Sallie Mae 2014 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2014 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

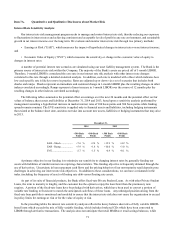

Item 7A. Quantitative and Qualitative Disclosures about Market Risk

Interest Rate Sensitivity Analysis

Our interest rate risk management program seeks to manage and control interest rate risk, thereby reducing our exposure

to fluctuations in interest rates and achieving consistent and acceptable levels of profit in any rate environment, and sustainable

growth in net interest income over the long term. We evaluate and monitor interest rate risk through two primary methods:

• Earnings at Risk (“EAR”), which measures the impact of hypothetical changes in interest rates on net interest income;

and

• Economic Value of Equity (“EVE”), which measures the sensitivity or change in the economic value of equity to

changes in interest rates.

A number of potential interest rate scenarios are simulated using our asset liability management system. The Bank is the

primary source of interest rate risk within the Company. The majority of the Bank’s assets are priced off of 1-month LIBOR.

Therefore, 1-month LIBOR is considered the core rate in our interest rate risk analysis with other interest rate changes

correlated to this rate through a detailed statistical analysis. In addition, each rate is modeled with a floor which indicates how

low each specific rate is likely to move in practice. Rates are adjusted up or down via a set of scenarios that includes both

shocks and ramps. Shocks represent an immediate and sustained change in 1-month LIBOR plus the resulting changes in other

indexes correlated accordingly. Ramps represent a linear increase in 1-month LIBOR over the course of 12 months plus the

resulting changes in other indexes correlated accordingly.

The following tables summarize the potential effect on earnings over the next 24 months and the potential effect on fair

values of balance sheet assets and liabilities at December 31, 2014 and 2013, based upon a sensitivity analysis performed by

management assuming a hypothetical increase in market interest rates of 100 basis points and 300 basis points while funding

spreads remain constant. The EVE sensitivity is applied only to financial assets and liabilities, including hedging instruments

that existed at the balance sheet date, and does not take into account new assets, liabilities or hedging instruments that may arise

in 2015.

December 31,

2014

2013

+300 Basis

Points

+100 Basis

Points

+300 Basis

Points

+100 Basis

Points

EAR - Shock ................

+7.6

%

+2.4

%

+12.9

%

+4.2

%

EAR - Ramp .................

+5.9

%

+1.8

%

+10.0

%

+3.0

%

EVE ............................

-2.7

%

-1.5

%

-0.4

%

+0.1

%

A primary objective in our funding is to minimize our sensitivity to changing interest rates by generally funding our

assets with liabilities of similar interest rate repricing characteristics. This funding objective is frequently obtained through the

use of derivatives. Uncertainty in loan repayment cash flows and the pricing behavior of our non-maturity retail deposits pose

challenges in achieving our interest rate risk objectives. In addition to these considerations, we can have a mismatch in the

index (including the frequency of reset) of floating rate debt versus floating rate assets.

As part of its suite of financial products, the Bank offers fixed-rate Private Student Loans. As with other Private Student

Loans, the term to maturity is lengthy, and the customer has the option to repay the loan faster than the promissory note

requires. A portion of the fixed-rate loans have been hedged with derivatives, which have been used to convert a portion of

variable rate funding to fixed-rate to match the anticipated cash flows of these loans. Any unhedged position arising from the

fixed-rate loan portfolio is monitored and modeled to ensure that the interest rate risk does not cause the organization to exceed

its policy limits for earnings at risk or for the value of equity at risk.

In the preceding tables the interest rate sensitivity analysis reflects the heavy balance sheet mix of fully variable LIBOR-

based loans which exceeds the mix of fully variable funding, which includes brokered CDs which have been converted to

LIBOR through derivative transactions. The analysis does not anticipate that retail MMDA or retail savings balances, while

71