ICICI Bank 2009 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

53Annual Report 2008-2009

The Power of Belief

‘Claims against the Bank, not acknowledged as debts’, represents demands made by the Government of India’s

tax authorities in excess of the provisions made in our accounts, in respect of income tax, interest tax, wealth tax,

service tax and sales tax/VAT matters. Based on consultation with counsel and favourable decisions in our own or

other cases, the management believes that the liability is not likely to actually arise. Other items for which the Bank

is contingently liable include primarily credit derivatives, repurchase and securitisation-related obligations.

As a part of our project financing and commercial banking activities, we have issued guarantees to enhance the

credit standing of our customers. These generally represent irrevocable assurances that we will make payments

in the event that the customer fails to fulfill its financial or performance obligations. Financial guarantees are

obligations to pay a third party beneficiary where a customer fails to make payment towards a specified financial

obligation. Performance guarantees are obligations to pay a third party beneficiary where a customer fails to

perform a non-financial contractual obligation. The guarantees are generally for a period not exceeding 10 years.

The credit risks associated with these products, as well as the operating risks, are similar to those relating to

other types of financial instruments. We generally have collateral available to reimburse potential losses on the

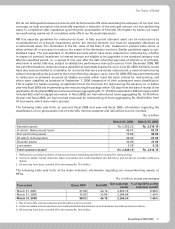

guarantees. Margins available to reimburse losses realised under guarantees amounted to Rs. 11.69 billion at

year-end fiscal 2009 and Rs. 10.61 billion at year-end fiscal 2008. Other property or security may also be available

to us to cover losses under guarantees.

We are obligated under a number of capital contracts. Capital contracts are job orders of a capital nature, which have

been committed. As of the balance sheet date, work had not been completed to this extent. Estimated amounts of

contracts remaining to be executed on capital account aggregated Rs. 4.46 billion at year-end fiscal 2009 compared

to Rs. 17.40 billion at year-end fiscal 2008 primarily on account of new branches and office premises.

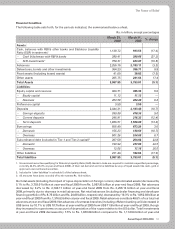

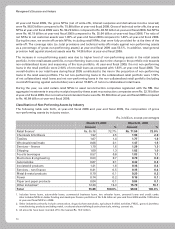

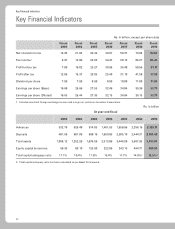

Capital Adequacy

Rs. in billion, except percentages

As per RBI guidelines

on Basel I As per RBI guidelines

on Basel II

March 31,

2008 March 31,

2009 March 31,

2008 March 31,

2009

Tier-1 capital 381.34 420.09 421.72 421.96

Tier-2 capital 121.21 129.72 78.86 131.59

Total capital 502.55 549.81 500.59 553.55

Credit Risk – Risk Weighted Assets (RWA) 2,998.08 3,171.94 3,173.33 3,151.95

Market Risk – RWA 369.46 281.44 258.74 206.98

Operational Risk – RWA — —152.50 205.70

Total risk weighted assets 3,367.55 3,453.38 3,584.57 3,564.63

Tier-1 capital adequacy ratio 11.32% 12.16% 11.76% 11.84%

Tier-2 capital adequacy ratio 3.60% 3.76% 2.20% 3.69%

Total capital adequacy ratio 14.92% 15.92% 13.97% 15.53%

We are subject to the capital adequacy norms stipulated by the RBI guidelines on Basel II which became applicable

to us with effect from year-end fiscal 2008. Prior to year-end fiscal 2008, we were subject to the capital adequacy

norms as stipulated by the RBI guidelines on Basel I. The RBI guidelines on Basel II require us to maintain a

minimum ratio of total capital to risk weighted assets of 9.0%, with a minimum Tier-1 capital adequacy ratio of

6.0%. Our total capital adequacy ratio at year-end fiscal 2009 as per the RBI guidelines on Basel II is 15.53% with

a Tier-1 capital adequacy ratio of 11.84%.

Under Pillar 1 of the RBI guidelines on Basel II, we follow the standardised approach for credit and market risk

and basic indicator approach (BIA) for operational risk.

In view of its transitional arrangements to the Basel II framework, RBI has prescribed a parallel run under which

we calculate capital adequacy under both Basel I and Basel II. Further at year-end fiscal 2009, we are required to

maintain capital adequacy based on the higher of the minimum capital required under Basel II or at 90.0% of the

minimum capital required under Basel I. The computation under Basel II guidelines results in a higher minimum

capital requirement as compared to Basel I and hence as a result the capital adequacy at year-end fiscal 2009 has

been maintained and reported by us as per Basel II guidelines.