Wells Fargo 2005 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

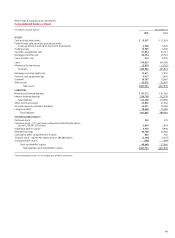

53

impact origination and servicing fees with a lag. The amount

and timing of the impact on origination and servicing fees

will depend on the magnitude, speed and duration of the

change in interest rates.

Under GAAP, MSRs are adjusted at the end of each

quarter to the lower of cost or market. While the valuation

of MSRs can be highly subjective and involve complex

judgments by management about matters that are inherently

unpredictable, changes in interest rates influence a variety

of assumptions included in the periodic valuation of MSRs.

Assumptions affected include prepayment speed, expected

returns and potential risks on the servicing asset portfolio,

the value of escrow balances and other servicing valuation

elements impacted by interest rates.

A decline in interest rates increases the propensity for

refinancing, reduces the expected duration of the servicing

portfolio and therefore reduces the estimated value of MSRs.

This reduction in value causes a charge to income as a result

of increasing the valuation allowance for potential MSRs

impairment (net of any gains on derivatives used to hedge

MSRs). We typically do not fully hedge with financial

instruments (derivatives or securities) all of the potential

decline in the value of our MSRs to a decline in interest rates

because the potential increase in origination/servicing fees

in that scenario provides a partial “natural business hedge.”

In a rising rate period, when the MSRs valuation is not fully

hedged with derivatives, the amount of valuation allowance

that can be recaptured into income will typically—although

not always—exceed the losses on any derivatives hedging

the MSRs.

Hedging the various sources of interest rate risk in mort-

gage banking is a complex process that requires sophisticated

modeling and constant monitoring. While we attempt to

balance these various aspects of the mortgage business,

there are several potential risks to earnings:

• MSRs valuation changes associated with interest rate

changes are recorded in earnings immediately within

the accounting period in which those interest rate

changes occur, whereas the impact of those same

changes in interest rates on origination and servicing

fees occur with a lag and over time. Thus, the mortgage

business could be protected from adverse changes in

interest rates over a period of time on a cumulative

basis but still display large variations in income in any

accounting period.

• The degree to which the “natural business hedge” off-

sets changes in MSRs valuations is imperfect, varies at

different points in the interest rate cycle, and depends

not just on the direction of interest rates but on the

pattern of quarterly interest rate changes. For example,

given the relatively high level of refinancing activity in

recent years and the increase in interest rates in 2005,

any significant increase in refinancing activity would

likely occur only if rates drop substantially from year-

end 2005 levels.

• Origination volumes, the valuation of MSRs and hedging

results and associated costs are also impacted by many

factors. Such factors include the mix of new business

between ARMs and fixed-rated mortgages, the relation-

ship between short-term and long-term interest rates,

the degree of volatility in interest rates, the relationship

between mortgage interest rates and other interest rate

markets, and other interest rate factors. Many of these

factors are hard to predict and we may not be able to

directly or perfectly hedge their effect.

• While our hedging activities are designed to balance

our mortgage banking interest rate risks, the financial

instruments we use, including mortgage, U.S. Treasury,

and LIBOR-based futures, forwards, swaps and options,

may not perfectly correlate with the values and income

being hedged.

Our MSRs totaled $12.5 billion, net of a valuation

allowance of $1.2 billion at December 31, 2005, and

$7.9 billion, net of a valuation allowance of $1.6 billion, at

December 31, 2004. The weighted-average note rate of our

owned servicing portfolio was 5.72% at December 31, 2005,

and 5.75% at December 31, 2004. Our MSRs were 1.44%

of mortgage loans serviced for others at December 31, 2005,

and 1.15% at December 31, 2004.

As part of our mortgage banking activities, we enter into

commitments to fund residential mortgage loans at specified

times in the future. A mortgage loan commitment is an interest

rate lock that binds us to lend funds to a potential borrower

at a specified interest rate and within a specified period of

time, generally up to 60 days after inception of the rate lock.

These loan commitments are derivative loan commitments if

the loans that will result from the exercise of the commitments

will be held for sale. Under FAS 133, Accounting for Derivative

Instruments and Hedging Activities (as amended), these

derivative loan commitments are recognized at fair value

on the consolidated balance sheet with changes in their fair

values recorded as part of income from mortgage banking

operations. Consistent with EITF 02-3, Issues Involved

in Accounting for Derivative Contracts Held for Trading

Purposes and Contracts Involved in Energy Trading and Risk

Management Activities, and SEC Staff Accounting Bulletin

No. 105, Application of Accounting Principles to Loan

Commitments, we record no value for the loan commitment

at inception. Subsequent to inception, we recognize fair

value of the derivative loan commitment based on estimated

changes in the fair value of the underlying loan that would

result from the exercise of that commitment and on changes

in the probability that the loan will fund within the terms of

the commitment. The value of that loan is affected primarily

by changes in interest rates and the passage of time. We also

apply a fall-out factor to the valuation of the derivative loan

commitment for the probability that the loan will not fund

within the terms of the commitments. The value of the MSRs is

recognized only after the servicing asset has been contractually

separated from the underlying loan by sale or securitization.