Capital One 2003 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2003 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

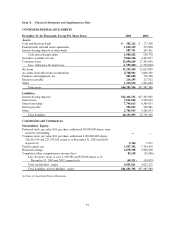

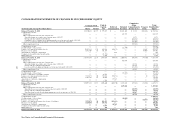

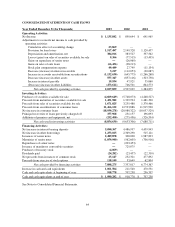

Note A

Significant Accounting Policies

Business

The Consolidated Financial Statements include the accounts of Capital One Financial Corporation (the

“Corporation”) and its subsidiaries. The Corporation is a holding company whose subsidiaries market a variety of

financial products and services to consumers. The principal subsidiaries are Capital One Bank (the “Bank”),

which offers credit card products, Capital One, F.S.B. (the “Savings Bank”), which offers consumer lending

(including credit cards) and deposit products, and Capital One Auto Finance, Inc. (“COAF”) which offers

primarily automobile financing products. The Corporation and its subsidiaries are collectively referred to as the

“Company.”

Basis of Presentation

The accompanying Consolidated Financial Statements have been prepared in accordance with accounting

principles generally accepted in the United States (“GAAP”) that require management to make estimates and

assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results

could differ from these estimates.

All significant intercompany balances and transactions have been eliminated. Certain prior years’ amounts have

been reclassified to conform to the 2003 presentation.

The following is a summary of the significant accounting policies used in preparation of the accompanying

Consolidated Financial Statements.

Recent Accounting Pronouncements

In May 2003, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting

Standard No. 150, Accounting for Certain Financial Instruments with Characteristics of both Liabilities and

Equity, (“SFAS 150”). SFAS 150 provides guidance on the reporting of various types of financial instruments as

liabilities or equity. SFAS 150 is effective for instruments entered into or modified after May 31, 2003 and it is

effective for pre-existing instruments beginning July 1, 2003. The adoption of SFAS 150 did not have an impact

on the consolidated earnings or financial position of the Company.

In April 2003, the FASB issued Statement of Financial Accounting Standard No. 149, Amendment of Statement

133 on Derivative Instruments and Hedging Activities, (“SFAS 149”). SFAS 149 amends SFAS 133, Accounting

for Derivative Instruments and Hedging Activities, for certain decisions made by the FASB as part of the

Derivatives Implementation Group (“DIG”) process and clarifies the definition of a derivative. SFAS 149 also

contains amendments to existing accounting pronouncements to provide more consistent reporting of contracts

that are derivatives or contracts that contain embedded derivatives that require separate accounting. SFAS 149 is

generally effective for contracts entered into or modified after June 30, 2003. The adoption of SFAS 149 did not

have an impact on the consolidated earnings or financial position of the Company.

In April 2003, the FASB issued FASB Staff Position on Accounting for Accrued Interest Receivable Related to

Securitized and Sold Receivables under SFAS No. 140, (the “FSP on AIR”). The FSP on AIR adopts the

provisions of the Interagency Advisory on the Accounting Treatment of Accrued Interest Receivable Related to

Credit Card Securitizations (the “AIR Advisory”) issued jointly by the Office of the Comptroller of the Currency,

The Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation and the

Office of Thrift Supervision. Under the AIR Advisory and the FSP on AIR, any subordinated finance charge and

fee receivables on the investors’ interest in securitized loans should be treated as retained beneficial interests and

not reported as part of “Loans Receivable” or other terminology implying that it has not been subordinated to the

senior interests in the securitization. The FSP on AIR became effective for fiscal quarters beginning after

65