ICICI Bank 2009 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

|

|

F95

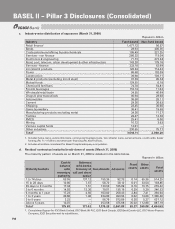

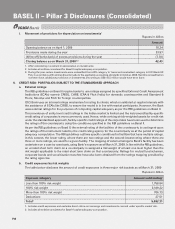

7. CREDIT RISK MITIGATION

a. Credit risk mitigation policy

The Bank defines collateral as the assets or rights provided to the Bank by the borrower or a third party in

order to secure a credit facility. The Bank would have the rights of secured creditor in respect of the assets/

contracts offered as security for the obligations of the borrower/obligor.

Collateral valuation and management

As stipulated by the RBI guidelines, the Bank uses the comprehensive approach for collateral valuation. Under

this approach, the Bank reduces its credit exposure to a counterparty when calculating its capital requirements

to the extent of risk mitigation provided by the eligible collateral as specified in the Basel II guidelines.

The Bank adjusts the value of any collateral received to adjust for possible future fluctuations in the value of

the collateral in line with the requirements specified by RBI guidelines. These adjustments, also referred to as

‘haircuts’, to produce volatility-adjusted amounts for collateral, are reduced from the exposure to compute

the capital charge based on the applicable risk weights.

Types of collateral taken by the Bank

ICICI Bank determines the appropriate collateral for each facility based on the type of product and counterparty.

In case of corporate and small and medium enterprises financing, fixed assets are generally taken as security

for long tenor loans and current assets for working capital finance. For project finance, security of the assets

of the borrower and assignment of the underlying project contracts is generally taken. In addition, in some

cases, additional security such as pledge of shares, cash collateral, charge on receivables with an escrow

arrangement and guarantees is also taken.

For retail products, the security to be taken is defined in the product policy for the respective products.

Housing loans and automobile loans are secured by the security of the property/automobile being financed.

The valuation of the properties is carried out by an approved valuation agency at the time of sanctioning the

loan.

The Bank also offers products which are primarily based on collateral such as shares, specified securities,

warehoused commodities and gold jewellery. These products are offered in line with the approved product

policies which include types of collateral, valuation and margining.

The Bank extends unsecured facilities to higher rated clients and for certain products such as derivatives,

credit cards and personal loans. The limits structure with respect to unsecured facilities has been approved

by the Board of Directors.

The decision on the type and quantum of collateral for each transaction is taken by the credit approving

authority as per the credit approval authorisation approved by the Board of Directors. For facilities provided

as per approved product policies (retail products, loan against shares etc.), collateral is taken in line with the

policy.

The RBI guidelines on Basel II allow specified types of collateral to be eligible for obtaining capital relief. In

line with the RBI guidelines, the Bank has framed a policy on collateral management and credit risk mitigation.

The Bank reckons the permitted collateral for capital relief when the collateral fulfill the conditions stipulated

for eligibility by RBI in its guidelines on Basel II.

The processes for capital computation and credit risk mitigation based on Basel II guidelines are consistent

across subsidiaries of the Bank.

Concentrations within credit risk mitigation

The RBI guidelines in addition to its stipulated pre-conditions for collateral eligibility require that there should

not be a material positive correlation between the credit quality of the counterparty and the value of the

collateral being considered. GCRMG conducts the assessment to identify any material positive correlation.

Based on the assessment the collateral is included or excluded as an eligible credit risk mitigant. Currently,

the Bank does not have any concentration risk within credit risk mitigation.

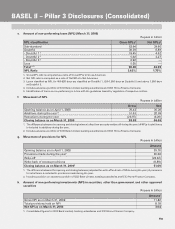

b. Portfolio covered by eligible financial collateral

The RBI guidelines allow specified types of financial collateral subject to fulfillment of certain conditions, to

be eligible for providing capital relief. This includes cash (deposited with the Bank), gold (including bullion

BASEL II – Pillar 3 Disclosures (Consolidated)