Wells Fargo 2005 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

|

|

105

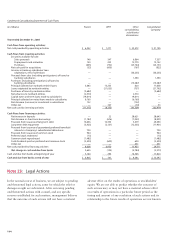

Note 24: Guarantees

We provide significant guarantees to third parties including

standby letters of credit, various indemnification agreements,

guarantees accounted for as derivatives, contingent consider-

ation related to business combinations and contingent

performance guarantees.

We issue standby letters of credit, which include performance

and financial guarantees, for customers in connection with

contracts between the customers and third parties. Standby

letters of credit assure that the third parties will receive

specified funds if customers fail to meet their contractual

obligations. We are obliged to make payment if a customer

defaults. Standby letters of credit were $10.9 billion at

December 31, 2005, and $9.4 billion at December 31, 2004,

including financial guarantees of $6.4 billion and $5.3 billion,

respectively, that we had issued or purchased participations

in. Standby letters of credit are net of participations sold to

other institutions of $2.1 billion at December 31, 2005,

and $1.7 billion at December 31, 2004. We consider the

credit risk in standby letters of credit in determining the

allowance for credit losses. Deferred fees for these standby

letters of credit were not significant to our financial statements.

We also had commitments for commercial and similar

letters of credit of $761 million at December 31, 2005,

and $731 million at December 31, 2004. At December 31,

2004, we also provided a back-up liquidity facility to a

commercial paper conduit that we considered to be a financial

guarantee. This credit facility, which was terminated in

2005, would have required us to advance, under certain

conditions, up to $860 million at December 31, 2004. This

back-up liquidity facility was included within our commercial

loan commitments at December 31, 2004, and was substantially

collateralized in the event it was drawn upon.

We enter into indemnification agreements in the ordinary

course of business under which we agree to indemnify third

parties against any damages, losses and expenses incurred in

connection with legal and other proceedings arising from

relationships or transactions with us. These relationships or

transactions include those arising from service as a director

or officer of the Company, underwriting agreements relating to

our securities, securities lending, acquisition agreements, and

various other business transactions or arrangements. Because

the extent of our obligations under these agreements depends

entirely upon the occurrence of future events, our potential

future liability under these agreements is not determinable.

We write options, floors and caps. Options are exercisable

based on favorable market conditions. Periodic settlements

occur on floors and caps based on market conditions. The

fair value of the written options liability in our balance sheet

was $563 million at December 31, 2005, and $374 million

at December 31, 2004. The aggregate written floors and caps

liability was $169 million and $227 million, respectively. Our

ultimate obligation under written options, floors and caps is

based on future market conditions and is only quantifiable

at settlement. The notional value related to written options

was $45.5 billion at December 31, 2005, and $29.7 billion

at December 31, 2004, and the aggregate notional value

related to written floors and caps was $24.3 billion and

$34.7 billion, respectively. We offset substantially all

options written to customers with purchased options.

We also enter into credit default swaps under which

we buy loss protection from or sell loss protection to a

counterparty in the event of default of a reference obligation.

The carrying amount of the contracts sold was a liability

of $6 million at December 31, 2005, and $2 million at

December 31, 2004. The maximum amount we would be

required to pay under the swaps in which we sold protection,

assuming all reference obligations default at a total loss,

without recoveries, was $2.7 billion and $2.6 billion

based on notional value at December 31, 2005 and 2004,

respectively. We purchased credit default swaps of comparable

notional amounts to mitigate the exposure of the written

credit default swaps at December 31, 2005 and 2004. These

purchased credit default swaps had terms (i.e., used the same

reference obligation and maturity) that would offset our

exposure from the written default swap contracts in which

we are providing protection to a counterparty.

In connection with certain brokerage, asset management

and insurance agency acquisitions we have made, the terms

of the acquisition agreements provide for deferred payments

or additional consideration based on certain performance

targets. At December 31, 2005 and 2004, the amount of

contingent consideration we expected to pay was not

significant to our financial statements.

We have entered into various contingent performance

guarantees through credit risk participation arrangements

with remaining terms ranging from one to 24 years. We will

be required to make payments under these guarantees if a

customer defaults on its obligation to perform under certain

credit agreements with third parties. Because the extent of

our obligations under these guarantees depends entirely

on future events, our potential future liability under these

agreements is not fully determinable. However, our exposure

under most of the agreements can be quantified and for

those agreements our exposure was contractually limited

to an aggregate liability of approximately $110 million at

December 31, 2005, and $370 million at December 31, 2004.