Rogers 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

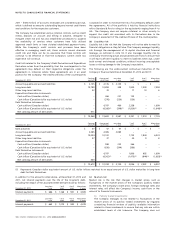

repayment of the Senior Notes aggregating $57 million, including

redemption premiums of $49 million and a net loss on the

termination of the associated Debt Derivatives of $8 million.

Concurrent with this redemption, on March 21, 2011, the Company

terminated the associated U.S. $470 million notional principal

amount of Debt Derivatives, resulting in a payment of approximately

$111 million.

As a result of these redemptions, the Company paid approximately

$878 million, including approximately $802 million principal amount

and $76 million for the premiums incurred in connection with the

redemptions. In addition, concurrent with the redemptions, the

Company terminated the associated U.S. $820 million notional

principal amount of Debt Derivatives, resulting in a payment of

approximately $330 million.

The total loss on repayment of the Senior Notes was $99 million and

recorded in finance costs for the year ended December 31, 2011.

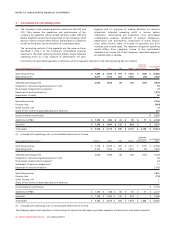

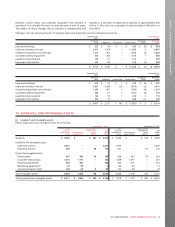

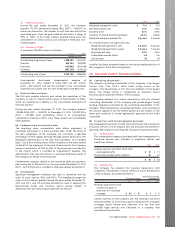

(e) Principal repayments:

As at December 31, 2012, principal repayments due within each of the

next five years and thereafter on all long-term debt are as follows:

2013 $ 348

2014 1,094

2015 826

2016 1,000

2017 500

Thereafter 7,090

$ 10,858

(f) Foreign exchange:

During 2012, foreign exchange gains related to the translation of

long-term debt recorded in the consolidated statements of income

totalled $9 million (2011 – $6 million loss).

(g) Weighted average interest rate:

The Company’s effective weighted average rate on all long-term

debt, as at December 31, 2012, including the effect of all of the

associated Debt Derivative instruments, was 6.06% (2011 – 6.22%).

(h) Terms and conditions:

The provisions of the Company’s $2.0 billion bank credit facility

described earlier impose certain restrictions on the operations and

activities of the Company, the most significant of which are leverage

related maintenance tests.

In addition, certain of the Company’s Senior Notes and Senior

Debentures described earlier (including the 6.25% Senior Notes due

2013 and 8.75% Senior Debentures due 2032) contain debt incurrence

tests as well as restrictions upon additional investments, sales of assets

and payment of dividends, all of which are suspended in the event

the public debt securities are assigned investment grade ratings by at

least two of three specified credit rating agencies. As at December 31,

2012, all of these public debt securities were assigned an investment

grade rating by each of the three specified credit rating agencies and,

accordingly, these restrictions have been suspended for so long as

such investment grade ratings are maintained. The Company’s other

Senior Notes do not contain any such restrictions, regardless of the

related credit ratings.

In addition to the foregoing, the repayment dates of certain debt

agreements may be accelerated if there is a change in control of the

Company.

At December 31, 2012 and 2011, the Company was in compliance with

all financial covenants, financial ratios and all the terms and

conditions of its long-term debt agreements.

18. CAPITAL RISK MANAGEMENT:

The Company’s objectives in managing capital are to ensure sufficient

liquidity to pursue its strategy of organic growth combined with

strategic acquisitions to provide returns to its shareholders. The

Company defines capital that it manages as shareholders’ equity

(which is comprised of issued capital, share premium, retained

earnings, hedging reserve and available-for-sale financial assets

reserve) and long-term debt.

The Company manages its capital structure and makes adjustments to

it in light of general economic conditions, the risk characteristics of

the underlying assets and the Company’s working capital

requirements. In order to maintain or adjust its capital structure, the

Company, upon approval from its Board of Directors, may issue or

repay long-term debt, issue shares, repurchase shares, pay dividends

or undertake other activities as deemed appropriate under the

specific circumstances. The Board of Directors reviews and approves

any material transactions out of the ordinary course of business,

including proposals on acquisitions or other major investments or

divestitures, as well as annual capital and operating budgets.

The Company monitors debt leverage ratios as part of the

management of liquidity and shareholders’ return and to sustain

future development of the business.

The Company is not subject to externally imposed capital

requirements and its overall strategy with respect to capital risk

management remains unchanged from the year ended December 31,

2011.

19. FINANCIAL RISK MANAGEMENT AND

FINANCIAL INSTRUMENTS:

The Company is exposed to credit risk, liquidity risk and market risk.

The Company’s primary risk management objective is to protect its

income and cash flows and, ultimately, shareholder value. Risk

management strategies, as discussed below, are designed and

implemented to ensure the Company’s risks and the related exposures

are consistent with its business objectives and risk tolerance.

(a) Credit risk:

Credit risk represents the financial loss that the Company would

experience if a counterparty to a financial instrument, in which the

Company has an amount owing from the counterparty, failed to meet

its obligations in accordance with the terms and conditions of its

contracts with the Company.

The Company’s credit risk is primarily attributable to its accounts

receivable. The amounts disclosed in the consolidated statements of

financial position are net of allowances for doubtful accounts, which

is estimated by the Company’s management based on prior

experience and an assessment of the current economic environment.

Significant management estimates are used to determine the

allowance for doubtful accounts. The allowance for doubtful

accounts is calculated by taking into account factors such as the

Company’s historical collection and write-off experience, the number

of days the counterparty is past due, and the status of the account.

The Company believes that its allowance for doubtful accounts is

sufficient to reflect the related credit risk associated with the

Company’s accounts receivable. The concentration of credit risk of

accounts receivable is limited due to the Company’s broad customer

base. At December 31, 2012, the Company had accounts receivable of

$1,536 million (December 31, 2011 – $1,574 million), net of an

allowance for doubtful accounts of $119 million (December 31, 2011 –

$129 million). At December 31, 2012, $492 million (December 31,

2012 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 103