Travelers 2011 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2011 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

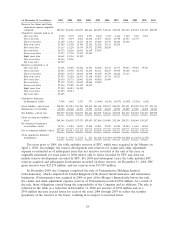

Geographic Distribution

The following table shows the geographic distribution of Personal Insurance’s direct written

premiums for the states that accounted for the majority of premium volume for the year ended

December 31, 2011:

% of

State Total

New York ................................................. 14.4%

Texas(1) ................................................... 8.0

Pennsylvania ................................................ 7.5

California .................................................. 6.5

Florida ................................................... 5.5

New Jersey ................................................ 5.0

Georgia ................................................... 4.5

Connecticut ................................................ 4.2

Massachusetts .............................................. 4.0

Virginia ................................................... 3.9

Maryland .................................................. 3.2

All others(2) ............................................... 33.3

Total ................................................... 100.0%

(1) The percentage for Texas includes business written by the Company through a fronting

agreement with another insurer.

(2) No other single state accounted for 3.0% or more of the total direct written premiums

written in 2011 by the Personal Insurance segment.

Competition

Although national companies write the majority of this business, Personal Insurance also faces

competition from many regional and hundreds of local companies. Personal Insurance primarily

competes based on service, ease of doing business, price, stability of the insurer and name recognition.

Personal Insurance competes for business within each independent agency since these agencies also

offer policies of competing companies. At the agency level, competition is primarily based on the level

of service, including claims handling, the level of automation and the development of long-term

relationships with individual agents, as well as on price. In recent years, many independent personal

insurance agents have begun utilizing price comparison rating technology, sometimes referred to as

‘‘comparative raters,’’ as a cost-efficient means of obtaining quotes from multiple companies.

Comparative raters tend to put additional focus on price over other competitive criteria. Personal

Insurance also competes with insurance companies that use exclusive agents or salaried employees to

sell their products, as well as those that employ direct marketing strategies, including the use of

toll-free numbers and the internet. Personal Insurance believes that its continued focus on underwriting

and pricing segmentation, claim settlement effectiveness strategies and expense management practices

enables it to price its products competitively in all of its distribution channels.

CLAIMS MANAGEMENT

The Company’s claim functions are managed through its Claims Services operation, with locations

in the United States and in the countries where it does business. With more than 13,000 employees,

Claims Services employs a diverse group of professionals, including claim adjusters, appraisers,

attorneys, investigators, engineers, accountants, system specialists and training, management and

support personnel. Approved external service providers, such as independent adjusters and appraisers,

investigators and attorneys, are available for use as appropriate.

16