Volvo 2014 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2014 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

149

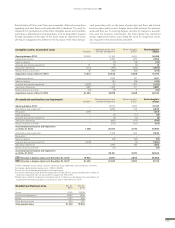

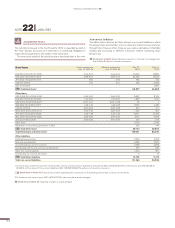

Assumptions applied for actuarial

calculations, % Dec 31,

2014 Dec 31,

2013

Sweden

Discount rate12.75 4.00

Expected salary increase 3.00 3.00

Infl ation 1.50 1.50

United States

Discount rate1 2 2.50–4.30 2.50–4.75

Expected salary increase 2.70–3.50 3.50

Infl ation 2.50 2.50

France

Discount rate11.50–2.00 3.25

Expected salary increase 2.50–3.00 3.00

Infl ation 1.50 1.50

Great Britain

Discount rate13.50–3.75 4.25–4.40

Expected salary increases 3.60–3.70 3.70–3.75

Infl ation 3.00 3.25

1 The discount rate for each country is determined by reference to market yields on

high-quality corporate bonds. In countries where there is no functioning market in

such bonds, the market yields on government bonds are used. The discount rate

for the Swedish pension obligation is determined by reference to mortgage bonds.

2 For all plans except two the discount rate used is within the range 3.60–4.30%

(3.75–4.75).

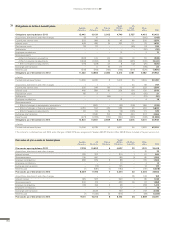

Pension costs 2014 2013

Current year service costs 1,298 1,297

Interest costs 1,479 1,319

Interest income (1,180) (842)

Past service costs 58 144

(Gain) loss on settlements (54) 0

Pension costs for the period,

defi ned-benefi t plans 1,601 1,918

Pension costs for defi ned-contribution plans 2,530 2,226

Total pension costs for the period 4,131 4,144

Costs for the period, post–employment

benefi ts other than pensions 2014 2013

Current year service costs 56 82

Interest costs 141 116

Interest income (2) (2)

Past service costs (37) 82

(Gain) loss on settlements – 1

Remeasurements (55) 7

Total costs for the period, post–employment

benefi ts other than pensions 103 286

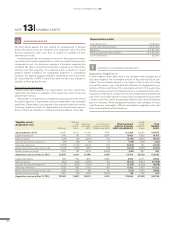

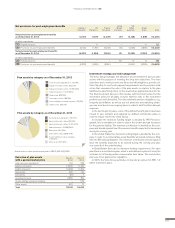

− +

Effect on obligation, SEK M

If discount rate increases 0.5% If discount rate decreases 0.5%

Sweden Pensions

Sweden Pensions

US Pensions

US Pensions

US Other benefits

US Other benefits

France Pensions

France Pensions

Great Britain Pensions

Great Britain Pensions

If inflation decreases 0.5% If inflation increases 0.5%

(1,667)

(854)

(204)

1,807

941

220

(539)

(176)

618

193

(1,667) 1,807

0

(5)

0

5

(422)

(17) 19

473

Sensitivity analysis

Sweden

Pensions US

Pensions France

Pensions Great Britain

Pensions US

Other benefi ts

Average duration of the obligation, years 21.9 10.9 15.5 17.7 10.7

The analysis below presents the sensitivity on the defi ned benefi t

obligations when changes in the applied assumptions for discount rate

and infl ation are made. The sensitivity analysis is based on a change in

an assump tion while holding all other assumptions constant. In practice,

thisis not probable, and changes in some of the assumptions may be

correlated.

FINANCIAL INFORMATION 2014