Travelers 2012 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2012 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

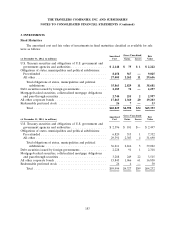

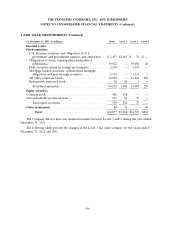

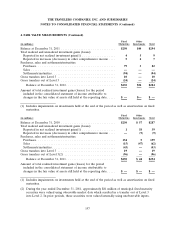

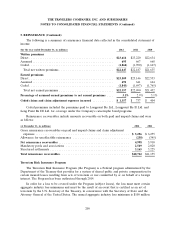

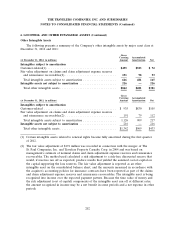

THE TRAVELERS COMPANIES, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

4. FAIR VALUE MEASUREMENTS (Continued)

relevant market information, benchmark curves, benchmarking of like securities, sector groupings and

matrix pricing. Additionally, the pricing service uses an Option Adjusted Spread model to develop

prepayment and interest rate scenarios.

The pricing service evaluates each asset class based on relevant market information, relevant credit

information, perceived market movements and sector news. The market inputs utilized in the pricing

evaluation, listed in the approximate order of priority, include: benchmark yields, reported trades,

broker/dealer quotes, issuer spreads, two-sided markets, benchmark securities, bids, offers, reference

data, and industry and economic events. The extent of the use of each market input depends on the

asset class and the market conditions. Depending on the security, the priority of the use of inputs may

change or some market inputs may not be relevant. For some securities, additional inputs may be

necessary.

The pricing service utilized by the Company has indicated that they will only produce an estimate

of fair value if there is objectively verifiable information to produce a valuation. If the pricing service

discontinues pricing an investment, the Company would be required to produce an estimate of fair

value using some of the same methodologies as the pricing service but would have to make

assumptions for market-based inputs that are unavailable due to market conditions.

The fair value estimates of most fixed maturity investments are based on observable market

information rather than market quotes. Accordingly, the estimates of fair value for such fixed

maturities, other than U.S. Treasury securities, provided by the pricing service are included in the

amount disclosed in Level 2 of the hierarchy. The estimated fair value of U.S. Treasury securities is

included in the amount disclosed in Level 1 as the estimates are based on unadjusted market prices.

The Company also holds certain fixed maturity investments which are not priced by the pricing

service and, accordingly, estimates the fair value of such fixed maturities using an internal matrix that is

based on market information regarding interest rates, credit spreads and liquidity. The underlying

source data for calculating the matrix of credit spreads relative to the U.S. Treasury curve are the BofA

Merrill Lynch U.S. Corporate Index and the BofA Merrill Lynch High Yield BB Rated Index. The

Company includes the fair value estimates of these corporate bonds in Level 2, since all significant

inputs are market observable.

While the vast majority of the Company’s municipal bonds and corporate bonds are included in

Level 2, the Company holds a number of municipal bonds and corporate bonds which are not valued

by the pricing service and estimates the fair value of these bonds using an internal pricing matrix with

some unobservable inputs that are significant to the valuation. Due to the limited amount of observable

market information, the Company includes the fair value estimates for these particular bonds in

Level 3. The fair value of the fixed maturities for which the Company used an internal pricing matrix

was $102 million and $88 million at December 31, 2012 and 2011, respectively. Additionally, the

Company holds a small amount of other fixed maturity investments that have characteristics that make

them unsuitable for matrix pricing. For these fixed maturities, the Company obtains a quote from a

broker (primarily the market maker). The fair value of the fixed maturities for which the Company

received a broker quote was $128 million and $162 million at December 31, 2012 and 2011,

respectively. Due to the disclaimers on the quotes that indicate that the price is indicative only, the

Company includes these fair value estimates in Level 3.

193