ICICI Bank 2009 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180

|

|

F96

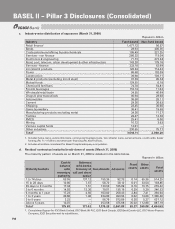

and jewellery, subject to collateralized jewellery being benchmarked to 99.99% purity), securities issued by

Central and State Governments, Kisan Vikas Patra, National Savings Certificates, life insurance policies with a

declared surrender value issued by an insurance company which is regulated by the insurance sector regulator,

certain debt securities rated by a recognized credit rating agency, mutual fund units where daily Net Asset

Value (NAV) is available in public domain and the mutual fund is limited to investing in the instruments listed

above. The Bank reckons the permitted financial collateral for capital relief when the financial collateral fulfill

the conditions stipulated for eligibility by RBI in its guidelines on Basel II.

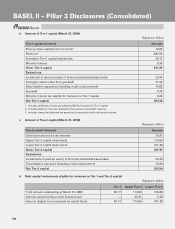

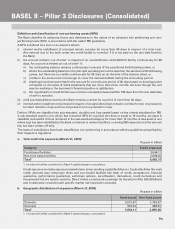

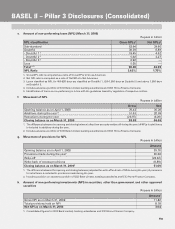

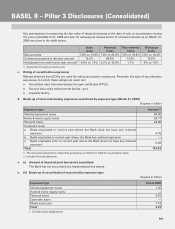

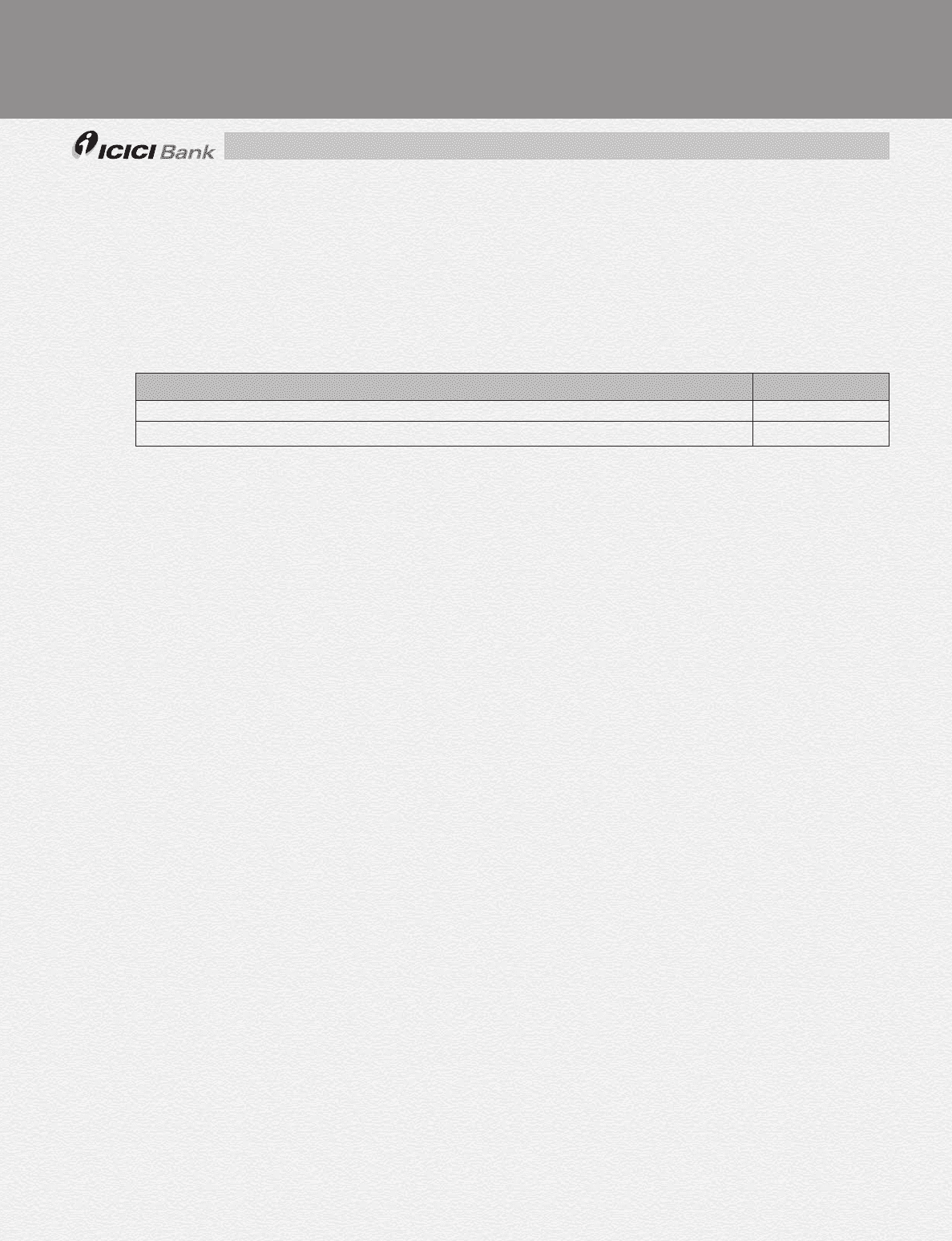

The table below details the total exposure that is covered by eligible financial collateral as at

March 31, 2009.

Rupees in billion

Exposures covered by eligible financial collateral Amount1

Exposure before considering eligible financial collateral 208.31

Exposure after considering eligible financial collateral 162.80

1. Includes all entities considered for Basel II capital adequacy computation.

8. SECURITISATION

a. Securitisation objectives and policies

Objectives

The Bank’s primary objective of securitization activities is to increase the efficiency of capital and enhance the

return on capital employed by diversifying sources of funding.

Roles played by the Bank

In securitization transactions backed by assets either originated by the Bank or third parties, the Bank plays

the following major roles:

Underwriter: allowing un-subscribed portions of securitized debt issuances, if any to devolve on the

Bank, with the intent of selling at a later stage.

Investor/trader/market-maker: acquiring investment grade securitized debt instruments backed by

