Vodafone 2007 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2007 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

144 Vodafone Group Plc Annual Report 2007

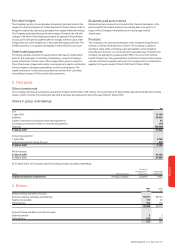

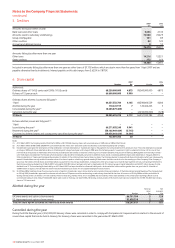

1. Basis of preparation

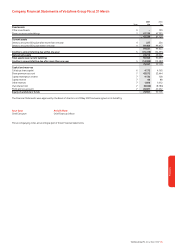

The separate financial statements of the Company are drawn up in

accordance with the Companies Act 1985 and UK generally accepted

accounting principles (“UK GAAP”).

The preparation of financial statements in conformity with generally accepted

accounting principles requires management to make estimates and

assumptions that affect the reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the financial

statements and the reported amounts of revenue and expenses during the

reporting period. Actual results could differ from those estimates. The estimates

and underlying assumptions are reviewed on an ongoing basis. Revisions to

accounting estimates are recognised in the period in which the estimate is

revised if the revision affects only that period or in the period of the revision and

future periods if the revision affects both current and future periods.

As permitted by Section 230 of the Companies Act 1985, the profit and loss

account of the Company is not presented in this Annual Report.

The Company has taken advantage of the exemption contained in FRS 1

“Cash flow statements” and has not produced a cash flow statement.

The Company has taken advantage of the exemption contained in FRS 8

“Related party disclosures” and has not reported transactions with fellow

Group undertakings.

The Company has taken advantage of the exemption contained in FRS 29

“Financial Instruments: Disclosures” and has not produced any disclosures

required by that standard, as full FRS 29 disclosures are available in the

Vodafone Group Plc Annual Report for the year ended 31 March 2007.

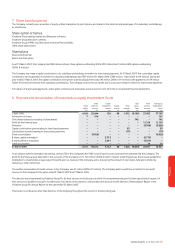

2. Significant accounting policies

The Company’s significant accounting policies are described below.

Accounting convention

The Company Financial Statements are prepared under the historical cost

convention and in accordance with applicable accounting standards of the

UK Accounting Standards Board and pronouncements of the Urgent Issues

Task Force.

Investments

Shares in Group undertakings are stated at cost less any provision for

permanent diminution in value.

The Company assesses investments for impairment whenever events or

changes in circumstances indicate that the carrying value of an investment

may not be recoverable. If any such indication of impairment exists, the

Company makes an estimate of the recoverable amount. If the recoverable

amount of the cash-generating unit is less than the value of the investment,

the investment is considered to be impaired and is written down to its

recoverable amount. An impairment loss is recognised immediately in the

profit and loss account.

For available-for-sale investments, gains and losses arising from changes in

fair value are recognised directly in equity, until the security is disposed of or

is determined to be impaired, at which time the cumulative gain or loss

previously recognised in equity, determined using the weighted average costs

method, is included in the net profit or loss for the period.

Foreign currencies

In preparing the financial statements of the Company, transactions in

currencies other than the Company’s functional currency are recorded at the

rates of exchange prevailing on the dates of the transactions. At each balance

sheet date, monetary items denominated in foreign currencies are

retranslated at the rates prevailing on the balance sheet date. Non-monetary

items carried at fair value that are denominated in foreign currencies are

retranslated at the rate prevailing on the date when fair value was

determined. Non-monetary items that are measured in terms of historical

cost in a foreign currency are not retranslated.

Exchange differences arising on the settlement of monetary items, and on

the retranslation of monetary items, are included in the profit and loss

account for the period. Exchange differences arising on the retranslation of

non-monetary items carried at fair value are included in the profit and loss

account for the period except for differences arising on the retranslation of

non-monetary items in respect of which gains and losses are recognised

directly in equity. For such non-monetary items, any exchange component of

that gain or loss is also recognised directly in equity.

Borrowing costs

All borrowing costs are recognised in the profit and loss account in the period

in which they are incurred.

Taxation

Current tax, including UK corporation tax and foreign tax, is provided at

amounts expected to be paid (or recovered) using the tax rates and laws that

have been enacted or substantively enacted by the balance sheet date.

Deferred tax is provided in full on timing differences that exist at the balance

sheet date and that result in an obligation to pay more tax, or a right to pay less

tax in the future. The deferred tax is measured at the rate expected to apply in

the periods in which the timing differences are expected to reverse, based on

the tax rates and laws that are enacted or substantively enacted at the balance

sheet date. Timing differences arise from the inclusion of items of income and

expenditure in taxation computations in periods different from those in which

they are included in the financial statements. Deferred tax assets are

recognised to the extent that it is regarded as more likely than not that they

will be recovered. Deferred tax assets and liabilities are not discounted.

Financial instruments

Financial assets and financial liabilities, in respect of financial instruments, are

recognised on the balance sheet when the Company becomes a party to the

contractual provisions of the instrument.

Financial liabilities and equity instruments

Financial liabilities and equity instruments issued by the Company are

classified according to the substance of the contractual arrangements

entered into and the definitions of a financial liability and an equity

instrument. An equity instrument is any contract that evidences a residual

interest in the assets of the Company after deducting all of its liabilities and

includes no obligation to deliver cash or other financial assets. The

accounting policies adopted for specific financial liabilities and equity

instruments are set out below.

Capital market and bank borrowings

Interest-bearing loans and overdrafts are initially measured at fair value

(which is equal to cost at inception), and are subsequently measured at

amortised cost, using the effective interest rate method, except where they

are identified as a hedged item in a fair value hedge. Any difference between

the proceeds net of transaction costs and the settlement or redemption of

borrowings is recognised over the term of the borrowing.

Equity instruments

Equity instruments issued by the Company are recorded at the proceeds

received, net of direct issue costs.

Derivative financial instruments and hedge accounting

The Company’s activities expose it to the financial risks of changes in foreign

exchange rates and interest rates.

The use of financial derivatives is governed by the Group’s policies approved

by the board of directors, which provide written principles on the use of

financial derivatives consistent with the Group’s risk management strategy.

Derivative financial instruments are initially measured at fair value on the

contract date, and are subsequently re-measured to fair value at each

reporting date. The Company designates certain derivatives as hedges of the

change of fair value of recognised assets and liabilities (“fair value hedges”).

Hedge accounting is discontinued when the hedging instrument expires or is

sold, terminated, or exercised, or no longer qualifies for hedge accounting.

Notes to the Company Financial Statements