Sallie Mae 2014 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2014 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

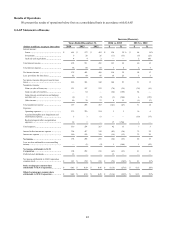

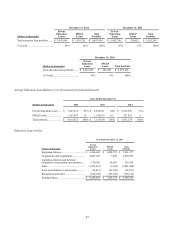

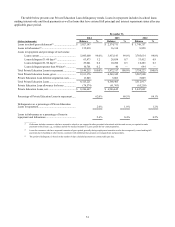

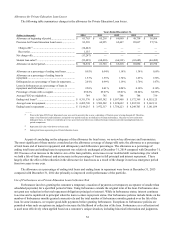

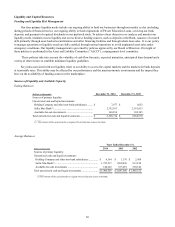

Allowance for Private Education Loan Losses

The following table summarizes changes in the allowance for Private Education Loan losses.

Years Ended December 31,

(Dollars in thousands)

2014

2013

2012

2011

2010

Allowance at beginning of period .................................

$

61,763

$

65,218

$

69,090

$

49,738

$

38,504

Provision for Private Education Loan losses ..................

83,583

64,955

62,447

85,037

57,716

Charge-offs(1) ..........................................................

(14,442

)

—

—

—

—

Recoveries ..............................................................

1,155

—

—

—

—

Net charge-offs...........................................................

(13,287

)

—

—

—

—

Student loan sales(2) ....................................................

(53,485

)

(68,410

)

(66,319

)

(65,685

)

(46,482

)

Allowance at end of period ..........................................

$

78,574

$

61,763

$

65,218

$

69,090

$

49,738

Allowance as a percentage of ending total loans ............

0.95

%

0.94

%

1.18

%

1.34

%

1.09

%

Allowance as a percentage of ending loans in

repayment ..................................................................

1.53

%

1.55

%

1.74

%

1.63

%

1.56

%

Delinquencies as a percentage of loans in repayment ......

2.01

%

0.99

%

1.19

%

1.70

%

1.47

%

Loans in forbearances as a percentage of loans in

repayment and forbearance ..........................................

2.56

%

0.41

%

0.24

%

0.10

%

0.10

%

Percentage of loans with a cosigner ..............................

89.82

%

89.87

%

89.81

%

88.84

%

82.55

%

Average FICO at origination ........................................

749

745

746

748

739

Ending total loans(3) ....................................................

$

8,311,376

$

6,563,342

$

5,507,908

$

5,172,369

$

4,555,125

Average loans in repayment .........................................

$

4,495,709

$

3,509,502

$

3,928,692

$

3,832,531

$

2,162,131

Ending loans in repayment ..........................................

$

5,149,215

$

3,972,317

$

3,750,223

$

4,249,703

$

3,181,039

_______

(1) Prior to the Spin-Off, Private Education Loans were sold to an entity that is now a subsidiary of Navient, prior to being charged off. Therefore,

many of our historical credit indicators and period-over-period trends are not indicative of future performance. Because we now retain more

delinquent loans, we believe it could take up to two years from now before our credit performance indicators provide meaningful period-over-

period comparisons.

(2) Represents fair value write-downs on loans sold.

(3) Ending total loans represents gross Private Education Loans.

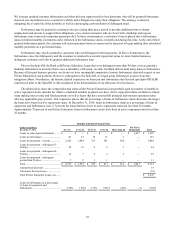

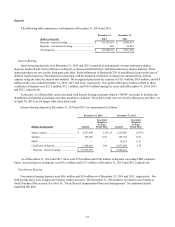

As part of concluding on the adequacy of the allowance for loan losses, we review key allowance and loan metrics.

The most significant of these metrics considered are the allowance coverage of charge-offs ratio; the allowance as a percentage

of total loans and of loans in repayment; and delinquency and forbearance percentages. The allowance as a percentage of

ending total loans and ending loans in repayment was relatively unchanged at December 31, 2014 compared with December 31,

2013 because of an increase in the relative size of the loan portfolio, an increase in our troubled debt restructurings (for which

we hold a life-of-loan allowance) and an increase in the percentage of loans in full principal and interest repayment. These

largely offset the effect of the reduction in the allowance for loan losses as a result of the change in our loss emergence period

from two years to one year.

The allowance as a percentage of ending total loans and ending loans in repayment were lower at December 31, 2013

compared with December 31, 2012 due primarily to improved credit performance of the portfolio.

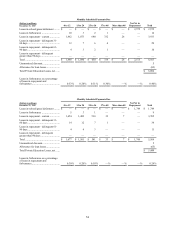

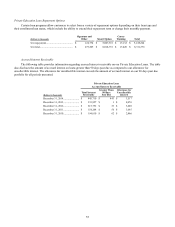

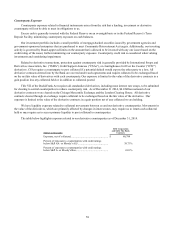

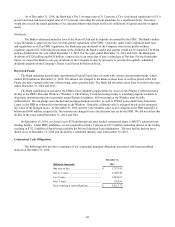

Use of Forbearance as a Private Education Loan Collection Tool

Forbearance involves granting the customer a temporary cessation of payments (or temporary acceptance of smaller than

scheduled payments) for a specified period of time. Using forbearance extends the original term of the loan. Forbearance does

not grant any reduction in the total repayment obligation (principal or interest). While in forbearance status, interest continues

to accrue and is capitalized to principal when the loan re-enters repayment status. Our forbearance policies include limits on the

number of forbearance months granted consecutively and the total number of forbearance months granted over the life of the

loan. In some instances, we require good-faith payments before granting forbearance. Exceptions to forbearance policies are

permitted when such exceptions are judged to increase the likelihood of collection of the loan. Forbearance as a collection tool

is used most effectively when applied based on a customer’ s unique situation, including historical information and judgments.

52