Rogers 2012 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2012 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

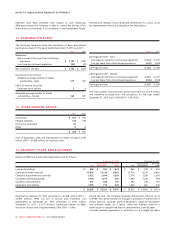

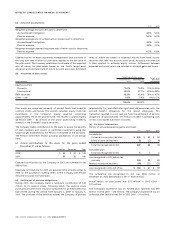

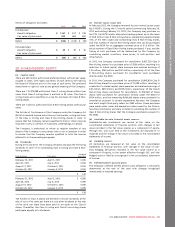

(a) Actuarial assumptions:

2012 2011

Weighted average discount rate used to determine:

Accrued benefit obligation 4.5% 5.5%

Pension expense 5.5% 6.0%

Weighted average rate of compensation increase used to determine:

Accrued benefit obligation 3.0% 3.0%

Pension expense 3.0% 3.0%

Weighted average expected long-term rate of return used to determine:

Pension expense 6.7% 6.8%

Expected return on assets represents management’s best estimate of

the long-term rate of return on plan assets applied to the fair value of

the plan assets. The Company establishes its estimate of the expected

rate of return on plan assets based on the fund’s target asset

allocation and estimated rate of return for each asset class. Estimated

rates of return are based on expected returns from fixed income

securities that take into account bond yields. An equity risk premium

is then applied to estimate equity returns. Differences between

expected and actual return are included in actuarial gains and losses.

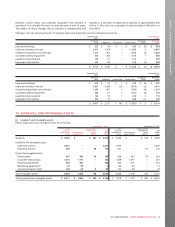

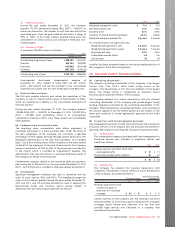

(b) Allocation of plan assets:

Percentage of plan assets Target asset

allocation

percentageAsset category December 31,

2012 December 31,

2011

Equity securities:

Domestic 19.3% 19.0% 10% to 29%

International 38.3% 37.7% 29% to 48%

Debt securities 41.8% 42.4% 38% to 47%

Other – cash 0.6% 0.9% 0% to 2%

100.0% 100.0%

Plan assets are comprised primarily of pooled funds that invest in

common stocks and bonds. The pooled Canadian equity fund has

investments in the Company’s equity securities comprising

approximately 1% of the pooled fund. This results in approximately

$2 million (2011 – $1 million) of the plans’ assets being indirectly

invested in the Company’s equity securities.

The Company makes contributions to the plans to secure the benefits

of plan members and invests in permitted investments using the

target ranges established by the Pension Committee of the Company.

The Pension Committee reviews actuarial assumptions on an annual

basis.

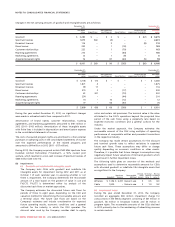

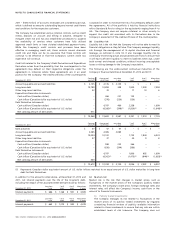

(c) Actual contributions to the plans for the years ended

December 31 are as follows:

Employer Employee Total

2012 $ 85 $ 23 $ 108

2011 80 20 100

Expected contributions by the Company in 2013 are estimated to be

$96 million.

Employee contributions for 2013 are assumed to be at levels similar to

2012 on the assumption staffing levels in the Company will remain

the same on a year-over-year basis.

(d) Settlement of pension obligations:

During 2011, the Company made a lump-sum contribution of $18

million to its pension plans, following which the pension plans

purchased annuities from insurance companies for all employees who

had retired during the period from January 1, 2009 to January 1,

2011. The purchase of the annuities relieves the Company of primary

responsibility for, and eliminates significant risk associated with, the

accrued benefit obligations for the retired employees. This

transaction resulted in a non-cash loss from the settlement of pension

obligations of approximately $11 million recorded in operating costs

on the consolidated statement of income.

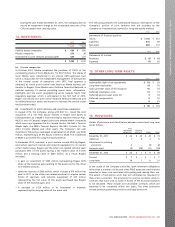

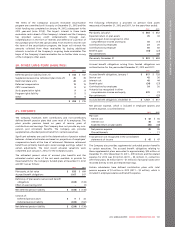

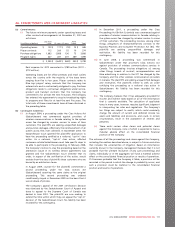

(e) Historical information:

History of annual experience (gains) and losses:

2012 2011 2010

Funded plan:

Actuarial loss on plan liabilities $ 240 $90$82

Effect of asset ceiling limit (1) (2) (4)

Total loss recognized in OCI 239 88 78

Unfunded plan:

Total loss recognized in OCI 512

Loss recognized in OCI, before tax

recovery 244 89 80

Related income tax recovery (64) (22) (21)

Loss recognized in OCI, net of tax $ 180 $67$59

The cumulative loss recognized in OCI was $306 million at

December 31, 2012 (December 31, 2011 – $126 million).

Actual return on plan assets was $75 million in 2012 (2011 –

$27 million).

The Company’s experience loss on funded plan liabilities was $50

million in 2012 (2011 – $16 million). The Company’s experience loss on

unfunded plan liabilities was $nil in 2012 (2011 – $1 million).

108 ROGERS COMMUNICATIONS INC. 2012 ANNUAL REPORT