Rogers 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

25

Rogers Communications Inc. 2004 Annual Report

expenditures and relatively higher levels of subscriber additions, resulting in higher subscriber acquisition and activation-related

expenses in that period. Seasonal fluctuation also typically occurs in the third quarter of each year because higher usage and roaming

result in higher network revenue and operating profit.

WIRELESS COMPETITION

At December 31, 2004, the highly-competitive Canadian wireless industry had approximately 15.0 million wireless subscribers.

Competition for wireless subscribers is based on price, scope of services, service coverage, quality of service, sophistication of wireless

technology, breadth of distribution, selection of equipment, brand and marketing. Wireless also competes with its rivals for dealers

and retail distribution outlets.

In the wireless voice and data market, Wireless competes primarily with two other national wireless service providers, Bell

Mobility and Telus Mobility, as well as resellers such as Virgin Mobile Canada, Sprint Canada and Primus, and other emerging providers

using alternative wireless technologies such as WiFi or “hotspots”. Wireless messaging (or one-way paging) also competes with a number

of local and national paging providers.

RECENT WIRELESS INDUSTRY TRENDS

Focus on Customer Retention

The wireless communications industry’s current market penetration in Canada is approximately 47% of the population, compared to

approximately 59% in the U.S. and approximately 99% in the United Kingdom, and Wireless expects the Canadian wireless industry to

grow by approximately 4 percentage points of penetration each year. While this will produce growth, the growth on a year-over-year

percentage change basis is slowing compared to historical levels. This deeper penetration drives an increased focus on customer satis-

faction, the promotion of new data and voice services and features and, primarily, customer retention. Legislation in the U.S. and other

countries has mandated wireless number portability (“WNP”). Canadian regulators have indicated that they intend to review the matter

in the 2005/2006 planning period and the recent federal budget has stated that implementation of WNP should occur expeditiously.

As such, customer satisfaction and retention will become even more critical in the future.

Demand for Sophisticated Data Applications

The ongoing development of wireless data transmission technologies has led developers of wireless devices, such as handsets and

other hand-held devices, to develop more sophisticated wireless devices with increasingly advanced capabilities, including access to

e-mail and other corporate information technology platforms, news, sports, financial information and services, shopping services, photos

and video clips, and other functions. Wireless believes that the introduction of such new applications will drive the growth for data

transmission services. As a result, wireless providers will likely continue to upgrade its digital networks to be able to offer the data

transmission capabilities required by these new applications.

Migration to Next Generation Wireless Technology

The ongoing development of wireless data transmission technologies and the increased demand for sophisticated wireless services,

especially data communications services, have led wireless providers to migrate towards the next generation of digital voice and data

networks. These networks are intended to provide wireless communications with wireline quality sound, far higher data transmission

speeds and streaming video capability. These networks are expected to support a variety of increasingly advanced data applications,

including broadband Internet access, multimedia services and seamless access to corporate information systems, such as e-mail and

purchasing systems.

Development of Additional Technologies

The development of additional technologies and their use by consumers may accelerate the widespread adoption of third generation

(“3G”) digital voice and data networks. One such example is WiFi, which allows suitably equipped devices, such as laptop computers

and personal digital assistants, to connect to a wireless access point. The wireless connection is only effective within a range of approx-

imately 100 meters and at theoretical speeds of up to 54 megabits per second. To address these limitations, WiFi access points must be

placed selectively in high-traffic locations where potential customers frequent and have sufficient time to use the service. Technology

companies are currently developing additional technologies designed to improve WiFi and otherwise utilize the higher data transmission

speeds found in a 3G network. Future enhancements to the range of WiFi service, such as the emerging WiMax technology, and the net-

working of WiFi access points, may provide additional opportunities for mobile wireless operators to deploy hybrid high-mobility 3G

and limited-mobility WiFi networks, each providing capacity and coverage under the appropriate circumstances.

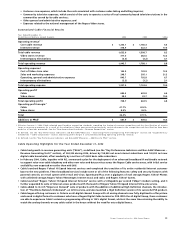

WIRELESS OPERATING AND FINANCIAL RESULTS

Year Ended December 31, 2004 Compared to Year Ended December 31, 2003

For purposes of this discussion, revenue has been classified according to the following categories:

• postpaid voice and data, revenues generated principally from

• monthly fees,

• airtime and long-distance charges,

• optional service charges,