Kodak 2007 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2007 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

19

Pension and Other Postretirement Benets

The Company accounts for its defined benefit pension plans and its other postretirement benefits in accordance with SFAS No. 87, “Employers’ Account-

ing for Pensions,” SFAS No. 88, “Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination Benefits,”

SFAS No. 106, “Employers’ Accounting for Postretirement Benefits Other than Pensions,” and SFAS No. 158, “Employers’ Accounting for Defined Benefit

Pension and Other Postretirement Plans.” These standards require that the amounts recognized in the financial statements be determined on an actuarial

basis. See Note 18, “Retirement Plans,” and Note 19, “Other Postretirement Benefits,” in the Notes to Financial Statements for disclosure of (i) the nature

of the Company’s plans, (ii) the amount of income and expense included in the Consolidated Statement of Operations for the years ended December 31,

2007, 2006 and 2005, (iii) the Company’s contributions and estimated future funding requirements and (iv) the amount of unrecognized gains and losses

at December 31, 2007 and 2006.

Kodak’s defined benefit pension and other postretirement benefit costs and obligations are dependent on the Company’s assumptions used by actuaries

in calculating such amounts. These assumptions, which are reviewed annually by the Company, include the discount rate, long-term expected rate of

return on plan assets (EROA), salary growth, healthcare cost trend rate and other economic and demographic factors. Actual results that differ from our

assumptions are recorded as unrecognized gains and losses and are amortized to earnings over the estimated future service period of the plan partici-

pants to the extent such total net unrecognized gains and losses exceed 10% of the greater of the plan’s projected benefit obligation or the market-related

value of assets. Significant differences in actual experience or significant changes in future assumptions would affect the Company’s pension and other

postretirement benefit costs and obligations.

Generally, the Company bases the discount rate assumption for its significant plans on high quality corporate long-term bond yields in the respective

countries as of the measurement date. Specifically, for its U.S. and Canada plans, the Company determines a discount rate using a cash flow model to

incorporate the expected timing of benefit payments and a AA-rated high quality corporate bond yield curve. For the Company’s other non-U.S. plans, the

discount rates are determined by comparison to published local long-term high quality bond indices.

The EROA assumption is based on a combination of formal asset and liability studies, historical results of the portfolio, and management’s expectation as

to future returns that are expected to be realized over the estimated remaining life of the plan liabilities that will be funded with the plan assets. The salary

growth assumptions are determined based on the Company’s long-term actual experience and future and near-term outlook. The healthcare cost trend

rate assumptions are based on historical cost and payment data, the near-term outlook and an assessment of the likely long-term trends.

The Company reviews its EROA assumption annually for the Kodak Retirement Income Plan (KRIP), the major U.S. defined benefit plan. To facilitate this

review, every three years, or when market conditions change materially, the Company undertakes a new asset and liability study to reaffirm the current

asset allocation and the related EROA assumption. In March 2005, an asset and liability modeling study was completed and the KRIP EROA assump-

tion for 2005, 2006 and 2007 was 9.0%. The KRIP EROA assumption is expected to remain at 9.0% for 2008 as well. Due to a reduced number of active

participants in the KRIP lowering the projected benefit obligation, service and interest cost are expected to continue to decline in 2008. Therefore, total

pension income from continuing operations before special termination benefits, curtailments and settlements for the major funded and unfunded defined

benefit plans in the U.S. is expected to increase from $156 million in 2007 to $177 million in 2008. Pension expense from continuing operations before

special termination benefits, curtailments and settlements in the Company’s major funded and unfunded non-U.S. defined benefit plans is projected to

increase from $32 million in 2007 to $42 million in 2008, which is primarily attributable increased amortization of actuarial losses. Additionally, due to favor-

able claims experience and changes in plan design, the Company expects the cost, before curtailment and settlement gains and losses of its major other

postretirement benefit plans, to approximate $148 million in 2008, as compared with $184 million for 2007.

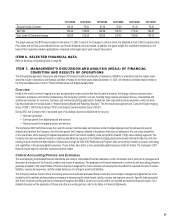

The following table illustrates the sensitivity to a change to certain key assumptions used in the calculation of expense for the year ending December 31,

2008 and the projected benefit obligation (PBO) at December 31, 2007 for the Company’s major U.S. and non-U.S. defined benefit pension plans:

Impact on 2008

Pre-Tax Pension Expense

Increase (Decrease)

Impact on PBO

December 31, 2007

Increase (Decrease)

(in millions) U.S. Non-U.S. U.S. Non-U.S.

Change in assumption:

25 basis point decrease in discount rate $ (2) $ 13 $ 119 $ 148

25 basis point increase in discount rate 2 (13) (114) (140)

25 basis point decrease in EROA 15 9 N/A N/A

25 basis point increase in EROA (15) (9) N/A N/A