PNC Bank 2000 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2000 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

52

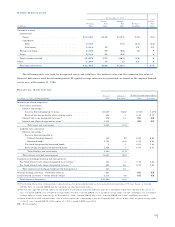

The Corporation models additional interest rate scenar-

ios covering a wider range of rate movements to identify

yield curve, term structure and basis risk exposures. These

scenarios are developed based on historical rate relation-

ships or management’s expectations regarding the future

direction and level of interest rates. Depending on market

conditions and other factors, these scenarios may be mod-

eled more or less frequently. Such analyses are used to

identify inherent risk and develop appropriate strategies.

An economic value of equity model is used by the

Corporation to value all current on-balance-sheet and off-

balance-sheet positions under a range of instantaneous

interest rate changes. The resulting change in the value of

equity is the measure of overall long-term interest rate risk

inherent in the Corporation’s existing on-balance-sheet and

off-balance-sheet positions. The Corporation uses the eco-

nomic value of equity model to complement the net interest

income simulation modeling process.

The Corporation’s risk management policies provide

that the change in economic value of equity should not

decline by more than 1.5% of the book value of assets for a

200 basis point instantaneous increase or decrease in inter-

est rates. Based on the results of the economic value of

equity model at December 31, 2000, if interest rates were to

instantaneously increase by 200 basis points, the model

indicated that the economic value of existing on-balance-

sheet and off-balance-sheet positions would decline by .8%

of assets. If interest rates were to instantaneously decrease

by 200 basis points, the model indicated that the economic

value of existing on-balance-sheet and off-balance-sheet

positions would decrease by .1% of assets.

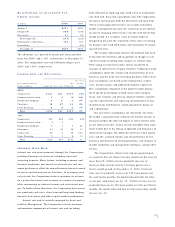

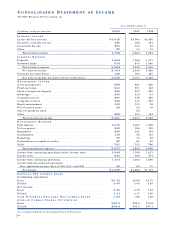

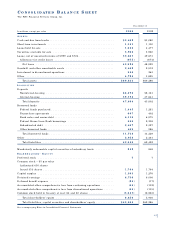

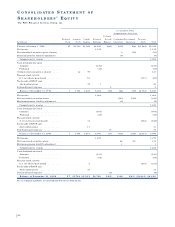

LI Q U I D I T Y RI S K

Liquidity represents the Corporation’s ability to obtain cost-

effective funding to meet the needs of customers as well as

the Corporation’s financial obligations. Liquidity is centrally

managed by Asset and Liability Management, with oversight

provided by the Corporate Asset and Liability Committee

and the Finance Committee of the Board of Directors.

Access to capital markets funding sources is a key fac-

tor affecting liquidity management. Access to such markets

is in part based on the Corporation’s credit ratings, which

are influenced by a number of factors including capital

ratios, credit quality and earnings. Additional factors that

impact liquidity include the maturity structure of existing

assets, liabilities, and off-balance-sheet positions, the level

of liquid securities and loans available for sale, and the

Corporation’s ability to securitize and sell various types

of loans.

Liquidity can also be provided through the sale of

liquid assets, which consist of short-term investments,

loans held for sale and securities available for sale. At

December 31, 2000, such assets totaled $8.7 billion, with

$3.8 billion pledged as collateral for borrowings, trust and

other commitments. Liquidity can also be obtained through

secured advances from the Federal Home Loan Bank, of

which PNC Bank, N.A., PNC’s largest bank subsidiary, is a

member. These borrowings are generally secured by resi-

dential mortgages and mortgage-backed securities. At

December 31, 2000, approximately $7.3 billion of residen-

tial mortgages were available as collateral for borrowings

from the Federal Home Loan Bank. Funding can also be

obtained through alternative forms of borrowing, including

federal funds purchased, repurchase agreements and short-

term and long-term debt issuances.

Liquidity for the parent company and subsidiaries is

also generated through the issuance of securities in public

or private markets and lines of credit. At December 31,

2000, the Corporation had unused capacity under effective

shelf registration statements of approximately $1.4 billion of

debt and equity securities and $400 million of trust pre-

ferred capital securities. In addition, the Corporation had an

unused line of credit of $500 million.

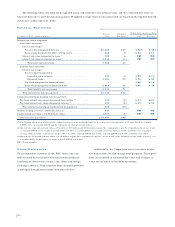

The principal source of parent company revenue and

cash flow is dividends from subsidiary banks. PNC

Bancorp, Inc. is a wholly-owned subsidiary of the parent

company and is the holding company for all bank sub-

sidiaries. There are legal limitations on the ability of bank

subsidiaries to pay dividends and make other distributions

to PNC Bancorp, Inc. and in turn to the parent company.

Without regulatory approval, the amount available for divi-

dend payments to PNC Bancorp, Inc. by all bank sub-

sidiaries was $634 million at December 31, 2000.

Dividends may also be impacted by capital needs, regulato-

ry requirements, corporate policies, contractual restrictions

and other factors.

Management believes the Corporation has sufficient

liquidity to meet current obligations to borrowers, deposi-

tors, debt holders and others. The impact of replacing

maturing liabilities is reflected in the income simulation

model in the overall asset and liability management

process.