Wells Fargo 2005 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2005 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

46

Balance Sheet Analysis

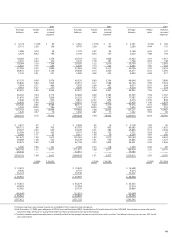

Table 6: Mortgage-Backed Securities

(in billions) Fair Net unrealized Remaining

value gain (loss) maturity

At December 31, 2005 $32.4 $ .4 5.3 yrs.

At December 31, 2005,

assuming a 200 basis point:

Increase in interest rates 29.9 (2.1) 7.5 yrs.

Decrease in interest rates 33.5 1.5 2.0 yrs.

Table 8: Deposits

(in millions) December 31,%

2005 2004 Change

Noninterest-bearing $ 87,712 $ 81,082 8%

Interest-bearing checking 3,324 3,122 6

Market rate and

other savings 134,811 126,648 6

Savings certificates 27,494 18,851 46

Core deposits 253,341 229,703 10

Other time deposits 46,488 36,622 27

Deposits in foreign offices 14,621 8,533 71

Total deposits $314,450 $274,858 14

Table 7: Maturities for Selected Loan Categories

(in millions) December 31, 2005

Within After After Total

one one year five

year through years

fiveyears

Selected loan maturities:

Commercial $18,748 $31,627 $11,177 $ 61,552

Other real estate mortgage 3,763 11,777 13,005 28,545

Real estate construction 5,081 6,887 1,438 13,406

Foreign 525 3,995 1,032 5,552

Total selected loans $28,117 $54,286 $26,652 $109,055

Sensitivity of loans due after

one year to changes in

interest rates:

Loans at fixed interest rates $11,145 $ 7,453

Loans at floating/variable

interest rates 43,141 19,199

Total selected loans $54,286 $26,652

2005 from $32.3 billion in 2004, due to higher origination

volume. Residential mortgage originations of $366 billion

were up 23% from $298 billion in 2004. Loans held for

sale decreased to $612 million at December 31, 2005, from

$8.7 billion a year ago, due to the transfer of student loans

held for sale to the held for investment portfolio. Our decision

to hold these loans for investment was based on present yields

and our intent and ability to hold this portfolio for the

foreseeable future.

Table 7 shows contractual loan maturities and interest

rate sensitivities for selected loan categories.

Deposits

Year-end deposit balances are in Table 8. Comparative

detail of average deposit balances is included in Table 3.

Average core deposits funded 54.5% and 54.4% of average

total assets in 2005 and 2004, respectively. Total average

interest-bearing deposits rose from $182.6 billion in 2004

to $194.6 billion in 2005. Total average noninterest-bearing

deposits rose from $79.3 billion in 2004 to $87.2 billion

in 2005. Savings certificates increased on average from

$18.9 billion in 2004 to $22.6 billion in 2005.

Securities Available for Sale

Our securities available for sale portfolio consists of both

debt and marketable equity securities. We hold debt

securities available for sale primarily for liquidity, interest

rate risk management and yield enhancement. Accordingly,

this portfolio primarily includes very liquid, high-quality

federal agency debt securities. At December 31, 2005, we held

$40.9 billion of debt securities available for sale, compared

with $33.0 billion at December 31, 2004, with a net unrealized

gain of $591 million and $1.2 billion for the same periods,

respectively. We also held $900 million of marketable equity

securities available for sale at December 31, 2005, and

$696 million at December 31, 2004, with a net unrealized

gain of $342 million and $189 million for the same

periods, respectively.

The weighted-average expected maturity of debt securities

available for sale was 5.9 years at December 31, 2005. Since

79% of this portfolio is mortgage-backed securities, the

expected remaining maturity may differ from contractual

maturity because borrowers may have the right to prepay

obligations before the underlying mortgages mature.

The estimated effect of a 200 basis point increase or

decrease in interest rates on the fair value and the expected

remaining maturity of the mortgage-backed securities

available for sale portfolio is shown in Table 6.

See Note 5 (Securities Available for Sale) to Financial

Statements for securities available for sale by security type.

Loan Portfolio

A comparative schedule of average loan balances is included

in Table 3; year-end balances are in Note 6 (Loans and

Allowance for Credit Losses) to Financial Statements.

Loans averaged $296.1 billion in 2005, compared with

$269.6 billion in 2004, an increase of 10%. Total loans at

December 31, 2005, were $310.8 billion, compared with

$287.6 billion at year-end 2004, an increase of 8%. Average

1-4 family first mortgages decreased $9.5 billion, or 11%,

and average junior liens increased $11.2 billion, or 25%, in

2005 compared with a year ago. Average commercial and

commercial real estate loans increased $12.0 billion, or 13%,

in 2005 compared with a year ago. Average mortgages held

for sale increased $6.7 billion, or 21%, to $39.0 billion in