Vodafone 2007 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2007 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

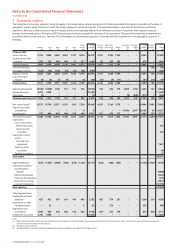

96 Vodafone Group Plc Annual Report 2007

Notes to the Consolidated Financial Statements

continued

Other intangible assets

Other intangible assets with finite lives are stated at cost less accumulated

amortisation and impairment losses. Amortisation is charged to the income

statement on a straight-line basis over the estimated useful lives of

intangible assets from the date they are available for use. The estimated

useful lives are as follows:

Brands 1 – 10 years

Customer bases 3 – 8 years

Property, plant and equipment

Land and buildings held for use are stated in the balance sheet at their cost,

less any subsequent accumulated depreciation and subsequent

accumulated impairment losses.

Equipment, fixtures and fittings are stated at cost less accumulated

depreciation and any accumulated impairment losses.

Assets in the course of construction are carried at cost, less any recognised

impairment loss. Depreciation of these assets commences when the assets

are ready for their intended use.

The cost of property, plant and equipment includes directly attributable

incremental costs incurred in their acquisition and installation.

Depreciation is charged so as to write off the cost or valuation of assets, other

than land and properties under construction, using the straight-line method,

over their estimated useful lives, as follows:

Freehold buildings 25 – 50 years

Leasehold premises the term of the lease

Equipment, fixtures and fittings

•Network infrastructure 3 – 25 years

•Other 3 – 10 years

Depreciation is not provided on freehold land.

Assets held under finance leases are depreciated over their expected useful

lives on the same basis as owned assets or, where shorter, the term of the

relevant lease.

The gain or loss arising on the disposal or retirement of an item of property,

plant and equipment is determined as the difference between the sales

proceeds and the carrying amount of the asset and is recognised in the

income statement.

Impairment of assets

Goodwill

Goodwill is not subject to amortisation but is tested for impairment annually

or whenever there is an indication that the asset may be impaired.

For the purpose of impairment testing, assets are grouped at the lowest

levels for which there are separately identifiable cash flows, known as cash-

generating units. If the recoverable amount of the cash-generating unit is less

than the carrying amount of the unit, the impairment loss is allocated first to

reduce the carrying amount of any goodwill allocated to the unit and then to

the other assets of the unit pro-rata on the basis of the carrying amount of

each asset in the unit. Impairment losses recognised for goodwill are not

reversed in a subsequent period.

Recoverable amount is the higher of fair value less costs to sell and value in

use. In assessing value in use, the estimated future cash flows are discounted

to their present value using a pre-tax discount rate that reflects current

market assessments of the time value of money and the risks specific to the

asset for which the estimates of future cash flows have not been adjusted.

2. Significant accounting policies continued

Intangible assets

Goodwill

Goodwill arising on the acquisition of an entity represents the excess of the

cost of acquisition over the Group’s interest in the net fair value of the

identifiable assets, liabilities and contingent liabilities of the entity recognised

at the date of acquisition. Goodwill is initially recognised as an asset at cost

and is subsequently measured at cost less any accumulated impairment

losses. Goodwill is held in the currency of the acquired entity and revalued to

the closing rate at each balance sheet date.

Goodwill is not subject to amortisation but is tested for impairment.

Negative goodwill arising on an acquisition is recognised directly in the

income statement.

On disposal of a subsidiary or a jointly controlled entity, the attributable

amount of goodwill is included in the determination of the profit or loss

recognised in the income statement on disposal.

Goodwill arising before the date of transition to IFRS, on 1 April 2004, has

been retained at the previous UK GAAP amounts, subject to being tested for

impairment at that date. Goodwill written off to reserves under UK GAAP prior

to 1998 has not been reinstated and is not included in determining any

subsequent profit or loss on disposal.

Licence and spectrum fees

Licence and spectrum fees are stated at cost less accumulated amortisation.

The amortisation periods range from 3 to 25 years and are determined

primarily by reference to the unexpired licence period, the conditions for

licence renewal and whether licences are dependent on specific technologies.

Amortisation is charged to the income statement on a straight-line basis over

the estimated useful lives from the commencement of service of the network.

Computer software

Computer software licences are capitalised on the basis of the costs incurred

to acquire and bring into use the specific software. These costs are amortised

over their estimated useful lives, being 3 to 5 years.

Costs that are directly associated with the production of identifiable and

unique software products controlled by the Group, and that are expected to

generate economic benefits exceeding costs beyond one year, are

recognised as intangible assets. Direct costs include software development

employee costs and directly attributable overheads.

Software integral to a related item of hardware equipment is accounted for as

property, plant and equipment.

Costs associated with maintaining computer software programmes are

recognised as an expense when they are incurred.

Research and development expenditure

Expenditure on research activities is recognised as an expense in the period

in which it is incurred.

An internally-generated intangible asset arising from the Group’s development

activity is recognised only if all of the following conditions are met:

•an asset is created that can be separately identified;

•it is probable that the asset created will generate future economic

benefits; and

•the development cost of the asset can be measured reliably.

Internally-generated intangible assets are amortised on a straight-line basis

over their estimated useful lives. Where no internally-generated intangible

asset can be recognised, development expenditure is charged to the

income statement in the period in which it is incurred.