 98,515 89,007 84,493 84,178

Consumer:

Real estate 1-4 family first mortgage 77,768 87,686 83,535 44,119 29,317

Real estate 1-4 family junior lien mortgage 59,143 52,190 36,629 28,147 21,801

Credit card 12,009 10,260 8,351 7,455 6,700

Other revolving credit and installment 47,462 34,725 33,100 26,353 23,502

Total consumer 196,382 184,861 161,615 106,074 81,320

Foreign 5,552 4,210 2,451 1,911 1,598

Total loans $310,837 $287,586 $253,073 $192,478 $167,096

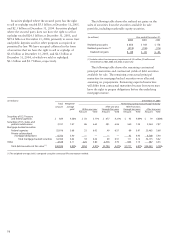

For certain extensions of credit, we may require collateral,

based on our assessment of a customer’s credit risk. We hold

various types of collateral, including accounts receivable,

inventory, land, buildings, equipment, automobiles, financial

instruments, income-producing commercial properties and

residential real estate. Collateral requirements for each customer

may vary according to the specific credit underwriting, terms

and structure of loans funded immediately or under a

commitment to fund at a later date.

A commitment to extend credit is a legally binding agree-

ment to lend funds to a customer, usually at a stated interest

rate and for a specified purpose. These commitments have

fixed expiration dates and generally require a fee. When we

make such a commitment, we have credit risk. The liquidity

requirements or credit risk will be lower than the contractual

amount of commitments to extend credit because a significant

portion of these commitments are expected to expire without

being used. Certain commitments are subject to loan agree-

ments with covenants regarding the financial performance

of the customer that must be met before we are required to

fund the commitment. We use the same credit policies in

extending credit for unfunded commitments and letters of

credit that we use in making loans. For information on

standby letters of credit, see Note 24.