Sallie Mae 2014 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2014 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, unless otherwise noted)

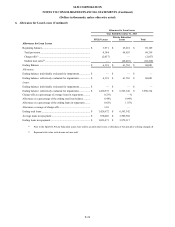

10. Borrowed Funds

We maintain discretionary uncommitted Federal Funds lines of credit with various correspondent banks, which totaled

$100,000 at December 31, 2014. The interest rate charged to the Company on these lines of credit is priced at Fed Funds plus a

spread at the time of borrowing, and is payable daily. We did not utilize these lines of credit in 2014, 2013 and 2012.

We established an account at the FRB to meet eligibility requirements for access to the Primary Credit borrowing facility

at the FRB’s Discount Window (“Window”). All borrowings at the Window must be fully collateralized. We pledged asset-

backed and mortgage-backed securities, as well as FFELP Loans and Private Education Loans to the FRB as collateral for

borrowings at the Window. Generally, collateral value is assigned based on the estimated fair value of the pledged assets. At

December 31, 2014 and 2013, the lendable value of our collateral at the FRB totaled $1,398,286 and $900,217, respectively.

The interest rate charged to us is the discount rate set by the FRB. We did not utilize this facility in 2014 and 2013.

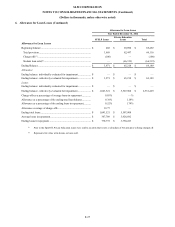

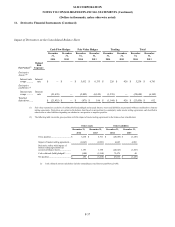

11. Derivative Financial Instruments

Risk Management Strategy

We maintain an overall interest rate risk management strategy that incorporates the use of derivative instruments to

minimize the economic effect of interest rate changes. Our goal is to manage interest rate sensitivity by modifying the repricing

frequency and underlying index characteristics of certain balance sheet liabilities so the net interest margin is not, on a material

basis, adversely affected by movements in interest rates. As a result of interest rate fluctuations, hedged liabilities will

appreciate or depreciate in market value or create variability in cash flows. Income or loss on the derivative instruments that are

linked to the hedged item will generally offset the effect of this unrealized appreciation or depreciation or volatility in cash

flows for the period the item is being hedged. We view this strategy as a prudent management of interest rate risk.

Although we use derivatives to offset (or minimize) the risk of interest rate changes, the use of derivatives does expose us

to both market and credit risk. Market risk is the chance of financial loss resulting from changes in interest rates and market

liquidity. Credit risk is the risk that a counterparty will not perform its obligations under a contract and it is limited to the loss of

the fair value gain in a derivative that the counterparty owes us less collateral held or plus collateral posted. When the fair value

of a derivative contract less collateral held or plus collateral posted is negative, we owe the counterparty and, therefore, we have

no credit risk exposure to the counterparty; however, the counterparty has exposure to us. We minimize the credit risk in

derivative instruments by entering into transactions with highly rated counterparties that are reviewed regularly by our Credit

Department. We also maintain a policy of requiring that all derivative contracts be governed by an International Swaps and

Derivative Association Master Agreement. Depending on the nature of the derivative transaction, bilateral collateral

arrangements generally are required as well. When we have more than one outstanding derivative transaction with the

counterparty, and there exists legally enforceable netting provisions with the counterparty (i.e., a legal right to offset receivable

and payable derivative contracts), the “net” mark-to-market exposure, less collateral held or plus collateral posted, represents

exposure with the counterparty. When there is a net negative exposure, we consider our exposure to the counterparty to be zero.

At December 31, 2014 and 2013, we had a net positive exposure (derivative gain positions to us less collateral which has been

posted by counterparties to us) related to derivatives of $60,784 and $3,517, respectively.

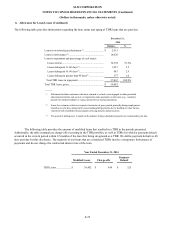

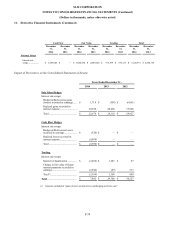

Accounting for Derivative Instruments

Derivative instruments that are used as part of our interest rate risk management strategy are interest rate swaps. The

accounting for derivative instruments requires that every derivative instrument, including certain derivative instruments

embedded in other contracts, be recorded on the balance sheet as either an asset or liability measured at fair value. Our

derivative instruments are classified and accounted for by us as fair value hedges and cash flow hedges.

Fair Value Hedges

Fair value hedges are generally used by us to hedge the exposure to changes in fair value of a recognized fixed-rate

liability. We enter into interest rate swaps to economically convert fixed-rate debt into variable rate debt. For fair value hedges,

F-35