Wells Fargo 2005 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

35

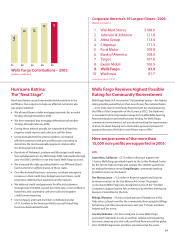

Our solid financial performance enables us to be one

of the top givers to non-profits among all U.S. companies.

We continued to have the only “Aaa” rated bank in the

U.S., the highest possible credit rating issued by Moody’s

Investors Service.

Our vision is to satisfy all the financial needs of our

customers, help them succeed financially, be recognized as

the premier financial services company in our markets and

be one of America’s great companies. Our primary strategy

to achieve this vision is to increase the number of products

our customers buy from us and to give them all the financial

products that fulfill their needs. Our cross-sell strategy and

diversified business model facilitate growth in strong and

weak economic cycles, as we can grow by expanding the

number of products our current customers have with us. At

year-end 2005, our average cross-sell set new records for the

Company – our average retail banking household now has

4.8 products with us, up from 4.6 a year ago and our average

Wholesale Banking customer now has a record 5.7 products.

Our goal is eight products per customer, which is currently

half of our estimate of potential demand.

Our core products grew this year:

• Average loans grew by 10%;

• Average retail core deposits grew by 10%

(average core deposits grew by 9%); and

• Assets managed and administered were up 11%.

We believe it is important to maintain a well controlled

environment as we continue to grow our businesses. We

manage our credit risk by maintaining prudent credit policies

for underwriting with effective procedures for monitoring and

review. We have a well diversified loan portfolio, measured

by industry, geography and product type. We manage the

interest rate and market risks inherent in our asset and liability

balances within prudent ranges, while ensuring adequate

liquidity and funding. Our stockholder value has increased

over time due to customer satisfaction, strong financial results,

investment in our businesses and the prudent way we attempt

to manage our business risks.

Our financial results included the following:

Net income in 2005 increased 9% to $7.7 billion from

$7.0 billion in 2004. Diluted earnings per common share

increased 10% to $4.50 in 2005 from $4.09 in 2004. Return

on average total assets was 1.72% and return on average

common equity was 19.57% in 2005, and 1.71% and

19.56%, respectively, in 2004.

Net interest income on a taxable-equivalent basis was

$18.6 billion in 2005, compared with $17.3 billion a year

ago, reflecting solid loan growth (other than ARMs) and a

relatively flat net interest margin. Average earning assets

grew 8% from a year ago, or 15% excluding 1-4 family first

mortgages. Our net interest margin was 4.86% for 2005,

compared with 4.89% in 2004. Given the prospect of higher

short-term interest rates and a flatter yield curve, beginning in

second quarter 2004, as part of our asset/liability management

strategy, we sold the lowest-yielding ARMs on our balance

sheet, replacing some of these loans with higher-yielding ARMs.

At the end of 2005, new ARMs being held for investment

within real estate 1-4 family mortgage loans had yields

more than 1% higher than the average yield on the ARMs

sold since second quarter 2004.

Noninterest income increased 12% to $14.4 billion in

2005 from $12.9 billion in 2004. Double-digit growth in

noninterest income was driven by growth across our busi-

nesses, with particular strength in trust, investment and IRA

fees, card fees, loan fees, mortgage banking income and

gains on equity investments.

Revenue, the sum of net interest income and noninterest

income, increased 10% to a record $32.9 billion in 2005

from $30.1 billion in 2004 despite balance sheet reposition-

ing actions, including losses from the sales of low-yielding

ARMs and debt securities. For the year, Wells Fargo Home

Mortgage (Home Mortgage) revenue increased $455 million,

or 10%, from $4.4 billion in 2004 to $4.9 billion in 2005.

Operating leverage improved during 2005 with revenue

growing 10% and noninterest expense up only 8%.

Noninterest expense was $19.0 billion in 2005, up 8%

from $17.6 billion in 2004, primarily due to increased

mortgage production and continued investments in new

stores and additional sales-related team members. Noninterest

expense also included a $117 million expense to adjust the

estimated lives for certain depreciable assets, primarily building

improvements, $62 million of airline lease write-downs,

$56 million of integration expense and $25 million for the

adoption of FIN 47. We began expensing stock options,

as required, on January 1, 2006. Taking into account our

February 2006 option grant, we anticipate that total stock

option expense will reduce earnings by approximately

$.06 per share for 2006.

During 2005, net charge-offs were $2.28 billion, or .77%

of average total loans, compared with $1.67 billion, or .62%,

during 2004. Credit losses for 2005 included $171 million of

incremental fourth quarter bankruptcy losses and increased

losses of $163 million for first quarter 2005 initial

implementation of conforming to more stringent FFIEC

charge-off timing rules at Wells Fargo Financial. The provision

for credit losses was $2.38 billion in 2005, up $666 million

from $1.72 billion in 2004. The 2005 provision for credit

losses also included $100 million for estimated credit losses

related to Hurricane Katrina. The allowance for credit losses,

which consists of the allowance for loan losses and the

reserve for unfunded credit commitments, was $4.06 billion,

or 1.31% of total loans, at December 31, 2005, compared

with $3.95 billion, or 1.37%, at December 31, 2004.

At December 31, 2005, total nonaccrual loans were

$1.34 billion, or .43% of total loans, down from $1.36 billion,

or .47%, at December 31, 2004. Foreclosed assets were

$191 million at December 31, 2005, compared with

$212 million at December 31, 2004.