financial assets originated by third parties for purposes of investment/trading/market-making with the

aim of developing an active secondary market in securitized debt.

Structurer: structuring appropriately in a form and manner suitably tailored to meet investor requirements

while being compliant with extant regulations.

Provider of liquidity facilities: addressing temporary mismatches on account of the timing differences

between the receipt of cash flows from the underlying performing assets and the fulfillment of obligations

to the beneficiaries.

Provider of credit enhancement facilities: addressing delinquencies associated with the underlying

assets, i.e. bridging the gaps arising out of credit considerations between cash flows received/collected

from the underlying assets and the fulfillment of repayment obligations to the beneficiaries.

Provider of collection and processing services: collecting and/or managing receivables from underlying

obligors, contribution from the investors to securitisation transactions, making payments to counterparties/

appropriate beneficiaries, reporting the collection efficiency and other performance parameters and

providing other services relating to collections and payments as may be required for the purpose of the

transactions.

b. Summary of the Bank’s accounting policies for securitisation activities

The Bank transfers commercial and consumer loans through securitisation transactions. The transferred

loans are de-recognised and gains/losses are accounted for only if the Bank surrenders the rights to benefits

specified in the loan contracts. Recourse and servicing obligations are accounted for net of provisions.

In accordance with the RBI guidelines, with effect from February 1, 2006, the Bank accounts for any loss

arising from securitisation immediately at the time of sale and the profit/premium arising from securitisation

is amortised over the life of the securities issued or to be issued by the special purpose vehicle to which the

assets are sold. In the case of loans sold to an asset reconstruction company, the gain, if any, is ignored.

BASEL II – Pillar 3 Disclosures (Consolidated)