Wells Fargo 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

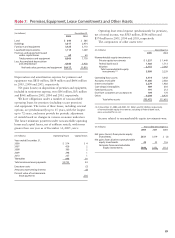

74

(in millions) December 31,

2005 2004

Commercial and commercial real estate:

Commercial $ 71,548 $ 59,603

Other real estate mortgage 2,398 2,788

Real estate construction 9,369 7,164

Total commercial and

commercial real estate 83,315 69,555

Consumer:

Real estate 1-4 family first mortgage 10,229 9,009

Real estate 1-4 family junior lien mortgage 37,909 31,396

Credit card 45,270 38,200

Other revolving credit and installment 13,957 15,427

Total consumer 107,365 94,032

Foreign 675 407

Total unfunded loan commitments $191,355 $163,994

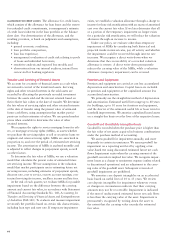

In addition, we manage the potential risk in credit com-

mitments by limiting the total amount of arrangements, both

by individual customer and in total, by monitoring the size

and maturity structure of these portfolios and by applying

the same credit standards for all of our credit activities.

The total of our unfunded loan commitments, net of all

funds lent and all standby and commercial letters of credit

issued under the terms of these commitments, is summarized

by loan category in the following table:

We have an established process to determine the adequacy

of the allowance for credit losses that assesses the risks and

losses inherent in our portfolio. This process supports an

allowance consisting of two components, allocated and

unallocated. For the allocated component, we combine

estimates of the allowances needed for loans analyzed on

a pooled basis and loans analyzed individually (including

impaired loans).

Approximately two-thirds of the allocated allowance

is determined at a pooled level for consumer loans and some

segments of commercial small business loans. We use fore-

casting models to measure inherent loss in these portfolios.

We frequently validate and update these models to capture

recent behavioral characteristics of the portfolios, as well as

changes in our loss mitigation or marketing strategies.

The remaining allocated allowance is for commercial loans,

commercial real estate loans and lease financing. We initially

estimate this portion of the allocated allowance by applying

historical loss factors statistically derived from tracking loss

content associated with actual portfolio movements over a

specified period of time, using a standardized loan grading

process. Based on this process, we assign loss factors to each

pool of graded loans and a loan equivalent amount for

unfunded loan commitments and letters of credit. These

estimates are then adjusted or supplemented where necessary

from additional analysis of long term average loss experience,

external loss data, or other risks identified from current

conditions and trends in selected portfolios. Also, we

individually review nonperforming loans over $3 million

for impairment based on cash flows or collateral. We include

the impairment on these nonperforming loans in the allocated

allowance unless it has already been recognized as a loss.

The potential risk from unfunded loan commitments and

letters of credit for wholesale loan portfolios is considered

along with the loss analysis of loans outstanding. Unfunded

commercial loan commitments and letters of credit are

converted to a loan equivalent factor as part of the analysis.

The reserve for unfunded credit commitments was $186 million

at December 31, 2005, and $188 million at December 31, 2004,

both representing less than 5% of the total allowance for

credit losses.

The allocated allowance is supplemented by the unallo-

cated allowance to adjust for imprecision and to incorporate

the range of probable outcomes inherent in estimates used

for the allocated allowance. The unallocated allowance is

the result of our judgment of risks inherent in the portfolio,

economic uncertainties, historical loss experience and other

subjective factors, including industry trends.

No material changes in estimation methodology for the

allowance for credit losses were made in 2005.

The ratios of the allocated allowance and the unallocated

allowance to the total allowance may change from period to

period. The total allowance reflects management’s estimate

of credit losses inherent in the loan portfolio, including

unfunded credit commitments, at December 31, 2005.

Like all national banks, our subsidiary national banks

continue to be subject to examination by their primary

regulator, the Office of the Comptroller of the Currency

(OCC), and some have OCC examiners in residence. The

OCC examinations occur throughout the year and target

various activities of our subsidiary national banks, including

both the loan grading system and specific segments of the

loan portfolio (for example, commercial real estate and

shared national credits). The Parent and its nonbank

subsidiaries are examined by the Federal Reserve Board.

We consider the allowance for credit losses of $4.06 billion

adequate to cover credit losses inherent in the loan portfolio,

including unfunded credit commitments, at December 31, 2005.