Travelers 2012 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2012 Travelers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

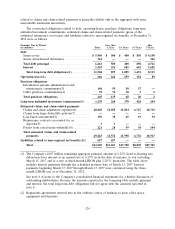

by structured settlements at December 31, 2012 (in millions). Also included is the A.M. Best rating of

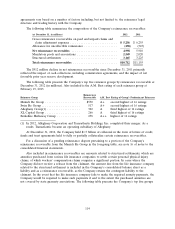

the Company’s predominant insurer from each insurer group at February 19, 2013:

Structured

Group Settlements A.M. Best Rating of Group’s Predominant Insurer

Fidelity & Guaranty Life Group ........... $981 B++ fifth highest of 16 ratings

MetLife Group ....................... 474 A+ second highest of 16 ratings

Genworth Financial Group .............. 437 A third highest of 16 ratings

Symetra Financial Group ................ 256 A third highest of 16 ratings

John Hancock Group .................. 190 A+ second highest of 16 ratings

Reinsurance companies and life insurance companies have been negatively impacted by turbulent

economic conditions, significant catastrophe events and investment portfolio challenges in recent years.

A number of such companies have been subjected to downgrades and/or negative outlook changes by

various ratings agencies, including those with which the Company conducts business. The Company

considers these factors in assessing the adequacy of its allowance for uncollectible amounts.

OUTLOOK

The following discussion provides outlook information for certain key drivers of the Company’s

results of operations and capital position.

Premiums. The Company’s earned premiums are a function of net written premium volume. Net

written premiums comprise both renewal business and new business and are recognized as earned

premium over the life of the underlying policies. When business renews, the amount of net written

premiums associated with that business may increase or decrease (renewal premium change) as a result

of increases or decreases in rate and/or insured exposures, which the Company considers as a measure

of units of exposure (such as the number and value of vehicles or properties insured). Net written

premiums from both renewal and new business, and therefore earned premiums, are impacted by

competitive market conditions as well as general economic conditions, which, particularly in the case of

the Business Insurance segment, affect audit premium adjustments, policy endorsements and mid-term

cancellations. Net written premiums are also impacted by the structure of reinsurance programs and

related costs.

Given the possibility that more active weather patterns such as the Company experienced in a

number of recent periods may continue, as well as the possibility that interest rates may remain low for

some period of time, along with the current level of profitability in certain of its product lines, the

Company has undertaken efforts to improve its underwriting margins. These efforts include seeking

improved rates, as well as improved terms and conditions on many of its insurance products, and also

include other initiatives, such as reducing operating expenses and acquisition costs. These efforts may

not be successful and/or may result in lower retention and new business levels and therefore lower

business volumes. In particular, in the Agency Automobile line of business, the Company has

undertaken various actions to improve its underwriting margins, which have been negatively impacted

by various factors. If these actions are not effective, the Company may need to explore other actions or

initiatives to improve its competitive position and profitability in this line of business. Refer to

‘‘Part I—Item 1A—Risk Factors—The intense competition that we face could harm our ability to

maintain or increase our business volumes and our profitability’’ in this report.

Nonetheless, the Company currently expects retention levels (the amount of expiring premium that

renews, before the impact of renewal premium changes) will remain strong relative to historical

experience. The Company also expects to continue to achieve price increases on renewal business

during 2013 that generally exceed loss cost trends. In the Business Insurance segment, the Company

expects that renewal premium changes during 2013 will be broadly consistent with the higher levels

115