ICICI Bank 2009 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

F41

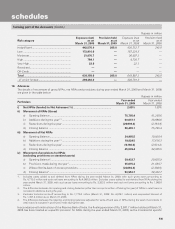

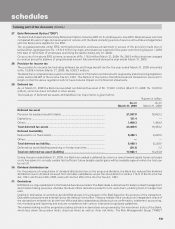

Rupees in million

As on March 31, 2008

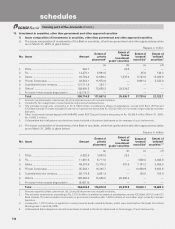

Sr.

No. Particulars Currency

derivatives1Interest rate

derivatives2

1. Derivatives (Notional principal amount)

a) For hedging ........................................................................................... 27,056.3 206,265.5

b) For trading ............................................................................................. 1,536,757.0 6,372,250.2

2. Marked to market positions3

a) Asset (+) ............................................................................................... 30,085.1 184.5

b) Liability (–) ............................................................................................. — —

3. Credit exposure4 ............................................................................................ 109,607.8 83,103.4

4. Likely impact of one percentage change in interest rate (100*PV01)5

a) On hedging derivatives6 ........................................................................ 559.5 8,879.2

b) On trading derivatives ........................................................................... 1,777 .8 2,270.7

5. Maximum and minimum of 100*PV01 observed during the year

a) On hedging6

Maximum .............................................................................................. (11.6) (4,268.4)

Minimum ............................................................................................... (714.7) (9,467.8)

b) On trading

Maximum .............................................................................................. (313.2) 2,809.2

Minimum ............................................................................................... (1,870.9) 464.9

1. Options and cross currency interest rate swaps are included in currency derivatives.

2. Foreign currency interest rate swaps, forward rate agreements and swaptions are included in interest rate derivatives.

3. For trading portfolio including accrued interest. Represents net positions.

4. Includes accrued interest.

5. Amounts given are absolute values on a net basis, excluding options.

6. The swap contracts entered for hedging purpose would have an opposite and offsetting impact with the underlying on-balance sheet

items.

The Bank deals in credit derivative instruments including credit default swaps, credit linked notes, collateralised debt

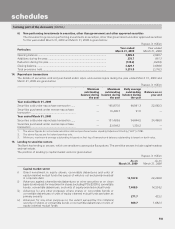

obligations and principal protected structures. The notional principal amount of these credit derivatives outstanding as on

March 31, 2009 was Rs. 18,411.4 million (March 31, 2008: Rs. 12,231.2 million) in funded instruments and Rs. 38,712.6

million (March 31, 2008: Rs. 50,568.5 million) in non-funded instruments which includes Rs. 253.6 million (March 31, 2008:

Rs. 200.6 million) of protection bought by the Bank.

The profit and loss impact of the above portfolio on account of mark-to-market and realised loss during the year ended

March 31, 2009 was a net loss of Rs. 2,754.3 million (March 31, 2008: Rs. 6,848.3 million). As on March 31, 2009, the total

outstanding mark-to-market position of the above portfolio was a net loss of Rs. 4,843.9 million (March 31, 2008: Rs. 5,870.6

million). The credit derivatives are marked to market by the Bank based on counter-party valuation quotes, or internal models

using inputs from market sources such as Bloomberg/Reuters, counter-parties and FIMMDA.

The Bank offers deposits to customers of its offshore branches with structured returns linked to interest, forex or equity

benchmarks. The Bank covers these exposures in the inter-bank market. As on March 31, 2009, the net open position

on this portfolio was Rs. Nil (March 31, 2008: Rs. 4.0 million) with mark-to-market loss of Rs. Nil (March 31, 2008:

Rs. 0.1 million).

The notional principal amount of forex contracts, classified as non-trading at March 31, 2009 amounted to Rs. 205,635.1

million (March 31, 2008: Rs. 393,701.5 million). The notional principal amount of forex contracts classified as trading at

March 31, 2009 amounted to Rs. 2,378,035.8 million (March 31, 2008: Rs. 2,678,010.8 million).

The net overnight open position at March 31, 2009 was Rs. 512.3 million (March 31, 2008: Rs. 2,584.5 million).

forming part of the Accounts (Contd.)

schedules