ICICI Bank 2009 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

|

|

F90

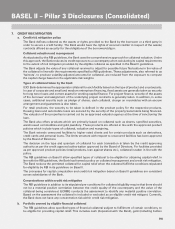

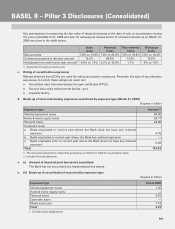

The credit rating process involves assessment of risk emanating from various sources such as industry risk,

business risk, financial risk, management risk, project risk and structure risk. For all corporate and majority of small

enterprises, a case-by-case rating is issued based on detailed analysis of the above factors.

In respect of retail advances, the Bank’s credit officers evaluate credit proposals on the basis of the product policy

approved by the Retail Credit Forum and the risk assessment criteria defined by the Global Retail Credit Risk

Management Group.

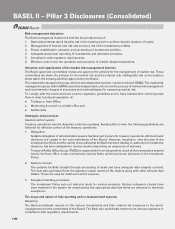

Credit approval authorisation structure

The Board of Directors has delegated the authority to the Credit Committee consisting of a majority of independent

Directors, the Committee of Directors consisting of whole time Directors, the Committee of Executives, the Regional

Committee, Small Enterprise Group Forums and Agricultural Credit Forums, all consisting of designated executives

and to individual executives in the case of program/policy based products, to approve financial assistance within

certain individual and group exposure limits set by the Board of Directors. The authorization is based on the level

of risk and the quantum of exposure, to ensure that the transactions with higher exposure and level of risk are put

up to correspondingly higher forum/committee for approval.

In respect of retail loans, all product-level policies require the approval of the Retail Credit Forum, comprising of

Executive Director and senior managers. These criteria vary across product segments but typically include factors

such as the borrower’s income, the loan-to-value ratio and demographic parameters. The individual credit proposals

are evaluated and approved by executives on the basis of the product policies.

Credit risk monitoring process

For effective monitoring of credit facilities, a post-approval authorization structure has been laid down. For Corporate

and Small Enterprises and RMAG, Credit Middle Office Group verifies adherence to the terms of the approval prior

to commitment and disbursement of credit facilities.

For retail credit, the Bank has established centralised operations to manage operating risk in the various back

office processes of the Bank’s retail loan business except for a few operations, which are decentralized to improve

turnaround time for customers. A fraud prevention and control group has been set up to manage fraud-related

risks through fraud prevention and through recovery of fraud losses. The fraud control group evaluates various

external agencies involved in the retail finance operations, including direct marketing associates, external verification

associates and collection agencies.

The Bank has a collections unit structured along various product lines and geographical locations, to control

delinquency levels. The collections unit operates under the guidelines of a standardised recovery process.

Reporting and measurement

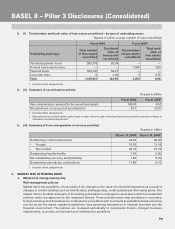

Credit exposure for ICICI Bank is measured & monitored using a centralised exposure management system. The

analysis of the composition of the portfolio is presented to the Risk Committee on a quarterly basis.

ICICI Bank complies with the norms on exposure stipulated by RBI for both single borrower as well as borrower

group at the consolidated level. Limits have been set by the risk management group as a percentage of the Bank’s

consolidated capital funds and are regularly monitored. The utilisation against specified limits is reported to the

Committee of Directors and Credit Committee on a periodic basis.

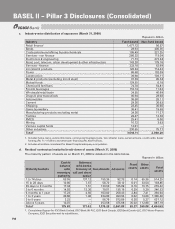

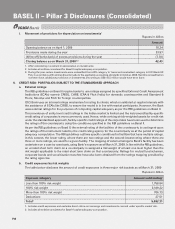

Credit concentration risk

Credit concentration risk arises mainly on account of concentration of exposures under various categories including

industry, products, geography, underlying collateral nature and single/group borrower exposures.

Within the corporate portfolio, as a prudential measure in line with better risk management practice, the RBI has

prescribed regulatory limits on banks’ maximum exposure to single borrowers and group borrowers. In order to

restrict the concentration risk arising out of longer tenure exposure within the prudential limits set by RBI, the Board

of ICICI Bank has approved prescribed sub-limits for the maximum long tenor exposure to a particular borrower

group.

Limits are stipulated in the credit policy to address concentration risk. Limits have been stipulated on single borrower,

group, industry, longer tenure exposure to a group. Exposure of top 10 borrowers and borrower groups for the

consolidated Bank are reported to the Committee of Directors on a quarterly basis.

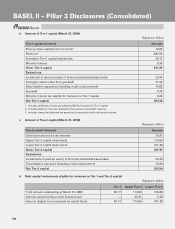

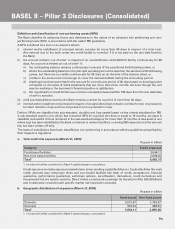

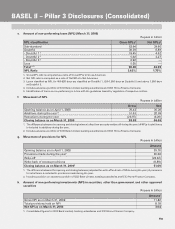

BASEL II – Pillar 3 Disclosures (Consolidated)