Kodak 2007 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2007 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

64

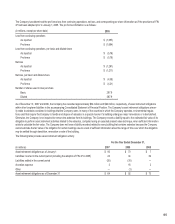

Uncertainties associated with environmental remediation contingencies are pervasive and often result in wide ranges of outcomes. Estimates developed in

the early stages of remediation can vary significantly. A finite estimate of costs does not normally become fixed and determinable at a specific time. Rather,

the costs associated with environmental remediation become estimable over a continuum of events and activities that help to frame and define a liability,

and the Company continually updates its cost estimates. The Company has an ongoing monitoring and identification process to assess how the activities,

with respect to the known exposures, are progressing against the accrued cost estimates, as well as to identify other potential remediation issues.

Estimates of the amount and timing of future costs of environmental remediation requirements are by their nature imprecise because of the continu-

ing evolution of environmental laws and regulatory requirements, the availability and application of technology, the identification of presently unknown

remediation sites and the allocation of costs among the potentially responsible parties. Based upon information presently available, such future costs are

not expected to have a material effect on the Company’s competitive or financial position. However, such costs could be material to results of operations in

a particular future quarter or year.

Asset Retirement Obligations

The Company adopted FASB Interpretation No. 47, “Accounting for Conditional Asset Retirement Obligations” (FIN 47) during the fourth quarter of 2005.

FIN 47 clarifies that the term “conditional asset retirement obligation,” as used in FASB No. 143, “Accounting for Asset Retirement Obligations,” requires

that conditional asset retirement obligations, legal obligations to perform an asset retirement activity in which the timing and/(or) method of settlement are

conditional on a future event, be reported, along with associated capitalized asset retirement costs, at their fair values. Upon initial application, FIN 47

requires recognition of (1) a liability, adjusted for cumulative accretion from the date the obligation was incurred until the date of adoption of FIN 47, for

existing asset retirement obligations; (2) an asset retirement cost capitalized as an increase to the carrying amount of the associated long-lived asset; and

(3) accumulated depreciation on the capitalized asset retirement cost. Accordingly, the Company recognized the following amounts in its Consolidated

Statement of Financial Position as of December 31, 2005 and Consolidated Statement of Operations for the year ended December 31, 2005:

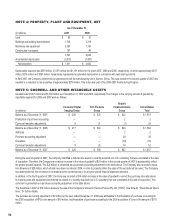

(in millions)

Additions to property, plant and equipment, gross $ 33

Additions to accumulated depreciation $ (33)

Additions to property, plant and equipment, net $ —

Asset retirement obligations $ 64

Cumulative effect of change in accounting principle, gross $ 64

Cumulative effect of change in accounting principle, net of tax $ 55

The adoption of FIN 47 reduced 2005 net earnings by $55 million, or $.19 per share.