PNC Bank 2000 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2000 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

66

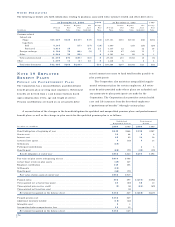

EQ U I T Y MA N A G E M E N T AS S E T S

Equity management assets are included in other assets.

These investments are carried at estimated fair value with

changes in fair value recognized in noninterest income.

GO O D W I L L A N D OT H E R AM O R T I Z A B L E AS S E T S

Goodwill is amortized to expense on a straight-line basis

over periods ranging from 15 to 25 years. Other amortizable

assets are amortized to expense using accelerated or

straight-line methods over their respective estimated useful

lives. On a periodic basis, management reviews goodwill

and other amortizable assets and evaluates events or

changes in circumstances that may indicate impairment in

the carrying amount of such assets. In such instances,

impairment, if any, is measured on a discounted future cash

flow basis.

DE P R E C I AT I O N A N D AM O R T I Z AT I O N

For financial reporting purposes, premises and equipment

are depreciated principally using the straight-line method

over the estimated useful lives ranging from one to 39 years.

Accelerated methods are used for federal income tax pur-

poses. Leasehold improvements are amortized over their

estimated useful lives or the respective lease terms,

whichever is shorter.

RE P U R C H A S E A N D RE S A L E AG R E E M E N T S

Repurchase and resale agreements are treated as collateral-

ized financing transactions and are carried at the amounts

that the securities will be subsequently reacquired or

resold, including accrued interest, as specified in the

respective agreements. The Corporation’s policy is to take

possession of securities purchased under agreements to

resell. The market value of securities to be repurchased and

resold is monitored, and additional collateral may be

obtained where considered appropriate to protect against

credit exposure.

TR E A S U R Y ST O C K

The Corporation records common stock purchased for treas-

ury at cost. At the date of subsequent reissue, the treasury

stock account is reduced by the cost of such stock on the

first-in, first-out basis.

FI N A N C I A L DE R I V A T I V E S

The Corporation uses off-balance-sheet financial derivatives

as part of the overall asset and liability management

process, for commercial mortgage banking risk management

and to manage credit risk. Substantially all such instru-

ments are used to manage risk related to changes in interest

rates. Financial derivatives primarily consist of interest rate

swaps, purchased interest rate caps and floors, forward con-

tracts and credit default swaps.

Interest rate swaps are agreements with a counterparty

to exchange periodic interest payments calculated on a

notional principal amount. Purchased interest rate caps and

floors are agreements where, for a fee, the counterparty

agrees to pay the Corporation the amount, if any, by which a

specified market interest rate is higher or lower than a

defined rate applied to a notional amount.

Interest rate swaps, caps and floors that modify the

interest rate characteristics (such as from fixed to variable,

variable to fixed, or one variable index to another) of desig-

nated interest-bearing assets or liabilities are accounted for

under the accrual method. The net amount payable or

receivable from the derivative contract is accrued as an

adjustment to interest income or interest expense of the des-

ignated instrument. Premiums on contracts are deferred and

amortized over the life of the agreement as an adjustment to

interest income or interest expense of the designated instru-

ments. Unamortized premiums are included in other assets.

Changes in the fair value of financial derivatives

accounted for under the accrual method are not reflected in

results of operations. Realized gains and losses, except loss-

es on terminated interest rate caps and floors, are deferred

as an adjustment to the carrying amount of the designated

instruments and amortized over the shorter of the remaining

original life of the agreements or the designated instru-

ments. Losses on terminated interest rate caps and floors

are recognized immediately in results of operations. If the

designated instruments are disposed, the fair value of the

associated derivative contracts and any unamortized

deferred gains or losses are included in the determination of

gain or loss on the disposition of such instruments.

Contracts not qualifying for accrual accounting are marked

to market with gains or losses included in noninterest

income.

Forward contracts provide for the delivery of financial

instruments at a specified future date and at a specified

price or yield. The Corporation uses forward contracts pri-

marily to manage risk associated with its student lending

activities. Realized gains and losses on mandatory and

optional delivery forward commitments are recorded in non-

interest income in the period settlement occurs. Unrealized

gains or losses are considered in the lower of cost or market

valuation of loans held for sale.