Vodafone 2007 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2007 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

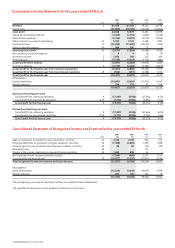

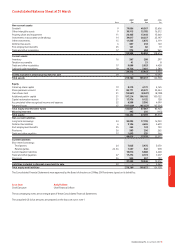

88 Vodafone Group Plc Annual Report 2007

Directors’ Statement of Responsibility

Company law of England and Wales requires the directors to prepare financial

statements for each financial year which give a true and fair view of the state

of affairs of the Company and the Group as at the end of the financial year

and of the profit or loss of the Group for that period. In preparing those

financial statements, the directors are required to:

•select suitable accounting policies and apply them consistently;

•make judgements and estimates that are reasonable and prudent;

•state whether the Consolidated Financial Statements have been prepared

in accordance with IFRS as adopted for use in the EU;

•for the Company Financial Statements, state whether applicable UK

accounting standards have been followed; and

•prepare the financial statements on a going concern basis unless it is

inappropriate to presume that the Company and the Group will continue in

business.

The directors are responsible for keeping proper accounting records which

disclose with reasonable accuracy at any time the financial position of the

Company and the Group and to enable them to ensure that the financial

statements comply with the Companies Act 1985 and Article 4 of the EU

IAS Regulation. They are also responsible for the system of internal control,

for safeguarding the assets of the Company and the Group and, hence, for

taking reasonable steps for the prevention and detection of fraud and other

irregularities.

Disclosure of Information to Auditors

Having made the requisite enquiries, so far as the directors are aware, there

is no relevant audit information (as defined by Section 234ZA of the

Companies Act 1985) of which the Company’s auditors are unaware, and the

directors have taken all the steps they ought to have taken to make

themselves aware of any relevant audit information and to establish that

the Company’s auditors are aware of that information.

Going Concern

After reviewing the Group’s and Company’s budget for the next financial

year, and other longer term plans, the directors are satisfied that, at the time

of approving the financial statements, it is appropriate to adopt the going

concern basis in preparing the financial statements.

Management’s Report on Internal Control over

Financial Reporting

As required by section 404 of the Sarbanes-Oxley Act of 2002, management

is responsible for establishing and maintaining adequate internal control

over financial reporting for the Group.

The Company’s internal control over financial reporting includes policies

and procedures that pertain to the maintenance of records that, in

reasonable detail, accurately and fairly reflect transactions and dispositions

of assets; provide reasonable assurance regarding the reliability of financial

reporting and the preparation of financial statements for external purposes

in accordance with IFRS, including the reconciliations to US GAAP, and that

receipts and expenditures are being made only in accordance with

authorisation of management and the directors of the Company; and

provide reasonable assurance regarding prevention or timely detection of

unauthorised acquisition, use or disposition of the Company’s assets that

could have a material effect on the financial statements.

Any internal control framework, no matter how well designed, has inherent

limitations, including the possibility of human error and the circumvention

or overriding of the controls and procedures, and may not prevent or detect

misstatements. Also, projections of any evaluation of effectiveness to future

periods are subject to the risk that controls may become inadequate

because of changes in conditions or because the degree of compliance with

the policies or procedures may deteriorate.

Management has assessed the effectiveness of the internal control

over financial reporting as at 31 March 2007 based on the Internal Control –

Integrated Framework, issued by the Committee of Sponsoring

Organizations of the Treadway Commission (“COSO”). The assessment

excluded the internal controls over financial reporting relating to Vodafone

Telekomunikasyon A.S. (“Vodafone Turkey “) because the entity was

acquired on 24 May 2006, as described in note 28 to the Consolidated

Financial Statements.

Management has not evaluated the internal controls of Vodacom Group

(Pty) Limited (“Vodacom”), which is accounted for using proportionate

consolidation. The conclusion regarding the effectiveness of internal

control over financial reporting does not extend to the internal controls of

Vodacom. Management is unable to assess the effectiveness of internal

control at Vodacom due to the fact that it does not have the ability to

dictate or modify its controls and does not have the ability, in practice, to

assess those controls.

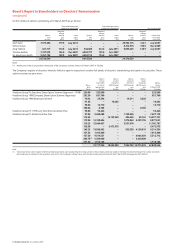

Key sub-totals that result from the consolidation of Vodafone Turkey and

the proportionate consolidation of Vodacom, whose internal controls have

not been assessed, are set out below.

Vodafone

Turkey Vodacom

2007 2007

£m £m

Total assets 607 1,008

Net assets 150 477

Revenue 698 1,478

Profit for the financial year 71 242

Management is not required to evaluate the internal controls of entities

accounted for under the equity method. Accordingly, the internal controls

of these entities, which contributed a net profit of £2,728 million to the loss

for the financial year, have not been assessed, except relating to controls

over the recording of amounts relating to the investments that are recorded

in the Group’s consolidated financial statement.

Based on management’s assessment, management has concluded that the

internal control over financial reporting was effective as at 31 March 2007.

Management’s assessment of the effectiveness of internal control over

financial reporting, as at 31 March 2007, has been audited by Deloitte &

Touche LLP, an independent registered public accounting firm, who also

audit the Group’s Consolidated Financial Statements. Their audit report on

internal control over financial reporting is on page 89.

By Order of the Board

Stephen Scott

Secretary

29 May 2007