ICICI Bank 2009 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

55Annual Report 2008-2009

The Power of Belief

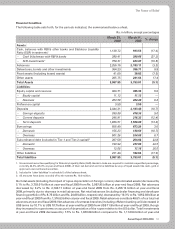

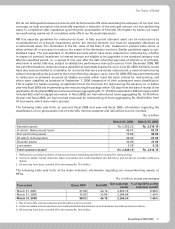

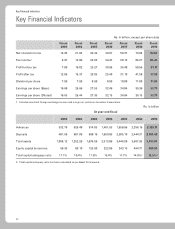

The following tables set forth, at the dates indicated, the composition of our gross advances (net of write-offs).

Rs. in billion, except percentages

March 31, 2008 March 31, 2009

Total

advances % of total

advances Total

advances % of total

advances

Retail finance11,347.54 58.6 1,102.20 49.3

Services – non finance 145.57 6.3 168.05 7.5

Crude petroleum/refining & petrochemicals 58.21 2.5 142.04 6.4

Iron/steel & products 93.23 4.1 99.14 4.4

Road, port, telecom, urban development & other infrastructure 51.45 2.2 94.62 4.2

Services – finance 66.18 2.9 77.68 3.5

Power 58.08 2.5 54.19 2.4

Food & beverages 63.32 2.8 53.57 2.4

Chemical & fertilisers 38.06 1.7 51.83 2.3

Electronics & engineering 20.82 0.9 36.17 1.6

Wholesale/retail trade 25.26 1.1 26.29 1.2

Construction 29.36 1.3 23.86 1.1

Other industries2301.84 13.1 306.57 13.7

Total 2,298.92 100.0% 2,236.21 100.0%

1. Includes home loans, automobile loans, commercial business loans, two wheeler loans, personal loans and credit cards. It also

includes dealer funding portfolio of Rs. 8.83 billion (Rs. 24.10 billion at year-end fiscal 2008) and developer financing of Rs. 24.14

billion (Rs. 27.79 billion at year-end fiscal 2008).

2. Other industries primarily include automobiles, cement, drugs & pharmaceuticals, agriculture & allied activities, FMCG, gems &

jewellery, manufacturing products excluding metal, metal & metal products (excluding iron & steel), mining, shipping, textiles etc.

The following table sets forth, at the dates indicated, the composition of our gross (net of write-offs) outstanding

retail finance portfolio.

Rs. in billion, except percentages

March 31, 2008 March 31, 2009

Total retail

advances % of total

retail advances Total retail

advances % of total

retail advances

Home loans1664.39 49.3 575.88 52.2

Automobile loans 174.66 13.0 133.05 12.1

Commercial business 203.71 15.1 164.40 14.9

Two-wheeler loans 29.81 2.2 16.91 1.5

Personal loans 144.13 10.7 108.66 9.9

Credit cards 96.45 7.2 90.02 8.2

Loans against securities & others234.39 2.5 13.28 1.2

Total retail finance portfolio 1,347.54 100.0% 1,102.20 100.0%

1. Includes developer financing of Rs. 27.79 billion and Rs. 24.14 billion at year-end fiscal 2008 and year-end fiscal 2009 respectively.

2. Includes dealer financing portfolio of Rs. 24.10 billion and Rs. 8.83 billion at year-end fiscal 2008 and year-end fiscal 2009

respectively.

Pursuant to the guidelines of RBI, our exposure to an individual borrower must not exceed 15.0% of our capital

funds, comprising Tier-1 and Tier-2 capital calculated pursuant to the guidelines of RBI. Exposure to individual

borrowers may exceed the exposure norm of 15.0% of capital funds by an additional 5.0% (i.e. up to 20.0%)

provided the additional exposure is on account of infrastructure financing. Our exposure to a group of companies

under the same management control must not exceed 40.0% of our capital funds unless the exposure is in respect

of an infrastructure project. In case of infrastructure projects, the exposure to a group of companies under the

same management control may be up to 50.0% of our capital funds. Banks may, in exceptional circumstances,

with the approval of their boards, enhance the exposure by 5.0% of capital funds (i.e. 20.0% of capital funds for

an individual borrower and 45.0% of capital funds for a group of companies under same management), making