ICICI Bank 2009 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180

|

|

F100

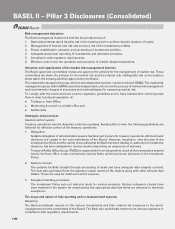

Risk management objectives

The Bank manages its market risk with the broad objectives of:

1. Optimizing interest rate & liquidity risk in the banking book to achieve desired duration of equity.

2. Management of interest rate risk and currency risk of the investment portfolio.

3. Proper classification, valuation and accounting of investment portfolio.

4. Adequate and proper reporting of investments and derivative products.

5. Compliance with regulatory requirements.

6. Effective control over the operation and execution of market related transactions.

Structure and organisation of the market risk management function

The Board approved committees review and approve the policies for the management of market risk. These

committees lay down the policies for the market risk and the interest rate risk/liquidity risk on the balance

sheet within the broad guidelines approved by the Board.

The market risk management group, which is an independent function, reports to head of GRMG. The market risk

management group within GRMG exercises independent control over the process of market risk management

and recommends changes in processes and methodologies for measuring market risk.

To comply with the home and host country regulatory guidelines and to have independent control groups

there is clear functional separation of:

Trading i.e. front Office,

Monitoring & control i.e. middle office and

Settlements.

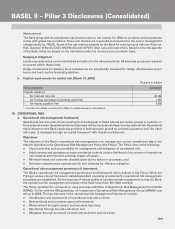

Strategies and processes

Internal control system

Treasury operations warrant elaborate control procedures. Keeping this in view, the following guidelines are

followed for effective control of the treasury operations:

1. Delegation

Suitable delegation of administrative powers has been put in place for treasury operations. All investment

decisions are vested in the sub-committees of the Board. However, keeping in view the size of the

investment portfolio and the variety of securities that the Bank has been dealing in, authority for investment

decisions has been delegated to various dealers depending on exigencies of business.

Treasury Middle Office Group (TMOG) is responsible for an independent check of the transactions entered

into by the front office. It also monitors the various limits, which have been laid down in the Investment

Policy.

2. System controls

The systems facilitate straight through processing of deals and have adequate data integrity controls.

The deal slips generated from the systems contain names of the dealers along with other relevant deal

details. These are used for audit and control purpose.

3. Exception handling processes

The Investment Policy sets out deal-size limits for various products. Various coherence checks have

been inserted in the system for ensuring that the appropriate deal size limits are enforced to minimize

exceptions.

The scope and nature of risk reporting and/or measurement systems

Reporting

The Bank periodically reports on the various investments and their related risk measures to the senior

management and the committees of the Board. The Bank also periodically reports to its various regulators in

compliance with regulatory requirements.

BASEL II – Pillar 3 Disclosures (Consolidated)