PNC Bank 2000 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2000 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

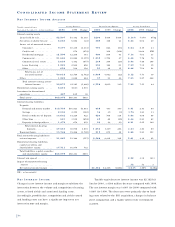

51

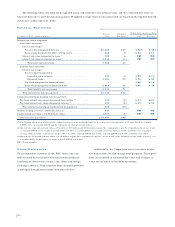

RO L L F O R W A R D O F AL L O WA N C E F O R

CR E D I T LO S S E S

Year ended December 31

In millions 2000 1999

January 1 . . . . . . . . . . . . . . . . . . . . $674 $753

Charge-offs . . . . . . . . . . . . . . . . . . . (186) (216)

Recoveries . . . . . . . . . . . . . . . . . . . 51 55

Net charge-offs . . . . . . . . . . . . . . (135) (161)

Provision for credit losses . . . . . . . . 136 163

Divestitures . . . . . . . . . . . . . . . . . . (81)

December 31 . . . . . . . . . . . . . . . $675 $674

The allowance as a percent of nonaccrual loans and total

loans was 209% and 1.33% , respectively, at December 31,

2000. The comparable year-end 1999 percentages were

232% and 1.36% , respectively.

CH A R G E - O F F S A N D RE C O V E R I E S

Percent of

Year ended December 31 Net Average

Dollars in millions Charge-offs Recoveries Charge-offs Loans

2000

Commercial . . . . . . . . . . $121 $21 $100 .46%

Commercial real estate . . 3 4 (1) (.04)

Residential mortgage . . . 8 2 6 .05

Consumer . . . . . . . . . . . . 46 22 24 .26

Lease financing . . . . . . . 8 2 6 .19

Total . . . . . . . . . . . . . . $186 $51 $135 .27

1999

Commercial . . . . . . . . . . $72 $22 $50 .22%

Commercial real estate . . 4 4

Residential mortgage . . . 8 1 7 .06

Consumer . . . . . . . . . . . . 63 25 38 .37

Credit card . . . . . . . . . . . 60 2 58 8.63

Lease financing . . . . . . . 9 1 8 .31

Total . . . . . . . . . . . . . . $216 $55 $161 .31

IN T E R E S T RA T E RI S K

Interest rate risk arises primarily through the Corporation’s

traditional business activities of extending loans and

accepting deposits. Many factors, including economic and

financial conditions, movements in interest rates and con-

sumer preferences affect the spread between interest earned

on assets and interest paid on liabilities. In managing inter-

est rate risk, the Corporation seeks to minimize its reliance

on a particular interest rate scenario as a source of earnings

while maximizing net interest income and net interest mar-

gin. To further these objectives, the Corporation uses securi-

ties purchases and sales, short-term and long-term funding,

financial derivatives and other capital markets instruments.

Interest rate risk is centrally managed by Asset and

Liability Management. The Corporation actively measures

and monitors components of interest rate risk including

term structure or repricing risk, yield curve or nonparallel

rate shift risk, basis risk and options risk. The Corporation

measures and manages both the short-term and long-term

effects of changing interest rates. An income simulation

model is designed to measure the sensitivity of net interest

income to changing interest rates over the next twenty-four

month period. An economic value of equity model is

designed to measure the sensitivity of the value of existing

on-balance-sheet and off-balance-sheet positions to chang-

ing interest rates.

The income simulation model is the primary tool used

to measure the direction and magnitude of changes in net

interest income resulting from changes in interest rates.

Forecasting net interest income and its sensitivity to

changes in interest rates requires that the Corporation make

assumptions about the volume and characteristics of new

business and the behavior of existing positions. These busi-

ness assumptions are based on the Corporation’s experi-

ence, business plans and published industry experience.

Key assumptions employed in the model include prepay-

ment speeds on mortgage-related assets and consumer

loans, loan volumes and pricing, deposit volumes and pric-

ing, the expected life and repricing characteristics of non-

maturity loans and deposits, and management’s financial

and capital plans.

Because these assumptions are inherently uncertain,

the model cannot precisely estimate net interest income or

precisely predict the effect of higher or lower interest rates

on net interest income. Actual results will differ from simu-

lated results due to the timing, magnitude and frequency of

interest rate changes, the difference between actual experi-

ence and the assumed volume and characteristics of new

business and behavior of existing positions, and changes in

market conditions and management strategies, among other

factors.

The Corporation’s interest rate risk management poli-

cies provide that net interest income should not decrease by

more than 3% if interest rates gradually increase or

decrease from current rates by 100 basis points over a

twelve-month period. At December 31, 2000, if interest

rates were to gradually increase by 100 basis points over

the next twelve months, the model indicated that net inter-

est income would decrease by .3% . If interest rates were to

gradually decrease by 100 basis points over the next twelve

months, the model indicated that net interest income would

increase by .4%.