Travelers 2012 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2012 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

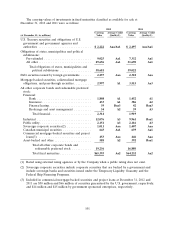

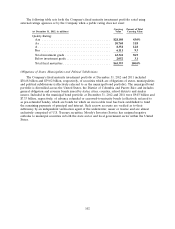

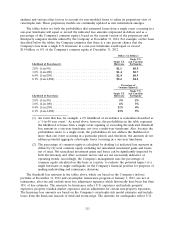

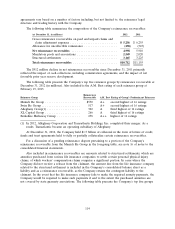

The following table displays the funding sources for the $11.48 billion of municipal bonds

identified as revenue bonds in the foregoing table at December 31, 2012.

Carrying Average Credit

(at December 31, 2012, in millions) Value Quality(1)

Source:

Water and sewer ............................... $ 3,886 Aaa/Aa1

Higher education .............................. 1,824 Aaa/Aa1

Transportation ................................ 1,169 Aa1

Power and utilities ............................. 1,071 Aa2

Special tax ................................... 883 Aa1

Lease ....................................... 536 Aa2

Government funded/grant revenue .................. 139 Aaa

Healthcare ................................... 98 Aa2

Housing ..................................... 97 Aaa/Aa1

General fund ................................. 61 Aa3

Industrial revenue .............................. 51 A1

Property tax .................................. 33 Aa2

Other revenue sources .......................... 1,636 Aaa/Aa1

Total ..................................... $11,484 Aa1

(1) Rated using external rating agencies or by the Company when a public rating does not

exist.

The Company bases its investment decision on the underlying credit characteristics of the

municipal security. While its municipal bond portfolio includes a number of securities that were

enhanced by third-party insurance for the payment of principal and interest in the event of an issuer

default, the Company does not rely on enhanced credit characteristics provided by such third-party

insurance as part of its investing decisions. The downgrade during 2008 and 2009 of credit ratings of

insurers of these securities resulted in a corresponding downgrade in the ratings of many such securities

to the underlying rating of the respective security. Of the insured municipal securities in the Company’s

investment portfolio at December 31, 2012, approximately 99% were rated at A3 or above, and

approximately 92% were rated at Aa3 or above, without the benefit of insurance. The Company

believes that a loss of the benefit of insurance would not result in a material adverse impact on the

Company’s results of operations, financial position or liquidity, due to the underlying credit strength of

the issuers of the securities, as well as the Company’s ability and intent to hold the securities. The

average credit rating of the underlying issuers of these securities was ‘‘Aa2’’ at December 31, 2012. The

average credit rating of the entire municipal bond portfolio was ‘‘Aa1’’ at December 31, 2012 with and

without the enhancement provided by third-party insurance.

104