Sallie Mae 2014 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2014 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

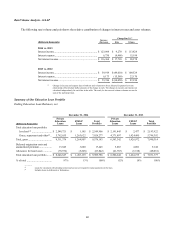

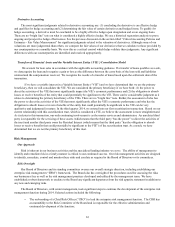

We leverage updated customer information and other decision support tools to best determine who will be granted forbearance

based on our expectations as to a customer’s ability and willingness to repay their obligation. This strategy is aimed at

mitigating the overall risk of the portfolio as well as encouraging cash resolution of delinquent loans.

Forbearance may be granted to customers who are exiting their grace period to provide additional time to obtain

employment and income to support their obligations, or to current customers who are faced with a hardship and request

forbearance time to provide temporary payment relief. In these circumstances, a customer’s loan is placed into a forbearance

status in limited monthly increments and is reflected in the forbearance status at month-end during this time. At the end of their

granted forbearance period, the customer will enter repayment status as current and is expected to begin making their scheduled

monthly payments on a go-forward basis.

Forbearance may also be granted to customers who are delinquent in their payments. In these circumstances, the

forbearance cures the delinquency and the customer is returned to a current repayment status. In more limited instances,

delinquent customers will also be granted additional forbearance time.

Prior to the Spin-Off, the Bank sold Private Education Loans that were delinquent more than 90 days or were granted a

hardship forbearance to an entity that is now a subsidiary of Navient. As such, the Bank did not hold many loans in forbearance.

Because of this past business practice, we do not yet have meaningful comparative historic forbearance data with respect to our

Private Education Loan portfolio. However, subsequent to the Spin-Off, we began using forbearance as part of our loss

mitigation efforts. Nonetheless, the historic default experience on loans put into forbearance that Navient (pre-Spin-Off SLM)

experienced prior to the Spin-Off is still considered in the determination of our allowance for loan losses.

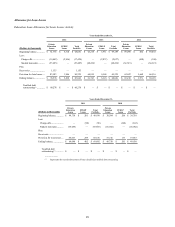

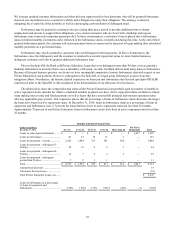

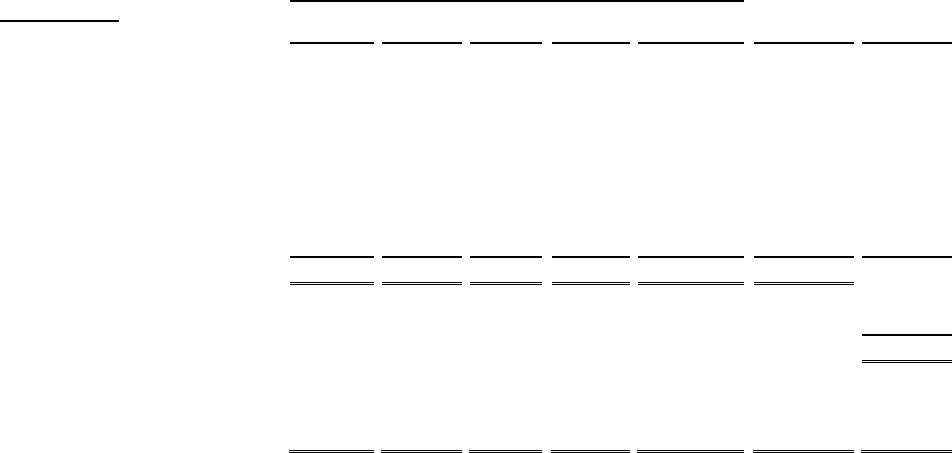

The tables below show the composition and status of the Private Education Loan portfolio aged by number of months in

active repayment status (months for which a scheduled monthly payment was due). Active repayment status includes in-school

loans making interest only and fixed payments as well as loans that have entered full principal and interest repayment status

after any applicable grace period. Our experience shows that the percentage of loans in forbearance status decreases the longer

the loans have been in active repayment status. At December 31, 2014, loans in forbearance status as a percentage of loans in

repayment and forbearance were 2.7 percent for loans that have been in active repayment status for less than 25 months.

Approximately 78 percent of our Private Education Loans in forbearance status have been in active repayment status less than

25 months.

(Dollars in millions)

December 31, 2014

Monthly Scheduled Payments Due

Not Yet in

Repayment

Total

0 to 12

13 to 24

25 to 36

37 to 48

More than 48

Loans in-school/grace/deferment .........

$

—

$

—

$

—

$

—

$

—

$

3,027

$

3,027

Loans in forbearance ..........................

82

23

16

11

3

—

135

Loans in repayment - current ..............

2,242

1,484

725

391

204

—

5,046

Loans in repayment - delinquent 31-

60 days .............................................

30

16

9

6

3

—

64

Loans in repayment - delinquent 61-

90 days .............................................

14

7

4

2

2

—

29

Loans in repayment - delinquent

greater than 90 days ...........................

7

2

1

1

—

—

11

Total .................................................

$

2,375

$

1,532

$

755

$

411

$

212

$

3,027

8,312

Unamortized discount ........................

14

Allowance for loan losses ...................

(79

)

Total Private Education Loans, net.......

$

8,247

Loans in forbearance as a percentage

of loans in repayment and

forbearance .......................................

3.45

%

1.50

%

2.12

%

2.68

%

1.42

%

—

%

2.55

%

53