Travelers 2011 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2011 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

|

|

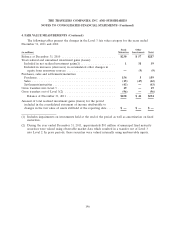

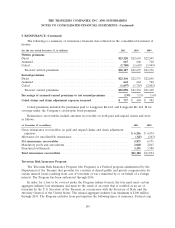

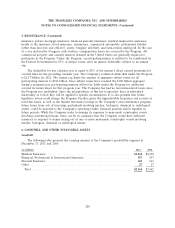

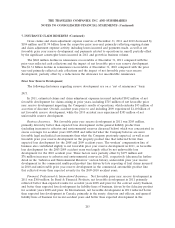

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

7. INSURANCE CLAIM RESERVES (Continued)

Asbestos Reserves. Because each policyholder presents different liability and coverage issues, the

Company generally reviews the exposure presented by each policyholder at least annually. Among the

factors which the Company may consider in the course of this review are: available insurance coverage,

including the role of any umbrella or excess insurance the Company has issued to the policyholder;

limits and deductibles; an analysis of the policyholder’s potential liability; the jurisdictions involved; past

and anticipated future claim activity and loss development on pending claims; past settlement values of

similar claims; allocated claim adjustment expense; potential role of other insurance; the role, if any, of

non-asbestos claims or potential non-asbestos claims in any resolution process; and applicable coverage

defenses or determinations, if any, including the determination as to whether or not an asbestos claim

is a products/completed operation claim subject to an aggregate limit and the available coverage, if any,

for that claim.

The Company’s quarterly asbestos reserve reviews include an analysis of exposure and claim

payment patterns by policyholder category, as well as recent settlements, policyholder bankruptcies,

judicial rulings and legislative actions. The Company also analyzes developing payment patterns among

policyholders in the Home Office, Field Office and Assumed Reinsurance and Other categories as well

as projected reinsurance billings and recoveries. In addition, the Company reviews its historical gross

and net loss and expense paid experience, year-by-year, to assess any emerging trends, fluctuations, or

characteristics suggested by the aggregate paid activity. Conventional actuarial methods are not utilized

to establish asbestos reserves nor have the Company’s evaluations resulted in any way of determining a

meaningful average asbestos defense or indemnity payment.

In the third quarter of 2011, the Company completed its annual in-depth asbestos claim review and

noted the following trends:

• continued high level of litigation activity involving individuals alleging serious asbestos-related

illness;

• an increase in severity for certain policyholders as a result of the continued high level of

litigation activity;

• stable payment patterns for a significant proportion of policyholders;

• a further decrease in the number of large asbestos exposures confronting the Company due to

additional settlement activity;

• continued moderate level of asbestos-related bankruptcy activity; and

• the absence of new theories of liability or new classes of defendants.

While the Company believes that over the past several years there has been a reduction in the

volatility associated with the Company’s overall asbestos exposure, there nonetheless remains a high

degree of uncertainty with respect to future exposure from asbestos claims.

As in prior years, the annual claim review considered active policyholders and litigation cases for

potential product and ‘‘non-product’’ liability. While the Home Office and Field Office categories,

which account for the vast majority of policyholders with active asbestos-related claims, experienced a

slight reduction in the number of policyholders with open asbestos claims compared with the prior year

period, gross asbestos-related payments in these categories increased slightly in 2011 compared with

2010. Payments on behalf of policyholders in these categories continue to be influenced by the high

206