Travelers 2011 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2011 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

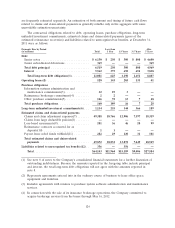

(5) Includes commitments to vendors entered into in the ordinary course of business for goods and

services including property, plant and equipment, office supplies, archival services, etc.

(6) Represents estimated timing for fulfilling unfunded commitments for private equity limited

partnerships and real estate partnerships.

(7) The amounts in ‘‘Claims and claim adjustment expenses’’ in the table above represent the

estimated timing of future payments for both reported and unreported claims incurred and related

claim adjustment expenses, gross of reinsurance recoverables, excluding structured settlements

expected to be paid by annuity companies.

The Company has entered into reinsurance agreements to protect itself from potential losses in

excess of the amount it is prepared to accept as described in note 5 of notes to the Company’s

consolidated financial statements.

In order to qualify for reinsurance accounting, a reinsurance agreement must indemnify the insurer

from insurance risk, i.e., the agreement must transfer amount and timing risk. Since the timing and

amount of cash inflows from such reinsurance agreements are directly related to the underlying

payment of claims and claim adjustment expenses by the insurer, reinsurance recoverables are

recognized in a manner consistent with the liabilities (the estimated liability for claims and claim

adjustment expenses) relating to the underlying reinsured contracts. The presence of any feature

that can delay timely reimbursement of claims by a reinsurer results in the reinsurance contract

being accounted for as a deposit rather than reinsurance (see below). The assumptions used in

estimating the amount and timing of the reinsurance recoverables are consistent with those used in

estimating the amount and timing of the related liabilities.

Reinsurance agreements that do not transfer both amount and timing risk are accounted for as

deposits and included in ‘‘Reinsurance contracts accounted for as deposits’’ in the table above.

The estimated future cash inflows from the Company’s reinsurance contracts that qualify for

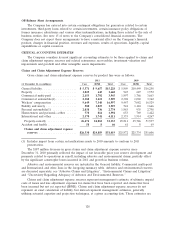

reinsurance accounting are as follows:

Less than After

(in millions) Total 1 Year 1-3 Years 3-5 Years 5 Years

Reinsurance recoverables .................. $7,453 $1,420 $1,770 $1,189 $3,074

The Company manages its business and evaluates its liabilities for claims and claim adjustment

expense on a net of reinsurance basis. The estimated cash flows on a net of reinsurance basis are

as follows:

Less than After

(in millions) Total 1 Year 1-3 Years 3-5 Years 5 Years

Claims and claim adjustment expenses, net ... $41,935 $9,346 $11,136 $6,208 $15,245

For business underwritten by non-U.S. operations, future cash flows related to reported and

unreported claims incurred and related claim adjustment expenses were translated at the spot rate

on December 31, 2011.

The amounts reported in the table above and in the table of reinsurance recoverables above are

presented on a nominal basis and have not been adjusted to reflect the time value of money.

Accordingly, the amounts above will differ from the Company’s balance sheet to the extent that

the liability for claims and claim adjustment expenses and the related reinsurance recoverables

have been discounted in the balance sheet. (See note 1 of notes to the Company’s consolidated

financial statements.)

(8) Workers’ compensation large deductible policies provide third party coverage in which the

Company typically is responsible for paying the entire loss under such policies and then seeks

reimbursement from the insured for the deductible amount. ‘‘Claims from large deductible

125