Rogers 2012 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2012 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

routinely engage in risk management practices such as hedging,

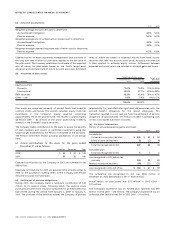

derivatives or short selling with respect to its publicly traded

investments.

At December 31, 2012, a $1 change in the market price per share

of the Company’s publicly traded investments would have

resulted in a $14 million change in the Company’s other

comprehensive income, net of income taxes of $2 million.

(ii) Stock-based compensation:

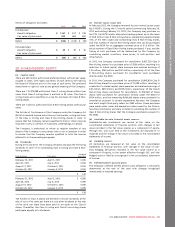

The liability related to stock-based compensation is marked-to-

market each period, and stock based compensation expense is

impacted by the change in the price of the Company’s Class B

Non-Voting shares during the life of an award, including SARs,

RSUs and DSUs.

At December 31, 2012, a $1 change in the market price of the

Company’s Class B Non-Voting shares would have resulted in a

change of $6 million in net income.

The Company may use derivatives from time to time to manage

its exposure to fluctuations with its stock-based compensation

expense.

(iii) Foreign exchange and interest rates:

The Company uses derivative financial instruments to manage its

risks from fluctuations in foreign exchange and interest rates

associated with its U.S. dollar denominated debt instruments. All

such agreements are used for risk management purposes only

and are designated as hedges of specific debt instruments for

economic purposes. The Company also uses derivative financial

instruments to manage the foreign exchange risk in its

operations. All such agreements are used for risk management

purposes only, and, in certain cases, are designated as hedges for

certain of the Company’s operational expenditures. The

Company does not use derivative instruments for speculative

purposes. From time to time, these derivative financial

instruments include cross-currency interest rate exchange

agreements, foreign exchange forward contracts and foreign

exchange option agreements.

At December 31, 2012, all of the Company’s long-term debt was

at fixed interest rates excluding the credit facility.

U.S. $350 million of the Company’s U.S. dollar-denominated

long-term debt instruments are not hedged for accounting

purposes and, therefore, a one cent change in the Canadian

dollar relative to the U.S. dollar would have resulted in a

$4 million change in the carrying value of long-term debt at

December 31, 2012. In addition, this would have resulted in a

$3 million change in net income, net of income taxes of

$1 million. There would have been a similar, offsetting change in

the carrying value of the associated U.S. $350 million of Debt

Derivatives with a similar offsetting impact on net income.

In July 2011, the Company entered into foreign exchange

forward contracts to manage foreign exchange risk on certain

forecasted expenditures. All of these Expenditure Derivatives

were accounted for as hedges during the year ended

December 31, 2012, with changes in fair value being recorded in

the hedging reserve, a component of equity. The Expenditure

Derivatives fix the exchange rate on an aggregate U.S. $20

million per month of the Company’s forecast expenditures at an

average exchange rate of C$0.9643/U.S.$1 from August 2011

through July 2014. At December 31, 2012, U.S. $380 million of

these Expenditure Derivatives remain outstanding.

A portion of the Company’s accounts receivable and accounts

payable and accrued liabilities is denominated in U.S. dollars;

however, due to their short-term nature, there is no significant

market risk arising from fluctuations in foreign exchange rates.

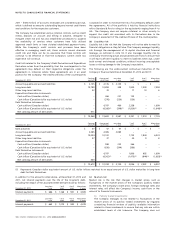

(d) Derivative instruments:

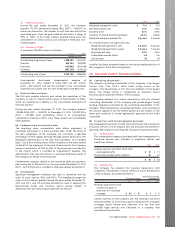

At December 31, 2012, 91.7% of the Company’s U.S. dollar-

denominated long-term debt instruments were hedged against

fluctuations in foreign exchange rates for accounting purposes. At

December 31, 2012, details of the Derivatives net liability position are

as follows:

December 31, 2012 U.S. $

notional Exchange

rate Cdn. $

notional Fair

value

Debt Derivatives accounted

for as cash flow hedges:

As assets $ 1,600 1.0252 $ 1,640 $ 34

As liabilities 2,280 1.2270 2,798 (561)

Debt Derivatives not

accounted for as hedges:

As assets 350 1.0258 359 3

Net mark-to-market liability

Debt Derivatives (524)

Expenditure Derivatives

accounted for as cash flow

hedges:

As assets 380 0.9643 366 13

Net mark-to-market liability $ (511)

The net mark-to-market derivative liability of the Derivatives is

comprised of:

2012 2011

Current asset $8$16

Long-term asset 42 64

50 80

Current liability (144) (37)

Long-term liability (417) (503)

(561) (540)

Net mark-to-market liability $ (511) $ (460)

In 2012, a $4 million decrease in estimated fair value (2011 – $6

million increase) related to hedge ineffectiveness was recognized in

net income.

2012 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 105