Volvo 2014 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2014 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

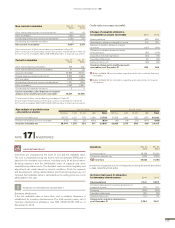

ACCOUNTING POLICIES

Credit loss reserves

The assessment of credit loss reserves on customer-financing receiva-

bles is dependent on estimates including assumptions regarding past

dues, repossession rates and the recovery rate on the underlying collater-

als. The impairment requirement is primarily evaluated for each respective

asset. If, based on objective grounds, it cannot be determined that one or

more assets are subject to an impairment loss, the assets are grouped in

units based, for example, on similar credit risks to evaluate the impairment

loss requirement collectively. This is in order to cover credit losses incurred

but not yet individually identified in a larger population. Individually

impaired assets or assets impaired during previous periods are not

included when grouping assets for collective assessment. If the condi-

tions that gave rise to the recognition of an impairment loss later prove to

no longer be valid the impairment loss is reversed in the income statement

as long as the carrying amount does not exceed the amortized cost at the

time of the reversal.

As of December 31, 2014, the total credit loss reserves in the Cus-

tomer Finance segment amounted to 1.33% (1.31) of the total credit port-

folio in the segment. This reserve ratio, which is used as an important

measure for the Customer Finance segment, includes operating leases

and inventory, whereas this note specifies the balance sheet item Cus-

tomer Finance receivables for the Volvo Group and thereby excludes

operating leases and inventory as they are recognized elsewhere in the

balance sheet.

Read more in Note 4 for a description of the credit risk, interest and currency

risks and in Note 30 for further information regarding customer-financing

receivables.

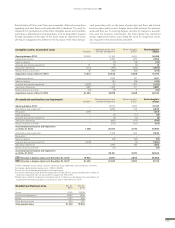

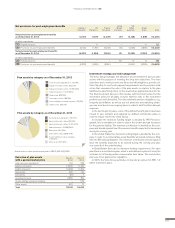

Non-current customer-financing receivables

Non-current customer-financing

receivables Dec 31,

2014 Dec 31,

2013

Installment credits 28,055 21,850

Financial leasing 21,820 21,040

Other receivables 1,455 902

B/S Non-current customer financing

receivables 51,331 43,792

The effective interest rate for non-current customer-financing receivables

amounted to 4.96% (5.61) as of December 31, 2014.

SOURCES OF ESTIMATION UNCERTAINTY

!

Interest income on the customer- financing receivables is recognized

within sales. Changes to the credit loss reserves are recognized in Other

operating income and expense.

2019

3,882

2020 or later

1,137

2018

8,495

2017

15,209

2016

22,608

Non-current customer- financing

receivables maturities

SEK M

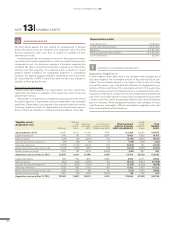

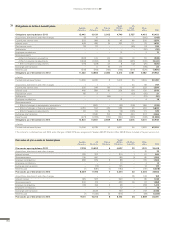

NOTE 15 CUSTOMER-FINANCING RECEIVABLES

Current customer-financing receivables

Current customer-financing receivables Dec 31,

2014 Dec 31,

2013

Installment credits 14 , 6 11 11 , 5 97

Financial leasing 14,617 13,808

Dealerfinancing 17,562 13,676

Other receivables 1,046 988

B/S Current customer financing receivables 47,836 40,069

The effective interest rate for current customer-financing receivables

amounted to 5.31% (5.63) as of December 31, 2014.

Credit risk in customer-financing receivables

Customer-financing receivables,

net of allowance Dec 31,

2014 Dec 31,

2013

Customer-financing receivables gross 100,616 85,040

Valuation allowance for doubtful customer-financing

receivables (1,450) (1,179)

Whereof specific reserve (364) (316)

Whereof other reserve (1,086) (863)

Customer-financing receivables, net 99,166 83,861

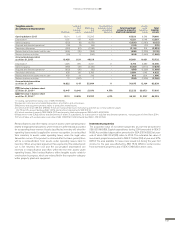

Change of valuation allowance for doubtful

customer-financing receivables 2014 2013

Opening balance 1,179 1,091

New valuation allowance charged to income 1,081 1,292

Reversal of valuation allowance charged to income (161) (437)

Utilization of valuation allowance related to

actual losses (752) (731)

Translation differences 103 (36)

Valuation allowance for doubtful customer-financing

receivables as of December 31 1,450 1,179

FINANCIAL INFORMATION 2014

143