Travelers 2011 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2011 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

Discussion of Product Lines

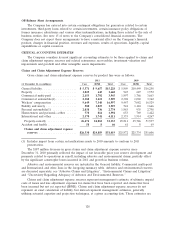

The following section details reserving considerations and common risk factors by product line.

There are many additional risk factors that may impact ultimate claim costs. Each risk factor presented

will have a different impact on required reserves. Also, risk factors can have offsetting or compounding

effects on required reserves. For example, in workers’ compensation, the use of expensive medical

procedures that result in medical cost inflation may enable workers to return to work faster, thereby

lowering indemnity costs. Thus, in almost all cases, it is impossible to discretely measure the effect of a

single risk factor and construct a meaningful sensitivity expectation.

In order to provide information on reasonably possible reserving changes by product line, the

historical changes in year-end claims and claim adjustment expense reserves over a one-year period are

provided for the U.S. product lines. This information is provided for both the Company and the

industry for the nine most recent years, and is based on the most recent publicly available data for the

reported line(s) that most closely match the individual product line being discussed. These changes

were calculated, net of reinsurance, from statutory annual statement data found in Schedule P of those

statements, and represent the reported reserve development on the beginning-of-the-year claim

liabilities divided by the beginning claim liabilities, all accident years combined, excluding non-defense

related claim adjustment expense. Data presented for the Company includes history for the entire

Travelers group (U.S. companies only), whether or not the individual subsidiaries were originally part of

SPC or TPC. This treatment is required by the statutory reporting instructions promulgated by state

regulatory authorities for Schedule P. Comparable data for non-U.S. companies is not available.

General Liability

General liability is generally considered a long tail line, as it takes a relatively long period of time

to finalize and settle claims from a given accident year. The speed of claim reporting and claim

settlement is a function of the specific coverage provided, the jurisdiction and specific policy provisions

such as self-insured retentions. There are numerous components underlying the general liability product

line. Some of these have relatively moderate payment patterns (with most of the claims for a given

accident year closed within 5 to 7 years), while others can have extreme lags in both reporting and

payment of claims (e.g., a reporting lag of a decade or more for ‘‘construction defect’’ claims).

While the majority of general liability coverages are written on an ‘‘occurrence’’ basis, certain

general liability coverages (such as those covering directors and officers or professional liability) are

typically insured on a ‘‘claims-made’’ basis.

General liability reserves are generally analyzed as two components: primary and excess/umbrella,

with the primary component generally analyzed separately for bodily injury and property damage.

Bodily injury liability payments reimburse the claimant for damages pertaining to physical injury as a

result of the policyholder’s legal obligation arising from non-intentional acts such as negligence, subject

to the insurance policy provisions. In some cases the damages can include future wage loss (which is a

function of future earnings power and wage inflation) and future medical treatment costs. Property

damage liability payments result from damages to the claimant’s private property arising from the

policyholder’s legal obligation for non-intentional acts. In most cases, property damage losses are a

function of costs as of the loss date, or soon thereafter. In addition, sizable or unique exposures are

reviewed separately. These exposures include asbestos, environmental, other mass torts, construction

defect, medical malpractice and large unique accounts that would otherwise distort the analysis. These

unique categories often require a very high degree of judgment and require reserve analyses that do

not rely on conventional actuarial methods.

134