ICICI Bank 2009 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

56

Management’s Discussion and Analysis

appropriate disclosures in their annual reports. Exposure for funded facilities is calculated as the total committed

credit and investment sanctions or the outstanding funded amount, whichever is higher (for term loans, as the

sum of undisbursed commitments and the outstanding amount). Exposure for non-funded facilities is calculated

as 100.0% of the committed amount or the outstanding non-funded amount whichever is higher.

During the year-end fiscal 2009, we had no single borrower and borrower group exposures which exceeded the

prudential exposure limits prescribed by RBI.

Directed Lending

RBI requires banks to lend to certain sectors of the economy. Such directed lending comprises priority sector

lending, export credit and housing finance.

RBI guidelines require banks to lend 40.0% of their adjusted net bank credit, or credit equivalent amount of off

balance sheet exposure, whichever is higher, to certain specified sectors called priority sectors. The definition of

adjusted net bank credit does not include certain exemptions and includes certain investments and is computed with

reference to the outstanding amount at March 31 of the previous year. Priority sectors include small enterprises,

agricultural sector, food and agri-based industries, small businesses and housing finance up to certain limits. Out of

the 40.0%, banks are required to lend a minimum of 18.0% of their net bank credit to the agriculture sector and the

balance to certain specified sectors, including small enterprises (defined as enterprises engaged in manufacturing/

production, processing and services businesses with a certain limit on investment in plant and machinery), small

road and water transport operators, small businesses, professional and self-employed persons, and all other

service enterprises, retail trade, micro credit, education and housing loans up to Rs. 2.0 million to individuals

for purchase/construction of a dwelling unit per family. In its letter dated April 26, 2002 granting its approval for

the amalgamation, RBI stipulated that since the loans of erstwhile ICICI Limited (ICICI) transferred to us were not

subject to the priority sector lending requirement, we are required to maintain priority sector lending of 50.0%

of our net bank credit on the residual portion of our advances (i.e. the portion of our total advances excluding

advances of ICICI at year-end fiscal 2002, referred to as “residual net bank credit”). This additional 10.0% priority

sector lending requirement will apply until such time as our aggregate priority sector advances reach a level of

40.0% of our total net bank credit. RBI’s existing instructions on sub-targets under priority sector lending and

eligibility of certain types of investments/ funds for qualification as priority sector advances apply to us.

Any shortfall in the amount required to be lent to the priority sectors may be required to be deposited with

government sponsored Indian development banks like the National Bank for Agriculture and Rural Development,

the Small Industries Development Bank of India and the National Housing Bank. These deposits have a maturity

of up to seven years and carry interest rates lower than market rates. At year-end fiscal 2009, total investments

in such bonds were Rs. 60.00 billion.

As per the guidelines, banks are also required to lend to the weaker sections 10.0% of adjusted net bank credit

or credit equivalent amount of off-balance sheet exposures, whichever is higher. In order to ensure that the

sub-target of lending to the weaker sections is achieved, RBI has decided to take into account the shortfall in lending

to weaker sections also, at the last reporting Friday of March of each year, for the purpose of allocating amounts

to the domestic Scheduled Commercial Banks (SCBs) for contribution to the Rural Infrastructure Development

Fund (RIDF) maintained with NABARD or funds with other Financial Institutions, as specified by RBI, with effect

from April 2009.

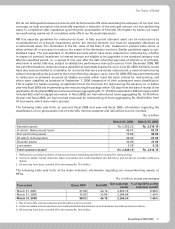

We are required to comply with the priority sector lending requirements on the last “reporting Friday” of each

fiscal year. At March 27, 2009, which was the last reporting Friday for fiscal 2009, our priority sector loans were

Rs. 684.26 billion, constituting 50.6% of our residual adjusted net bank credit against the requirement of 50.0%.

At that date, qualifying agriculture loans were 19.0% of our residual net bank credit as against the requirement

of 18.0%. Our advances to weaker sections were Rs. 20.74 billion constituting 1.5% of our residual adjusted net

bank credit against the requirement of 10.0%.

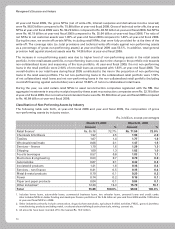

Classification of Loans

We classify our assets as performing and non-performing in accordance with RBI guidelines. Under these guidelines,

an asset is classified as non-performing if any amount of interest or principal remains overdue for more than

90 days, in respect of term loans. In respect of overdraft or cash credit, an asset is classified as non-performing

if the account remains out of order for a period of 90 days and in respect of bills, if the account remains overdue

for more than 90 days.