ICICI Bank 2009 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2009 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

F42

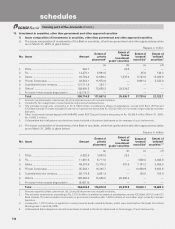

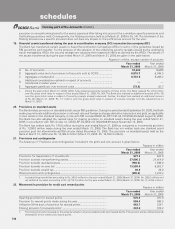

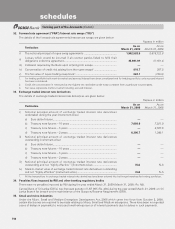

32. Forward rate agreement (“FRA”)/Interest rate swaps (“IRS”)

The details of the forward rate agreements/interest rate swaps are given below:

Rupees in million

Particulars As on

March 31, 2009 As on

March 31, 2008

i) The notional principal of rupee swap agreements ............................................ 1,942,528.9 5,618,122.6

ii) Losses which would be incurred if all counter parties failed to fulfil their

obligations under the agreement........................................................................ 35,591.81 37,181.6

iii) Collateral required by the Bank upon entering into swaps ................................ ——

iv) Concentration of credit risk arising from the rupee swaps2 ............................... 919.7 307.5

v) The fair value of rupee trading swap book3 ........................................................ 622.1 (120.9)

1. For trading portfolio both mark-to-market and accrued interest have been considered and for hedging portfolio, only accrued interest

has been considered.

2. Credit risk concentration is measured as the highest net receivable under swap contracts from a particular counter-party.

3. Fair value represents mark-to-market including accrued interest.

33. Exchange traded interest rate derivatives

The details of exchange traded interest rate derivatives are given below:

Rupees in million

Particulars As on

March 31, 2009 As on

March 31, 2008

i) Notional principal amount of exchange traded interest rate derivatives

undertaken during the year (instrument-wise)

a) Euro dollar futures ....................................................................................... ——

b) Treasury note futures – 10 years ................................................................ 7,608.0 7,021.0

c) Treasury note futures – 5 years .................................................................. —4,557.6

d) Treasury note futures – 2 years .................................................................. 6,390.7 1,380.1

ii) Notional principal amount of exchange traded interest rate derivatives

outstanding (instrument-wise)

a) Euro dollar futures ....................................................................................... ——

b) Treasury note futures – 10 years ................................................................ ——

c) Treasury note futures – 5 years .................................................................. ——

d) Treasury note futures – 2 years .................................................................. ——

iii) Notional principal amount of exchange traded interest rate derivatives

outstanding and not “highly effective ” (instrument-wise) ................................. N.A N.A

iv) Mark-to-market value of exchange traded interest rate derivatives outstanding

and not “highly effective” (instrument-wise) ...................................................... N.A N.A

1. All the transactions in exchange traded interest rate derivatives have been entered into by foreign branches for trading portfolios.

34. Penalties/fines imposed by RBI and other banking regulatory bodies

There were no penalties imposed by RBI during the year ended March 31, 2009 (March 31, 2008: Rs. Nil).

Central Bank of Sri Lanka (CBSL) has imposed penalty of LKR 865 (Rs. 400) during the year ended March 31, 2009, on Sri

Lanka Branch for breach on the maintenance of the Statutory Reserve Requirement (SRR).

35. Small and micro industries

Under the Micro, Small and Medium Enterprises Development Act, 2006 which came into force from October 2, 2006,

certain disclosures are required to be made relating to Micro, Small and Medium enterprises. There have been no reported

cases of delays in payments to micro and small enterprises or of interest payments due to delays in such payments.

forming part of the Accounts (Contd.)

schedules