Travelers 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

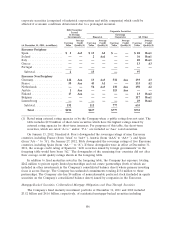

regulatory approval for changes to personal property and casualty insurance prices, as well as

competitive market conditions, may impact the timing and extent of renewal premium changes.

The pricing environment for new business generally has less of an impact on underwriting

profitability than renewal rate changes, given the volume of new business relative to renewal business.

Property and casualty insurance market conditions are expected to remain competitive during 2012 for

new business, not only in Business Insurance and Financial, Professional & International Insurance, but

also in Personal Insurance, where price comparison technology used by agents and brokers, sometimes

referred to as ‘‘comparative raters’’, has increased the focus on price over other competitive factors.

See ‘‘Risk Factors—The intense competition that we face could harm our ability to maintain or

increase our business volumes and our profitability.’’ In addition, the Company launched a new

distribution channel in 2009 that markets personal insurance products directly to consumers, which is

expected to generate modest growth in premium volume for Personal Insurance during 2012.

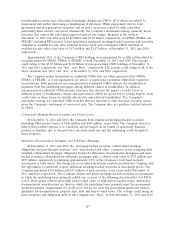

Current economic conditions have been somewhat volatile and there is increased uncertainty as to

whether the U.S. or the global economy will grow modestly, remain stagnant or enter a recession.

Economic growth experienced in 2011 may or may not continue, or may continue at a slower rate for

an extended period of time. In addition, some economic conditions, such as the commercial and

residential real estate environment and employment rates, may continue to be weak. If weak economic

conditions persist or deteriorate, the resulting low levels of economic activity could impact exposure

changes at renewal and the Company’s ability to write business at acceptable rates. Additionally, low

levels of economic activity could adversely impact audit premium adjustments, policy endorsements and

mid-term cancellations after policies are written. All of the foregoing, in turn, could adversely impact

net written premiums during 2012 and, since earned premiums lag net written premiums, earned

premiums could be adversely impacted during and following 2012.

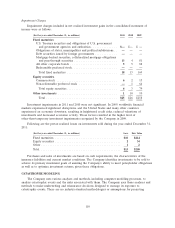

Underwriting Gain/Loss. The Company’s underwriting gain/loss can be significantly impacted by

catastrophe losses and net favorable or unfavorable prior year reserve development, as well as

underlying underwriting margins.

Catastrophe and other weather-related losses are inherently unpredictable from period to period.

The Company experienced significant catastrophe and other weather-related losses in 2011 which

adversely impacted its results of operations. The Company’s results of operations would continue to be

adversely impacted if significant catastrophe and other weather-related losses were to occur during

2012.

The Company utilizes a general catastrophe reinsurance treaty with unaffiliated reinsurers to

manage its exposure to losses resulting from catastrophes. In addition to the coverage provided under

this treaty, the Company also utilizes a catastrophe bond program, as well as a Northeast catastrophe

reinsurance treaty, to protect against certain losses resulting from catastrophes in the Northeastern

United States. For additional information regarding the Company’s catastrophe reinsurance program,

see ‘‘Item 1—Business—Reinsurance’’ in this report.

As discussed in more detail in Item 1, the attachment point for index-based losses and the

maximum limit of the Company’s catastrophe bond program are reset annually to maintain modeled

probabilities of attachment and expected loss on the respective catastrophe bonds equal to the initial

modeled probabilities of attachment and expected loss. For the period May 1, 2012 through April 30,

2013, the attachment point for the index-based losses and the maximum limit will be based on the new

version of the third-party proprietary computer model used to estimate potential hurricane losses for

the entire industry, discussed in ‘‘Item 7—Management’s Discussion and Analysis of Financial

Condition and Results of Operations—Catastrophe Modeling.’’ The Company estimates that the

attachment point for the index-based losses and the maximum limit on the reinsurance agreements in

the catastrophe bond program will increase by as much as 70%, reflecting increases in the third-party

model’s industry estimate of covered losses. The Company regularly reviews its catastrophe reinsurance

coverage and may seek additional catastrophe reinsurance coverage, either through general catastrophe

116