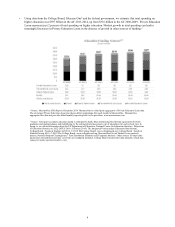

Sallie Mae 2014 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2014 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

We must comply with the FDIC’s final rule implementing the Basel III capital framework related to regulatory capital

measurement and reporting. The rule strengthens both the quantity and quality of risk-based capital for all banks, placing

greater emphasis on Tier 1 common equity capital. Under the new rule, well-capitalized institutions will be required to maintain

a minimum Tier 1 Leverage ratio of 5 percent, a minimum Tier 1 common equity risk-based capital ratio of 6.5 percent, a

minimum Tier 1 risk-based capital of 8 percent and minimum total risk-based capital of 10 percent. In addition, a capital

conservation buffer will be phased in over four years beginning on January 1, 2016, as follows: the maximum buffer will be

0.625 percent of risk weighted assets for 2016, 1.25 percent for 2017, 1.875 percent for 2018 and 2.5 percent for 2019 and

beyond, resulting in the following minimum ratios beginning in 2019: a Tier 1 common equity risk-based capital ratio of a

minimum 7.0 percent, a Tier 1 capital ratio of a minimum 8.5 percent and a total risk-based capital ratio of a minimum 10.5

percent.

Stress Testing Requirements

The Dodd-Frank Act imposes stress testing requirements on banking organizations with total consolidated assets,

averaged over the four most recent consecutive quarters, of more than $10 billion. As of September 30, 2014, the Bank has met

this asset threshold. Under the FDIC’s implementing regulations, the Bank is required to conduct annual company-run stress

tests utilizing scenarios provided by the FDIC and publish a summary of those results. The Bank must conduct its first annual

stress test under the rules in the January 1, 2016 stress testing cycle and submit the results of that stress test to the FDIC by July

31, 2016.

Deposit Insurance and Assessments

Deposits at the Bank are insured by the Deposit Insurance Fund (the “DIF”), as administered by the FDIC, up to the

applicable limits established by law. The Dodd-Frank Act amended the statutory regime governing the DIF. Among other

things, the Dodd-Frank Act established a minimum designated reserve ratio (“DRR”) of 1.35 percent of estimated insured

deposits, required that the fund reserve ratio reach 1.35 percent by September 30, 2020, and directed the FDIC to amend its

regulations to redefine the assessment base used for calculating deposit insurance assessments. Specifically, the Dodd-Frank

Act requires the assessment base to be an amount equal to the average consolidated total assets of the insured depository

institution during the assessment period, minus the sum of the average tangible equity of the insured depository institution

during the assessment period and an amount the FDIC determines is necessary to establish assessments consistent with the risk-

based assessment system found in the FDIA.

In December of 2010, the FDIC adopted a final rule setting the DRR at 2.0 percent. Furthermore, on February 7, 2011,

the FDIC issued a final rule changing its assessment system from one based on domestic deposits to one based on the average

consolidated total assets of a bank minus its average tangible equity during each quarter. The February 7, 2011 final rule

modifies two adjustments added to the risk-based pricing system in 2009 (an unsecured debt adjustment and a brokered deposit

adjustment), discontinues a third adjustment added in 2009 (the secured liability adjustment), and adds an adjustment for long-

term debt held by an insured depository institution where the debt is issued by another insured depository institution. Under the

February 7, 2011 final rule, the total base assessment rates will vary depending on the DIF reserve ratio.

With respect to brokered deposits, an insured depository institution must be well-capitalized in order to accept, renew or

roll over such deposits without FDIC clearance. An adequately capitalized insured depository institution must obtain a waiver

from the FDIC to accept, renew or roll over brokered deposits. Undercapitalized insured depository institutions generally may

not accept, renew or roll over brokered deposits. For more information on the Bank’s deposits, see Item 7. “Management's

Discussion and Analysis of Financial Condition and Results of Operations - Key Financial Measures — Funding Sources”.

Regulatory Examinations

The Bank currently undergoes regular on-site examinations by the Bank’s regulators, which examine for adherence to a

range of legal and regulatory compliance responsibilities. A regulator conducting an examination has complete access to the

books and records of the examined institution. The results of the examination are confidential. The cost of examinations may be

assessed against the examined institution as the agency deems necessary or appropriate.

13