Volvo 2013 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2013 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

|

|

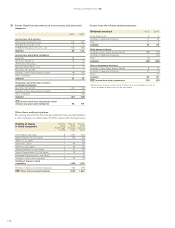

Goals and policies in fi nancial risk management (cont.)

CREDIT RISKS

Credit risks are defi ned as the risk that the Volvo Group does not receive

payment for recognized accounts receivable and customer-fi nancing

receivables (commercial credit risk), that the Volvo Group’s investments

are unable to be realized (fi nancial credit risk) and that potential profi t is

not realized due to the counterparty not fulfi lling its part of the contract

when using derivative instruments (fi nancial counterparty risk).

POLICY

The objective of the Volvo Group Credit Policy is to defi ne and measure

the credit exposure and control the risk of losses deriving from credits to

customers, credits to suppliers, counter party risks and Customer Dealer

Financing activities.

Commercial credit risk

The Volvo Group’s credit granting is steered by Group-wide policies and

customer-classifi cation rules. The credit portfolio should contain a distri-

bution among different customer categories and industries. The credit

risks are managed through active credit monitoring, follow-up routines and,

where applicable, product repossession. Moreover, regular monitoring

ensures that the necessary allowances are made for incurred losses on

doubtful receivables. In Notes 15 and 16, ageing analyses are presented of

customer fi nance receivables overdue and accounts receivables overdue

in relation to the reserves made.

The customer-fi nancing receivables in the Volvo Group’s customer-

fi nancing operations amounted at December 31, 2013 to approximately

net SEK 84 billion (81). The credit risk of this portfolio is distributed over

a large number of retail customers and dealers. Collaterals are provided in

the form of the fi nanced products. In the credit granting the Volvo Group

strives for a balance between risk exposure and expected return.

Read more about Volvo’s credit risk in the customer-fi nancing operation in

Note 15.

The Volvo Group’s accounts receivables amounted as of December 31,

2013 to approximately net SEK 29 billion (27).

Financial credit risk

The Volvo Group’s fi nancial assets are largely managed by Volvo Treasury

and invested in the money and capital markets. All investments must meet

the requirements of low credit risk and high liquidity. According to the Volvo

Group’s credit policy, counterparties for investments and derivative trans-

actions should have a rating better or equivalent to A from one of the

well-established credit rating institutions.

Liquid funds and marketable securites amounted as of December 31,

2013 to approximately SEK 30 billion (28).

Read more about Volvo Group’s Marketable securities and liquid funds in

Note 18.

Financial counterparty risk

The use of derivatives involves a counterparty risk, in that a potential gain

will not be realized if the counterparty fails to fulfi ll its part of the contract.

To reduce the exposure, the Volvo Group enters into master netting

agreements (primarily so called ISDA agreements) with all counterpart

eligible for derivative transactions. The netting agreements provide the

possibility for assets and liabilities to be set off under certain circum-

stances, such as in the case of the counterpart’s insolvency. These net-

ting agreements have no effect on profi t, loss or the position of the Volvo

Group, since derivative transactions are accounted for on a gross-basis,

with the exception of the derivatives described in footnote 3, under the

table on page 161 in note 30. Counterparty risk exposure for derivatives

is also limited through weekly cash transfers corresponding to the value

change of open contracts. The Volvo Group’s gross exposure from posi-

tive derivatives, amounting to SEK 3,713 M (5,148) is reduced by 41%

(43%) to SEK 2,203 M (2,948) by netting agreements and cash deposits,

so called CSA agreements. The Volvo Group is actively working with limits

per counterpart in order to reduce risk for high net amounts towards indi-

vidual counterparts.

Read more about the Volvo Group’s gross exposure from positive derivatives

per type of instrument in note 30 on page 163.

INTEREST-RATE RISKS CURRENCY RISKS CREDIT RISKS

FINANCIAL RISKS

OTHER PRICE RISKSLIQUIDITY RISKS

126

FINANCIAL INFORMATION 2013

126